The dream of homeownership is a cornerstone of the American experience, a tangible symbol of stability and achievement. For many, however, the path to owning a home is paved with financial hurdles, primarily the significant down payment and the often-daunting mortgage process. While conventional loans are a familiar route, there’s a powerful and often underutilized option available to a specific group of individuals: the VA mortgage loan. Backed by the U.S. Department of Veterans Affairs (VA), these loans offer a distinct set of advantages that can make homeownership more accessible and affordable for eligible veterans and service members.

This article will delve into the intricacies of VA mortgage loans, exploring what they are, who qualifies, their unique benefits, and the process involved in securing one. We’ll also touch upon how the principles of smart financial planning, often discussed in personal finance circles, are intrinsically linked to leveraging this valuable benefit.

Understanding the VA Mortgage Loan: A Benefit Rooted in Service

At its core, a VA mortgage loan is a home loan guaranteed by the Department of Veterans Affairs. This guarantee allows private lenders, such as banks and mortgage companies, to offer more favorable terms to eligible borrowers. The VA doesn’t directly lend money; instead, it insures a portion of the loan, reducing the risk for the lender. This reduced risk translates into significant advantages for the borrower, making it a powerful tool for achieving homeownership.

The genesis of the VA loan program can be traced back to the Servicemen’s Readjustment Act of 1944, commonly known as the GI Bill of Rights. This landmark legislation was designed to provide returning World War II veterans with a range of benefits, including educational opportunities and preferential access to housing. Over the decades, the program has evolved to continue supporting those who have served, recognizing their sacrifice and commitment.

Key Features and Benefits That Set VA Loans Apart

The appeal of a VA mortgage loan lies in its distinct features that often make it superior to conventional financing. These benefits are designed to alleviate financial burdens and simplify the home buying process for those who have earned them through their service.

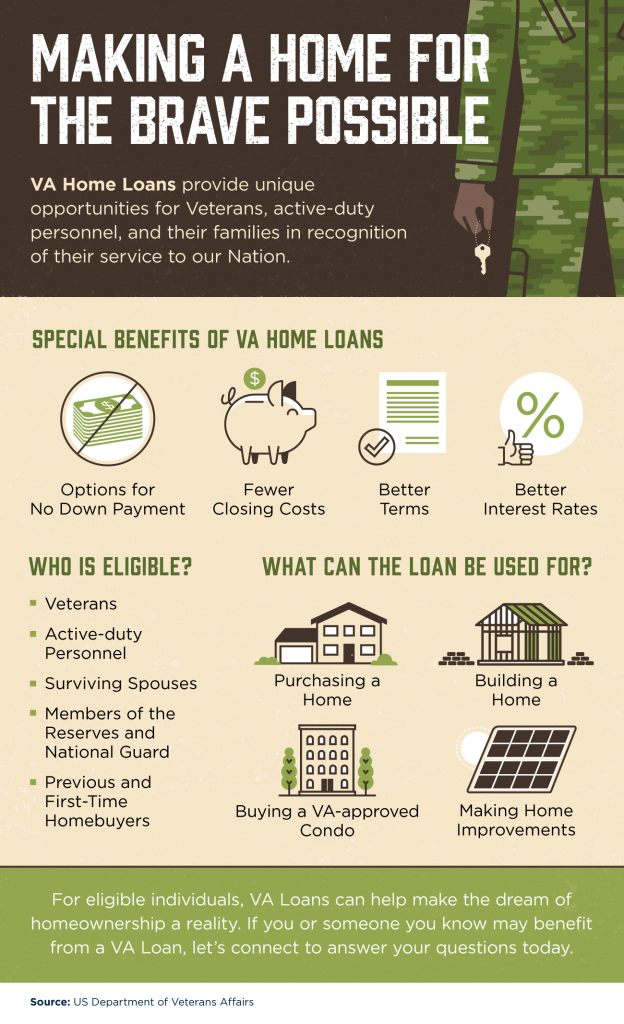

Eliminating Down Payments: A Game-Changer for Accessibility

Perhaps the most significant and celebrated benefit of a VA loan is the absence of a down payment requirement for most eligible borrowers. For conventional loans, a down payment can range from 5% to 20% of the home’s purchase price, representing a substantial upfront cost. For many first-time homebuyers or those looking to upgrade, saving for such a down payment can be a considerable obstacle.

With a VA loan, eligible veterans can finance up to 100% of the home’s value. This means that if you qualify, you can purchase a home without needing to tap into your savings for a down payment. This can dramatically accelerate the timeline to homeownership, allowing individuals to build equity sooner and avoid the financial strain of a large upfront payment. This benefit aligns with the broader principles of smart financial management, where minimizing debt and maximizing liquidity are often prioritized. By removing the down payment hurdle, VA loans enable a more immediate entry into the real estate market.

Competitive Interest Rates: Saving Money Over the Long Term

Beyond the zero-down payment advantage, VA loans typically come with competitive interest rates. Because the loan is guaranteed by the VA, lenders face less risk and can therefore offer lower interest rates compared to conventional mortgages. Over the lifespan of a 30-year mortgage, even a small difference in interest rate can translate into tens of thousands of dollars saved.

This focus on affordability is crucial in the realm of personal finance. Lower interest rates mean lower monthly payments, freeing up more of your income for other financial goals, such as investing, saving for retirement, or paying down other debts. When considering long-term financial planning, securing the lowest possible interest rate on your mortgage is paramount, and VA loans often provide that opportunity.

No Private Mortgage Insurance (PMI): Reducing Monthly Costs

Another significant financial advantage of VA loans is the elimination of Private Mortgage Insurance (PMI). PMI is typically required for conventional loans when a borrower puts down less than 20% of the home’s purchase price. PMI protects the lender in case the borrower defaults on the loan. While it serves a purpose for lenders, PMI adds a recurring cost to the borrower’s monthly mortgage payment.

VA loans, due to their government guarantee, do not require PMI. Instead, they have a VA Funding Fee. While the VA Funding Fee is a one-time charge, it can be financed into the loan, meaning you don’t have to pay it upfront in cash. This avoids the ongoing monthly expense of PMI, further reducing your housing costs and contributing to your overall financial well-being. From a financial strategy perspective, eliminating a recurring monthly expense like PMI can free up significant funds over time.

Limited Foreclosure Impact: Protecting Service Members

The VA also has provisions in place to help veterans avoid foreclosure. The VA actively works with lenders to find alternatives to foreclosure, such as loan modifications or repayment plans, when borrowers face financial difficulties. This commitment to helping service members retain their homes underscores the program’s dedication to supporting those who have served. This protective measure aligns with the idea of building financial resilience, ensuring that unforeseen circumstances don’t lead to the loss of a significant asset.

Eligibility Requirements: Who Qualifies for a VA Loan?

The benefits of a VA loan are reserved for those who have served in the U.S. military. While the core requirement is service, there are specific eligibility criteria that applicants must meet.

Service Requirements: Demonstrating Your Commitment

To qualify for a VA loan, you must meet specific service requirements. These typically include:

- During peacetime: Having served at least 90 consecutive days on active duty.

- During wartime: Having served at least 90 days on active duty.

- For National Guard and Reserve members: Having served at least six years, or having been called to active duty for at least 90 days.

- Spouses: Surviving spouses of veterans who died in service or from a service-related disability may also be eligible.

The VA will issue a Certificate of Eligibility (COE) to confirm that you meet these service requirements. This certificate is a crucial document in the VA loan application process.

Credit and Income Requirements: Demonstrating Financial Responsibility

While the VA guarantees the loan, lenders will still assess your ability to repay the mortgage. This means you’ll need to meet certain credit and income requirements set by the individual lender.

- Credit Score: While the VA doesn’t set a minimum credit score, most lenders do. Typically, you’ll need a credit score in the mid-600s or higher to qualify for a VA loan, though some lenders may have slightly lower or higher requirements. A good credit score demonstrates responsible financial behavior, a key factor in any lending decision.

- Income and Employment Stability: Lenders will review your income and employment history to ensure you have a stable source of funds to make your monthly mortgage payments. They will look for a consistent employment history and sufficient income to cover your debt-to-income ratio, which compares your monthly debt obligations to your gross monthly income. Sound personal finance management emphasizes maintaining stable income and a manageable debt load.

It’s important to note that while the VA loan removes the down payment and PMI, it’s still a significant financial commitment. Demonstrating financial responsibility through good credit and stable income is essential for approval.

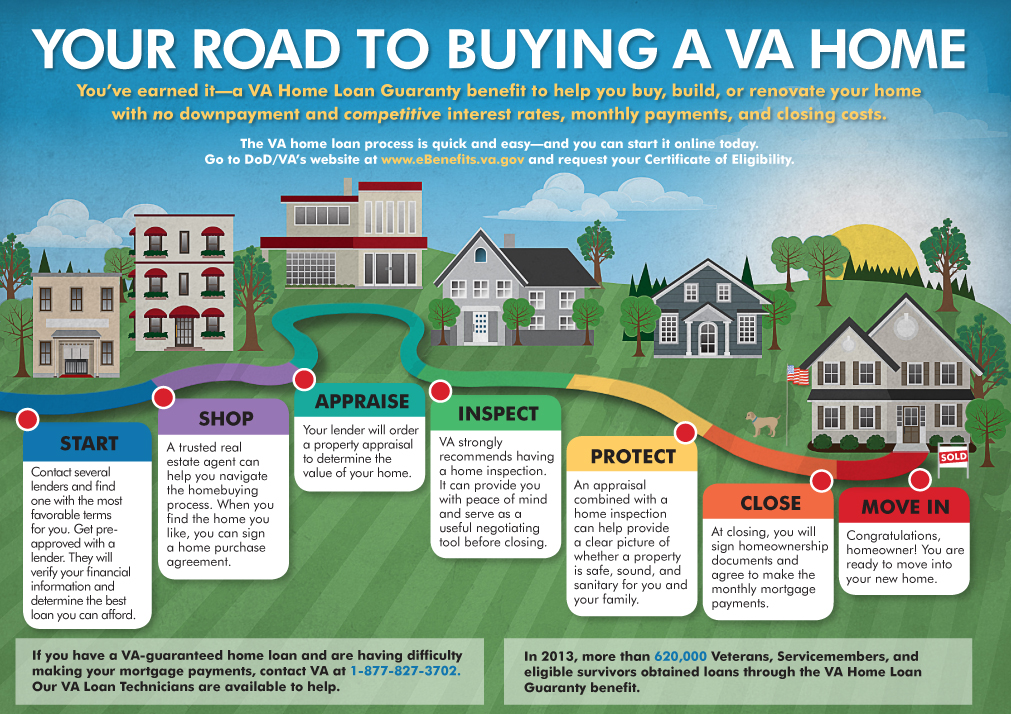

The VA Loan Process: Navigating Your Path to Homeownership

Securing a VA loan involves a process similar to obtaining any other mortgage, but with a few VA-specific steps. Understanding these steps can help streamline your journey.

Step 1: Obtain Your Certificate of Eligibility (COE)

As mentioned earlier, your COE is the first critical document. You can obtain your COE online through the VA’s eBenefits portal, by mail, or through your lender, who can often request it on your behalf. Having your COE readily available will expedite the loan process.

Step 2: Get Pre-Approved by a VA-Approved Lender

Once you have your COE, you’ll need to find a VA-approved lender. Not all lenders offer VA loans, so it’s important to research and compare options. Once you’ve chosen a lender, you’ll go through the pre-approval process. This involves providing financial documentation, such as pay stubs, tax returns, and bank statements, so the lender can assess your financial standing and determine how much you can borrow. Being pre-approved gives you a clear budget and strengthens your offer when you find a home.

Step 3: Find a Home and Make an Offer

With your pre-approval in hand, you can begin your home search. When you find a property you’re interested in, you’ll make an offer. If your offer is accepted, you’ll proceed to the next stages of the loan process.

Step 4: The VA Appraisal and Home Inspection

Unlike conventional loans, VA loans require a VA appraisal to ensure the home meets the VA’s minimum property requirements (MPRs). These MPRs are in place to protect the veteran borrower by ensuring the home is safe, sound, and sanitary. A home inspection, while not mandatory by the VA, is highly recommended to identify any potential issues with the property.

Step 5: Underwriting and Closing

The lender will then submit your loan application to underwriting for final approval. Once approved, you’ll proceed to closing, where you’ll sign all the necessary paperwork, and the loan will be funded. At closing, you’ll also pay the VA Funding Fee (unless you’re exempt) and any other closing costs.

VA Funding Fee: Understanding the One-Time Charge

The VA Funding Fee is a one-time, upfront fee that helps keep the VA loan program running and reduces the cost to taxpayers. The amount of the funding fee varies depending on several factors, including:

- Type of service: Whether you are an active-duty service member, veteran, National Guard member, or reservist.

- Down payment amount: The percentage of the down payment you make (if any).

- Prior use of VA loan benefits: Whether this is your first time using a VA loan or if you’ve used it before.

While the funding fee can seem like an additional cost, remember that it’s often financed into the loan, meaning you don’t pay it out-of-pocket. Furthermore, certain veterans, such as those receiving VA disability compensation, are exempt from paying the funding fee.

Conclusion: A Powerful Tool for Veteran Homeownership

The VA mortgage loan is an invaluable benefit earned through dedicated service to our country. By eliminating the need for a down payment and PMI, offering competitive interest rates, and providing robust borrower protections, VA loans significantly lower the financial barriers to homeownership for eligible veterans and service members.

Understanding the eligibility requirements, the application process, and the unique features of VA loans empowers veterans to make informed decisions about their housing journey. When combined with sound personal finance principles and diligent planning, leveraging a VA mortgage loan can transform the dream of homeownership into a tangible reality, providing a stable foundation for the future. If you’re a veteran or an active-duty service member, exploring the possibility of a VA loan is a crucial step in building your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.