In the landscape of personal finance, few acronyms carry as much weight—or cause as much confusion—as APR. Standing for Annual Percentage Rate, APR is the most critical metric for anyone utilizing credit cards, yet many consumers treat it as a secondary detail behind rewards programs or sign-up bonuses. Understanding APR is not merely an academic exercise; it is a fundamental pillar of debt management and wealth preservation.

In the context of a credit card, the APR represents the cost of borrowing money over a one-year period. However, because credit cards are revolving lines of credit, the way this interest is calculated and applied is more complex than a simple annual fee. This guide delves into the mechanics of APR, the various types of rates you may encounter, and strategic ways to navigate these costs to maintain a healthy financial profile.

The Mechanics of Credit Card APR: How Interest is Calculated

To manage your finances effectively, you must look beyond the “annual” in Annual Percentage Rate. While the rate is expressed as a yearly figure, credit card issuers do not wait until the end of the year to calculate what you owe. Instead, they typically use a daily periodic rate to apply interest to your balance.

Understanding the Daily Periodic Rate

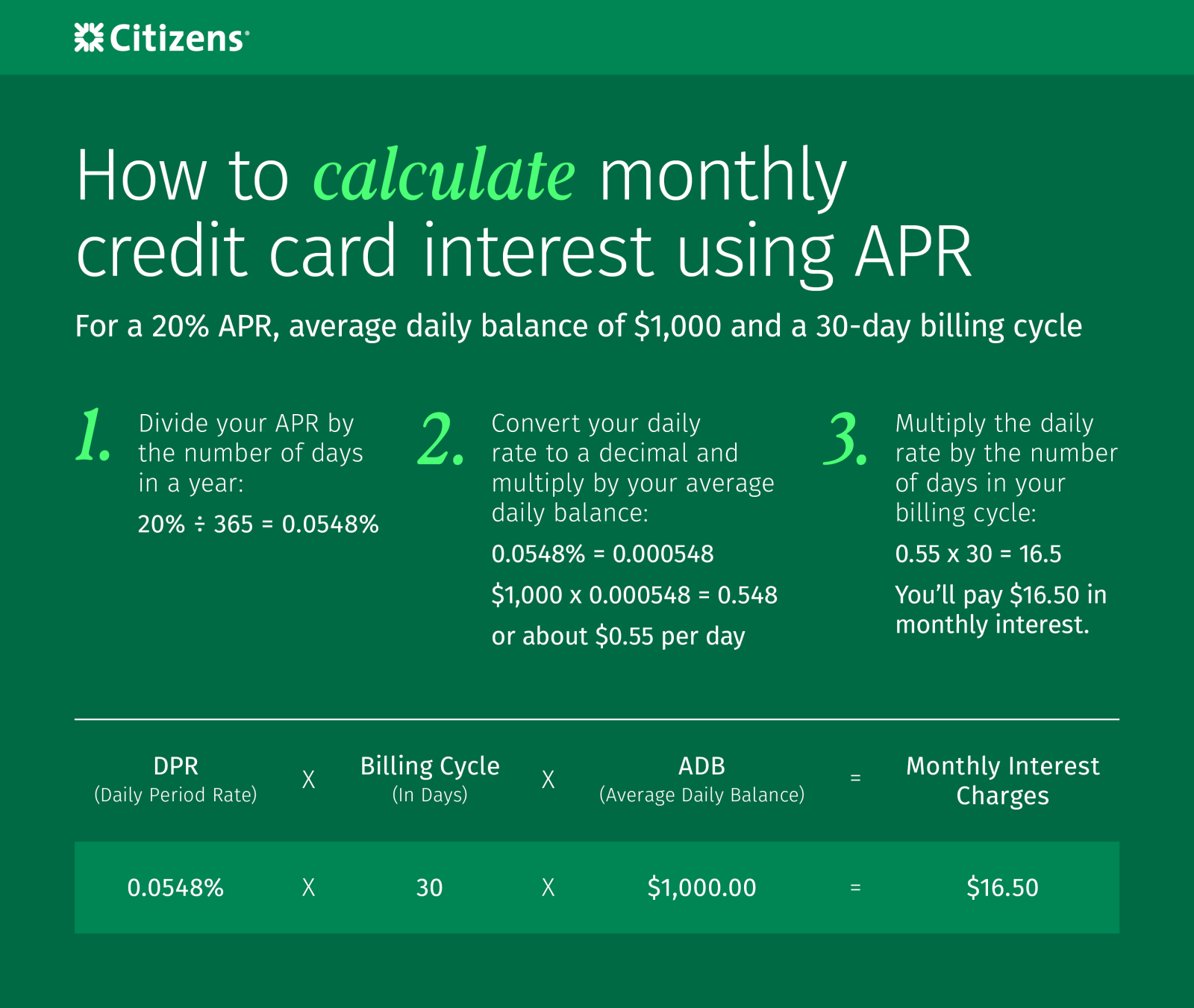

The Daily Periodic Rate (DPR) is the APR divided by 365 (the number of days in a year). For example, if your credit card has an APR of 21.99%, your DPR is approximately 0.0602%. Every day that you carry a balance, the bank applies this small percentage to your “average daily balance.” This process is known as compounding. While some cards compound interest monthly, most modern credit cards compound daily, meaning you are paying interest on the interest that accrued the day before. Over time, this can lead to a significant increase in the total amount owed if the balance is not paid in full.

The Average Daily Balance Method

Most issuers use the “Average Daily Balance” method to determine how much interest to charge at the end of a billing cycle. To find this number, the issuer adds up your balance at the end of each day in the billing cycle and divides it by the number of days in that cycle. This total is then multiplied by the DPR and the number of days in the billing cycle. Because this calculation happens behind the scenes, many consumers are surprised by the size of their interest charges, especially if they make large purchases early in a billing cycle.

The Different Types of Credit Card APR

One of the most common misconceptions is that a credit card has a single, static APR. In reality, a single card can have multiple APRs that apply to different types of transactions. Knowing which rate applies to which action is essential for avoiding high-cost mistakes.

Purchase APR and Promotional Rates

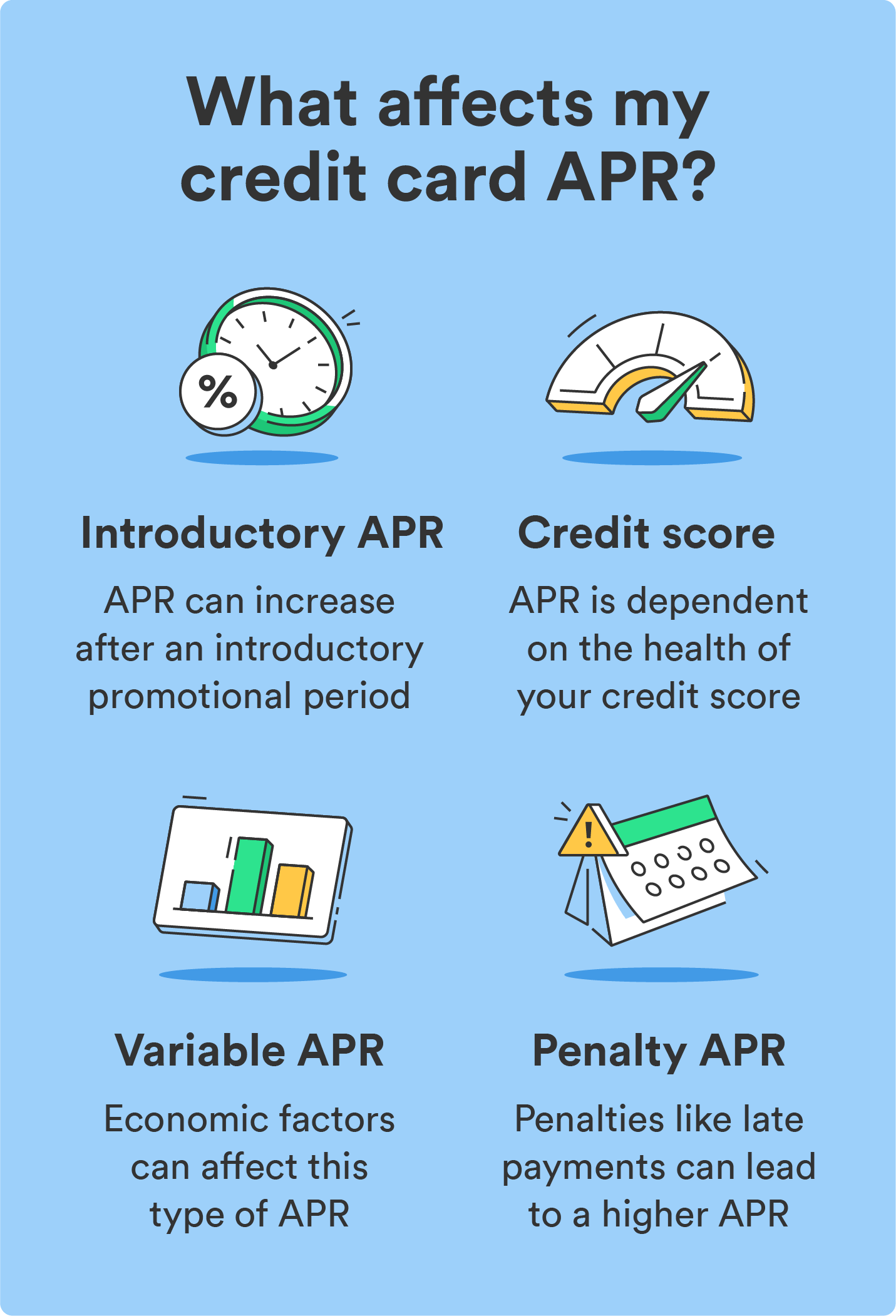

The Purchase APR is the “standard” rate applied to most things you buy, from groceries to electronics. This is the rate most frequently advertised by lenders. However, many issuers offer an “Introductory APR,” which might be 0% for the first 12 to 18 months. These promotional rates are powerful financial tools for consolidating debt or financing a large purchase interest-free, provided the balance is paid off before the promotional window closes. Once that window shuts, the rate typically jumps to a much higher standard purchase APR.

Cash Advance and Balance Transfer APRs

Borrowing cash from an ATM using your credit card is significantly more expensive than using the card for a purchase. Cash Advance APRs are typically much higher than purchase APRs—often exceeding 25% or 30%. Furthermore, cash advances usually do not have a “grace period,” meaning interest begins accruing the moment the cash is in your hand.

Balance Transfer APRs apply when you move debt from one card to another. While some cards offer 0% introductory balance transfer rates, the standard balance transfer APR is often slightly different from your purchase APR. Additionally, these transactions usually incur a one-time fee (typically 3% to 5% of the transferred amount), which must be factored into the total cost of borrowing.

Penalty APR: The Cost of Delinquency

Perhaps the most “expensive” rate is the Penalty APR. If you trigger this rate—usually by making a payment 60 days late—your APR can skyrocket to nearly 30%. This rate can stay in effect indefinitely, or until you make several consecutive on-time payments. The Penalty APR is designed to mitigate the bank’s risk when a borrower shows signs of financial instability, but for the consumer, it can create a “debt spiral” that is difficult to escape.

Variable vs. Fixed APR: The Role of the Prime Rate

When you look at your credit card agreement, you will likely see that your APR is “Variable.” In the modern financial era, fixed-rate credit cards are extremely rare. A variable APR is tied to an index, most commonly the U.S. Prime Rate.

How Federal Reserve Decisions Impact Your Interest

The Prime Rate is influenced heavily by the Federal Funds Rate, which is set by the Federal Reserve. When the Fed raises interest rates to combat inflation, the Prime Rate rises shortly thereafter. Because most credit card APRs are calculated as “Prime Rate + Margin,” your credit card interest rate will increase automatically when the Fed acts. For example, if your card’s margin is 15% and the Prime Rate is 8.5%, your APR is 23.5%. If the Prime Rate moves to 9%, your APR becomes 24%.

Navigating Fluctuating Interest Costs

Since variable rates are outside of the consumer’s direct control, the only way to “hedge” against rising rates is to minimize the balance carried from month to month. In a high-interest-rate environment, the cost of carrying a $5,000 balance can increase by hundreds of dollars a year purely due to macroeconomic shifts. Understanding this relationship helps consumers realize that their credit card costs are dynamic and require regular monitoring of financial news and monthly statements.

Strategies to Minimize APR Costs and Manage Debt

While APR is a reality of using credit, it does not have to be a financial burden. By understanding the rules of the game, savvy consumers can use credit cards for years without ever paying a cent in interest.

The Power of the Grace Period

The “grace period” is the most effective tool for avoiding interest. This is the gap between the end of your billing cycle and your payment due date. If you pay your “statement balance” in full by the due date every month, the issuer will waive the interest on your purchases. In this scenario, your effective APR is 0%, regardless of what the card’s actual rate is. However, if you carry even a small portion of that balance over to the next month, the grace period is usually revoked for all subsequent purchases until the balance is fully cleared.

Negotiation and Improving Your Credit Score

Your APR is not necessarily set in stone. It is largely a reflection of your “creditworthiness.” Lenders use your credit score (FICO or VantageScore) to determine the risk of lending to you. If your credit score has improved significantly since you first opened the account, you can call your issuer and request a lower APR. Many banks are willing to lower rates for long-term customers with a perfect payment history to prevent them from moving their business to a competitor.

Leveraging Balance Transfers and Debt Consolidation

For those already struggling with high-interest debt, the strategy shifts toward mitigation. Utilizing a 0% APR balance transfer card can provide a “breathing room” period where 100% of your monthly payment goes toward the principal balance rather than interest. However, this requires discipline; if the balance is not cleared during the introductory period, the high interest rates return, often on a larger balance if the consumer continued to spend.

Conclusion: APR as a Financial Health Metric

At its core, the APR on your credit card is the price of liquidity. It is the cost of spending money today that you haven’t yet earned. While credit cards offer unparalleled convenience and security, the APR is the mechanism that allows banks to profit from that convenience.

By understanding the difference between daily compounding and annual rates, recognizing the various types of APRs for different transactions, and staying aware of how the Federal Reserve influences variable rates, you can move from being a passive consumer to an active manager of your financial life. The goal is not just to have a low APR, but to build a financial structure where the APR becomes irrelevant because you are leveraging the grace period and paying your balances in full. In the world of personal finance, knowledge of the APR is the ultimate defense against the eroding effects of high-interest debt.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.