In the modern landscape of digital finance, Cash App has emerged as one of the most popular tools for peer-to-peer (P2P) payments, Bitcoin trading, and even stock investing. However, as users move beyond simple transfers and begin using the platform for more complex financial tasks—such as setting up direct deposits for paychecks or receiving government stimulus funds—a common question arises: “What is Cash App’s banking name?”

To the surprise of many, Cash App is not actually a bank. Instead, it is a financial platform that partners with established banking institutions to provide regulated financial services. Understanding the nuances of these partnerships is essential for anyone looking to use Cash App as a primary component of their personal finance strategy.

Understanding Cash App’s Banking Partners

Cash App is a financial technology (FinTech) platform developed by Block, Inc. (formerly Square, Inc.). Because Block is not a chartered bank, it cannot legally hold deposits or issue debit cards on its own. To bridge this gap, Cash App utilizes “partner banks” to handle the regulated aspects of banking.

Sutton Bank: The Issuer of the Cash Card

When you order a Cash Card—the Visa debit card linked to your Cash App balance—you are technically interacting with Sutton Bank. Based in Ohio, Sutton Bank is the primary issuer of the physical and virtual cards provided to Cash App users. If you are asked for the bank name associated with your debit card for a merchant refund or a verification process, Sutton Bank is typically the entity responsible for the card’s infrastructure.

Lincoln Savings Bank: The Direct Deposit Partner

While Sutton Bank handles the cards, Lincoln Savings Bank often manages the underlying routing and account numbers used for direct deposits. When you navigate to the “Money” tab in your Cash App and see a routing number and an account number, these are frequently provided through Lincoln Savings Bank’s infrastructure. This allows Cash App to function like a traditional checking account, enabling users to receive paychecks, tax refunds, and unemployment benefits directly into the app.

The Role of Wells Fargo

In certain instances involving large-scale transfers or specific back-end settlements, Wells Fargo may also play a role in the Cash App ecosystem. However, for the average user setting up a direct deposit or looking for their “banking name” for a form, Lincoln Savings Bank and Sutton Bank are the two names that most frequently appear on official documentation.

How to Find Your Specific Banking Information

Because Cash App uses different partners for different users and services, you should never guess your banking name or routing number. Your specific account details are unique to your profile and must be verified within the app to ensure successful transactions.

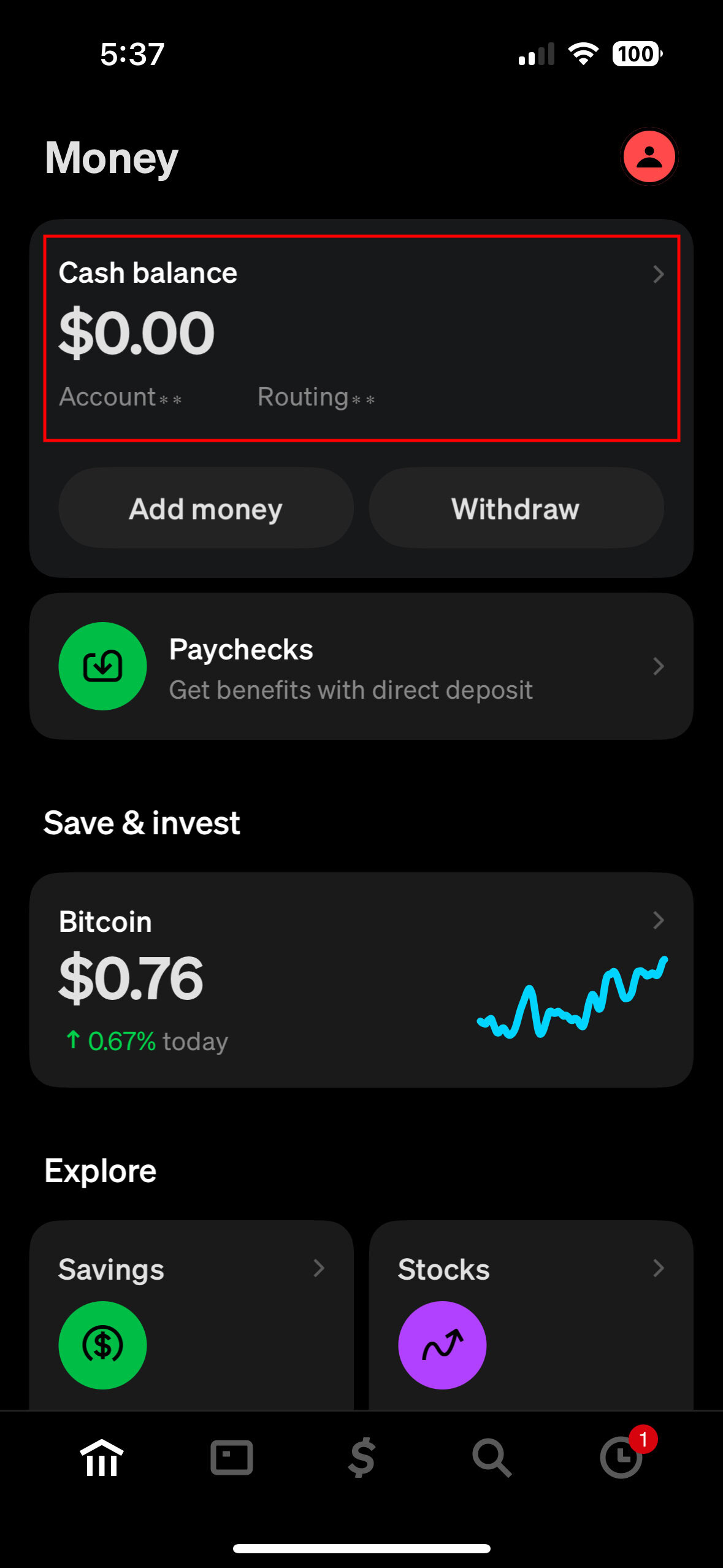

Locating Your Routing and Account Numbers

To find the banking information required for a direct deposit or to pay a bill using your Cash App balance, follow these steps:

- Open Cash App and tap the Money tab (the bank icon or dollar amount on the bottom left).

- Tap the Routing and Account Number section located under your balance.

- Here, you will see your specific routing number and your unique account number.

- You can tap the numbers to copy them directly to your clipboard.

Identifying the Correct Bank Name for Forms

When filling out a direct deposit form for an employer, the “Bank Name” field can sometimes be tricky. Generally, if you have located your routing number using the steps above, you can look up that specific routing number online to confirm the associated bank. In most cases, it will be Lincoln Savings Bank. However, some users may find their accounts are serviced by different partners as Cash App expands its network. Always use the name associated with the routing number provided in your specific app interface.

Why You Shouldn’t Use a Friend’s Information

It is a common mistake in personal finance management to assume that all Cash App users share the same banking details. Since Cash App assigns accounts through different partner branches, your routing number may differ from a friend’s. Using incorrect information can lead to rejected transfers or, in worse cases, funds being sent to the wrong institution, leading to significant delays in accessing your money.

The Benefits of Using Cash App for Personal Finance

Using a FinTech platform like Cash App instead of a traditional brick-and-mortar bank offers several distinct advantages, particularly for those looking for speed and ease of use.

Early Direct Deposit

One of the most significant draws of Cash App is the “Early Direct Deposit” feature. Most traditional banks hold onto incoming funds for a “settlement period,” which can delay your access to your paycheck. Because Cash App uses a streamlined digital infrastructure, users can often receive their paychecks up to two days earlier than they would at a standard bank. For individuals managing tight monthly budgets, this 48-hour window can be a vital lifeline.

Tax Refunds and Stimulus Payments

By providing users with a standard routing and account number, Cash App allows individuals to receive federal and state tax refunds directly. This is particularly beneficial for the “unbanked” or “underbanked” population—those who may not have access to traditional checking accounts due to credit history or high minimum balance requirements. Cash App provides a path to digital financial inclusion without the monthly maintenance fees often associated with big-name banks.

Integration with Peer-to-Peer Payments

By keeping your primary “banking” functions within the same app you use to split dinner bills or pay rent to a roommate, you eliminate the friction of transferring money between institutions. When your paycheck lands in Cash App, it is immediately available to be sent to other users, spent via the Cash Card, or invested in the stock market—all within a single ecosystem.

Safety, Security, and FDIC Insurance

A major concern for anyone moving their money into a FinTech app is whether their funds are safe. If Cash App isn’t a bank, does it have the same protections as a bank?

Is Your Money FDIC Insured?

In a traditional bank, deposits are insured by the Federal Deposit Insurance Corporation (FDIC) up to $250,000. For Cash App users, the insurance is “pass-through.” This means that the money you hold in Cash App is deposited into accounts at partner banks (like Lincoln Savings Bank or Sutton Bank) that are FDIC-insured.

However, there is a catch: to be eligible for FDIC insurance through Cash App, you generally must have a Cash Card. This card links your identity to the account, allowing the partner banks to provide the necessary regulatory coverage. If you use Cash App without a Cash Card, your balance may not be covered by FDIC insurance in the same way.

Security Features for Your Funds

Beyond federal insurance, Cash App employs several layers of digital security to protect your personal finance assets:

- Security Locks: You can require a PIN or biometric ID (FaceID/TouchID) for every payment.

- Instant Freezing: If you lose your Cash Card, you can instantly disable it within the app to prevent unauthorized spending.

- Notification Alerts: Real-time push notifications for every transaction help you spot fraudulent activity immediately.

Comparing Cash App to Traditional Banking Institutions

While Cash App offers many “bank-like” features, it is important to understand where it differs from traditional institutions like Chase, Bank of America, or local credit unions.

Fees and Limitations

Traditional banks often charge monthly maintenance fees unless a minimum balance is met. Cash App is generally free to use, with no monthly fees or minimums. However, it makes its money through other avenues, such as “Instant Transfer” fees (if you want to move money to an external bank account immediately rather than waiting 1-3 days) and ATM withdrawal fees.

Customer Service Considerations

One of the primary drawbacks of using a FinTech app for all your banking needs is the lack of physical branches. If you have a problem with a traditional bank, you can walk into a branch and speak to a manager. With Cash App, all support is handled through the app or via phone. For complex financial disputes, some users find the digital-only support model to be less responsive than a traditional banking relationship.

Building Your Financial Ecosystem

For many savvy personal finance enthusiasts, the best strategy is a “hybrid” approach. They use a traditional bank for long-term savings and mortgage payments, while using Cash App’s banking features for daily spending, early direct deposits, and P2P convenience. By understanding that Sutton Bank and Lincoln Savings Bank are the engines behind the app, you can more confidently integrate Cash App into your broader financial life, ensuring your money is handled with the same professionalism and security as any other major financial institution.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.