For many, the journey toward homeownership begins not with a walk-through of a sun-drenched living room, but with a spreadsheet. The question “How much do I qualify for?” is the most critical hurdle in the real estate process. It defines the neighborhoods you can explore, the type of property you can afford, and the long-term health of your personal finances.

Determining your mortgage qualification is a multifaceted process that lenders use to assess risk. While online calculators provide a quick estimate, a true understanding of your borrowing power requires a deep dive into your income, debt obligations, and credit history. This guide explores the financial mechanics behind mortgage qualification, helping you navigate the complexities of the lending world with confidence.

The Financial Pillars of Mortgage Qualification

Lenders do not simply look at your salary and hand over a check. They utilize a series of standardized metrics to ensure that you can realistically manage a mortgage payment alongside your other life expenses. Understanding these pillars allows you to see your finances through the eyes of a bank.

Debt-to-Income Ratio (DTI): The Golden Metric

The Debt-to-Income (DTI) ratio is perhaps the most significant factor in determining your loan amount. It represents the percentage of your gross monthly income that goes toward paying debts. Lenders typically look at two types of DTI:

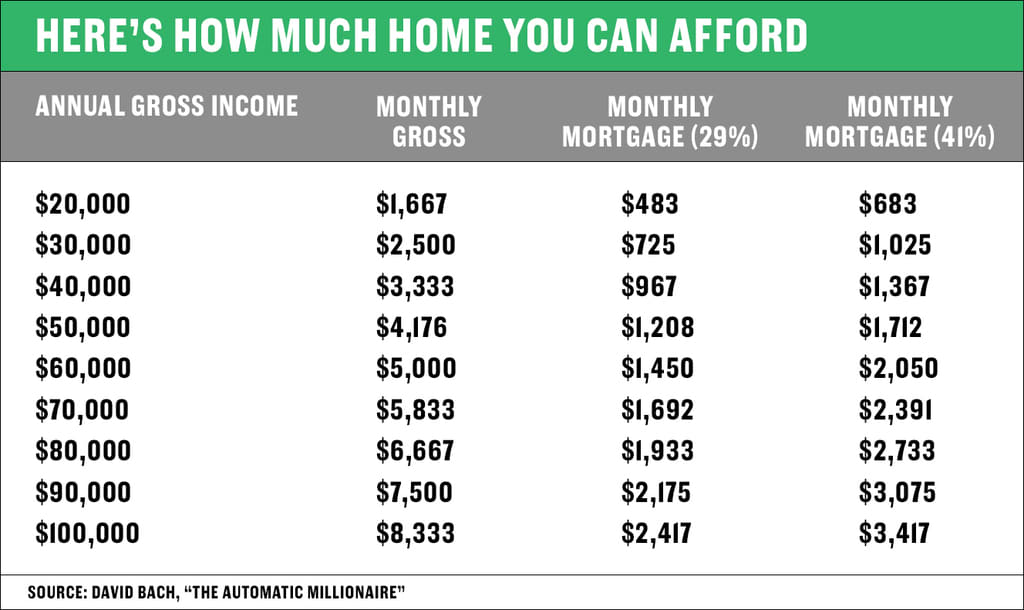

- Front-End Ratio: This is the percentage of your income that would go toward your future housing expenses (principal, interest, taxes, and insurance). Most lenders prefer this to stay below 28%.

- Back-End Ratio: This includes your housing expenses plus all other monthly debt obligations, such as car loans, student loans, and credit card minimums. A common benchmark for the back-end ratio is 36%, though some programs (like FHA loans) may allow up to 43% or even 50% in specific circumstances.

Credit Score and Its Impact on Purchasing Power

Your credit score is a numerical representation of your reliability as a borrower. It doesn’t just determine if you qualify, but at what cost. A higher credit score typically translates to a lower interest rate.

Even a 1% difference in your interest rate can shift your qualification limit by tens of thousands of dollars. For instance, on a 30-year fixed mortgage, a borrower with a 760 score might qualify for a much higher loan amount than someone with a 620 score, simply because a larger portion of the monthly payment for the lower-score borrower is being eaten up by interest rather than the principal.

Employment History and Income Stability

Lenders look for “stable and predictable” income. Generally, they prefer to see at least two years of consistent employment in the same field. If you are a W-2 employee, this is straightforward. However, for the self-employed or those with commission-based roles, lenders will often average the last two years of tax returns. They want to ensure that the income you’re using to qualify isn’t a temporary windfall but a sustainable flow that can support a 15- or 30-year commitment.

The Role of the Down Payment and Loan Types

The amount of cash you can bring to the closing table significantly influences your mortgage qualification. The down payment acts as an immediate equity stake, reducing the lender’s risk and potentially opening doors to different loan products.

How Down Payment Size Affects Loan-to-Value (LTV)

The Loan-to-Value (LTV) ratio is the amount of the loan compared to the appraised value of the property. If you put 20% down, your LTV is 80%. A lower LTV is viewed as lower risk. If you have a substantial down payment, lenders may be more flexible with other qualifying factors, such as a slightly higher DTI or a thinner credit file. Furthermore, reaching the 20% threshold allows you to avoid Private Mortgage Insurance (PMI), which lowers your monthly cost and increases the total loan amount you can afford.

Conventional vs. Government-Backed Loans

The “how much” also depends on the type of loan you choose.

- Conventional Loans: These usually require higher credit scores and offer competitive rates but may have stricter DTI requirements.

- FHA Loans: Insured by the Federal Housing Administration, these are designed for borrowers with lower credit scores or smaller down payments (as low as 3.5%). Because the criteria are more lenient, you might “qualify” for a higher amount through an FHA loan than a conventional one, though you must factor in the cost of mortgage insurance premiums.

- VA and USDA Loans: For veterans or those buying in specific rural areas, these loans often require 0% down. This significantly increases the purchasing power for those who have the income to support a mortgage but lack the liquid savings for a down payment.

The Impact of Private Mortgage Insurance (PMI)

If your down payment is less than 20%, you will likely be required to pay PMI. This is an additional monthly fee that protects the lender if you default. When calculating how much you qualify for, you must subtract the cost of PMI from your total monthly allotment for housing. This effectively lowers your maximum home price, as a portion of your “buying power” is redirected toward insurance rather than the home itself.

Understanding the “All-In” Cost: Beyond the Principal

One of the most common mistakes prospective buyers make is equating a mortgage payment solely with principal and interest. Lenders, however, calculate your qualification based on the “PITI” (Principal, Interest, Taxes, and Insurance).

Property Taxes and Homeowners Insurance

These vary wildly by location. A $400,000 home in a state with high property taxes will require a much higher monthly payment than the same priced home in a low-tax state. When a lender determines your qualification, they estimate these costs. If you are looking at a home in a high-tax district or a flood zone that requires expensive additional insurance, your qualifying loan amount will decrease accordingly.

Homeowners Association (HOA) Fees

If you are looking at condos, townhomes, or certain planned communities, HOA fees are a mandatory part of your monthly debt. Lenders treat HOA fees exactly like a car payment or a student loan—they are added to your DTI. A $500 monthly HOA fee can reduce your mortgage borrowing power by nearly $70,000 to $100,000, depending on current interest rates.

Closing Costs and Cash Reserves

Qualification isn’t just about the monthly payment; it’s about the “cash to close.” Usually, closing costs range from 2% to 5% of the home’s purchase price. Some loan programs also require you to have “reserves”—liquid cash equivalent to two or three months of mortgage payments—remaining in your account after the house is bought. If you don’t have enough cash to cover both the down payment and closing costs, you may have to settle for a lower-priced home, even if your income suggests you can afford more.

Strategies to Increase Your Qualifying Amount

If your initial pre-qualification comes back lower than you hoped, there are several financial levers you can pull to increase your purchasing power. These strategies focus on optimizing your financial profile to appear as low-risk as possible to the lender.

Aggressive Debt Reduction

Since DTI is a ratio, you can improve it by either increasing your income or decreasing your debt. Paying off a car loan or a high-balance credit card can drastically change your DTI. For example, if you have a $400 monthly car payment, eliminating that debt could potentially allow you to qualify for an additional $50,000 to $60,000 in mortgage principal.

Boosting Your Credit Profile

Before applying for a mortgage, spend six months to a year optimizing your credit. This includes ensuring all payments are made on time, keeping credit card utilization below 10%, and avoiding any new credit inquiries. Moving from a “Good” credit tier to an “Excellent” tier can lower your interest rate, which in turn lowers your monthly payment and allows you to qualify for a larger loan amount.

Adding a Co-Borrower

If your individual income isn’t sufficient to qualify for the home you want, adding a co-borrower (such as a spouse or partner) can help. The lender will combine both incomes to calculate the DTI. However, be aware that lenders typically use the lower of the two borrowers’ middle credit scores when determining the interest rate.

Conclusion: Balancing Qualification with Affordability

There is a significant difference between what a bank says you can borrow and what you should borrow. Qualification is based on gross income, but you live on your net (after-tax) income. While a lender might qualify you for a certain amount based on a 43% DTI, your personal lifestyle—including travel, hobbies, and retirement savings—might dictate a much lower threshold.

The key to a successful mortgage experience is to use the qualification process as a ceiling, not a target. By understanding the mechanics of DTI, credit scores, and PITI, you can enter the market with a clear-eyed view of your financial standing, ensuring that your new home remains a source of wealth rather than a financial burden. Always consult with a qualified mortgage professional to get a tailored pre-approval, which remains the most accurate way to answer the question: “How much do I qualify for?”

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.