Navigating the world of personal finance often feels like deciphering a complex code, especially when it comes to borrowing. Whether you are eyeing a first home, a new vehicle, or a personal loan for debt consolidation, the first question that inevitably arises is: “How much can I actually borrow?”

While many people approach banks with a specific number in mind, lenders operate on a rigid set of mathematical formulas and risk assessments. This is where a “how much loan can I qualify for” calculator becomes an indispensable tool. These digital resources allow you to input your financial data and receive an estimate of your borrowing power before you ever take a hit to your credit score with a formal application. However, to use these tools effectively, one must understand the financial pillars that hold them up.

Understanding the Mechanics: How Loan Qualification Calculators Work

A loan qualification calculator is more than just a simple subtraction tool. It is an algorithmic representation of a lender’s risk appetite. By entering your income, debts, and potential interest rates, these calculators simulate the underwriting process used by major financial institutions.

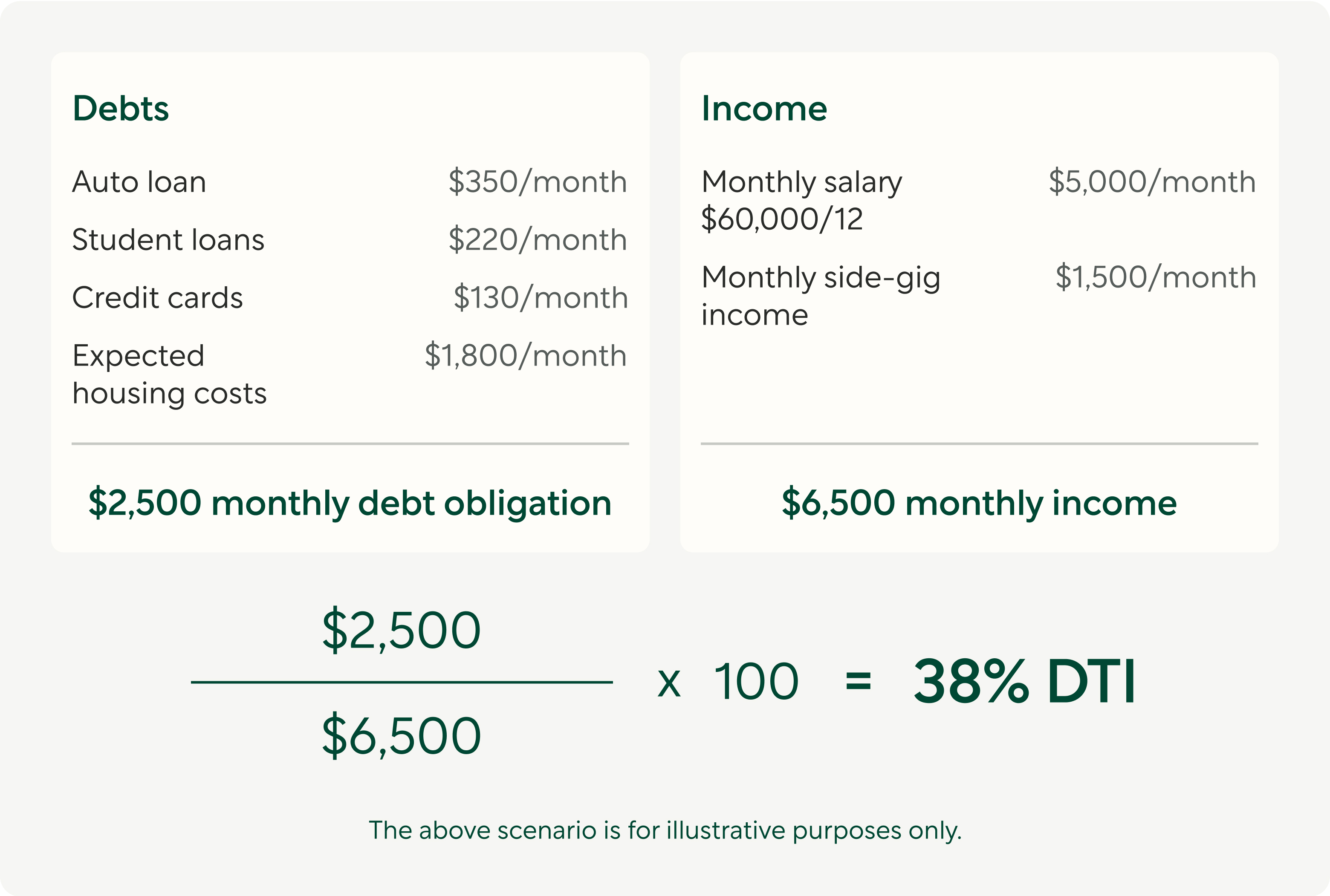

Debt-to-Income (DTI) Ratio: The Magic Number

The primary metric used by almost every loan calculator is the Debt-to-Income (DTI) ratio. This is the percentage of your gross monthly income that goes toward paying your monthly debt obligations. Lenders typically look for a DTI ratio below 36%, although some mortgage programs allow for up to 43% or even 50% in specific circumstances. A calculator takes your total monthly debt (credit cards, student loans, car payments) and compares it against your pre-tax income to determine how much “room” is left for a new loan payment.

The Role of Credit Scores in Borrowing Power

While a basic calculator might ask for your credit tier (Excellent, Good, Fair, or Poor), the reality is that your credit score acts as a multiplier for your loan capacity. A higher credit score qualifies you for lower interest rates. Because a lower interest rate reduces your monthly payment for the same principal amount, a borrower with an 800 credit score can technically “afford” a larger loan than a borrower with a 620 score, even if their incomes are identical.

Interest Rates and Term Lengths

Calculators also factor in the current market interest rates and the “term” or duration of the loan. A 30-year mortgage will allow for a much higher loan amount than a 15-year mortgage because the payments are spread out over a longer period, reducing the monthly burden on your DTI ratio. However, it is crucial to remember that a longer term usually means paying significantly more in total interest over the life of the loan.

Key Factors Influencing Your Maximum Loan Amount

Beyond the raw numbers you plug into a calculator, several qualitative and quantitative factors influence a lender’s final decision. Understanding these variables can help you adjust your expectations and financial habits before applying.

Gross Monthly Income vs. Net Income

Lenders calculate your qualification based on “Gross Monthly Income”—your earnings before taxes and deductions. This often leads to a common trap: a calculator might suggest you qualify for a $3,000 monthly mortgage payment, but after taxes, health insurance, and 401(k) contributions, your “take-home” pay might make that payment feel suffocating. It is vital to balance what a calculator says you can qualify for with what your actual budget can sustain.

Existing Debt Obligations

Not all debts are treated equally. Installment loans (like car payments) with a fixed end date are viewed differently than revolving debt (like credit cards). If you have high credit card balances, even if you make the minimum payments, lenders see high “utilization,” which signals risk. Most calculators require you to list these monthly obligations accurately to provide a realistic loan ceiling.

Employment History and Stability

A calculator cannot see your resume, but a lender will. Most traditional lenders require at least two years of consistent employment in the same field or a steady increase in responsibility and pay. If you have recently switched from a W-2 position to 1099 freelancing, a calculator might show you qualify based on income, but a lender might require two years of tax returns before approving the amount the calculator suggested.

Types of Loan Calculators and Which One You Need

Depending on your financial goal, the type of calculator you use matters. Each lending product has unique “guardrails” and requirements that a generic calculator might overlook.

Mortgage Qualification Calculators

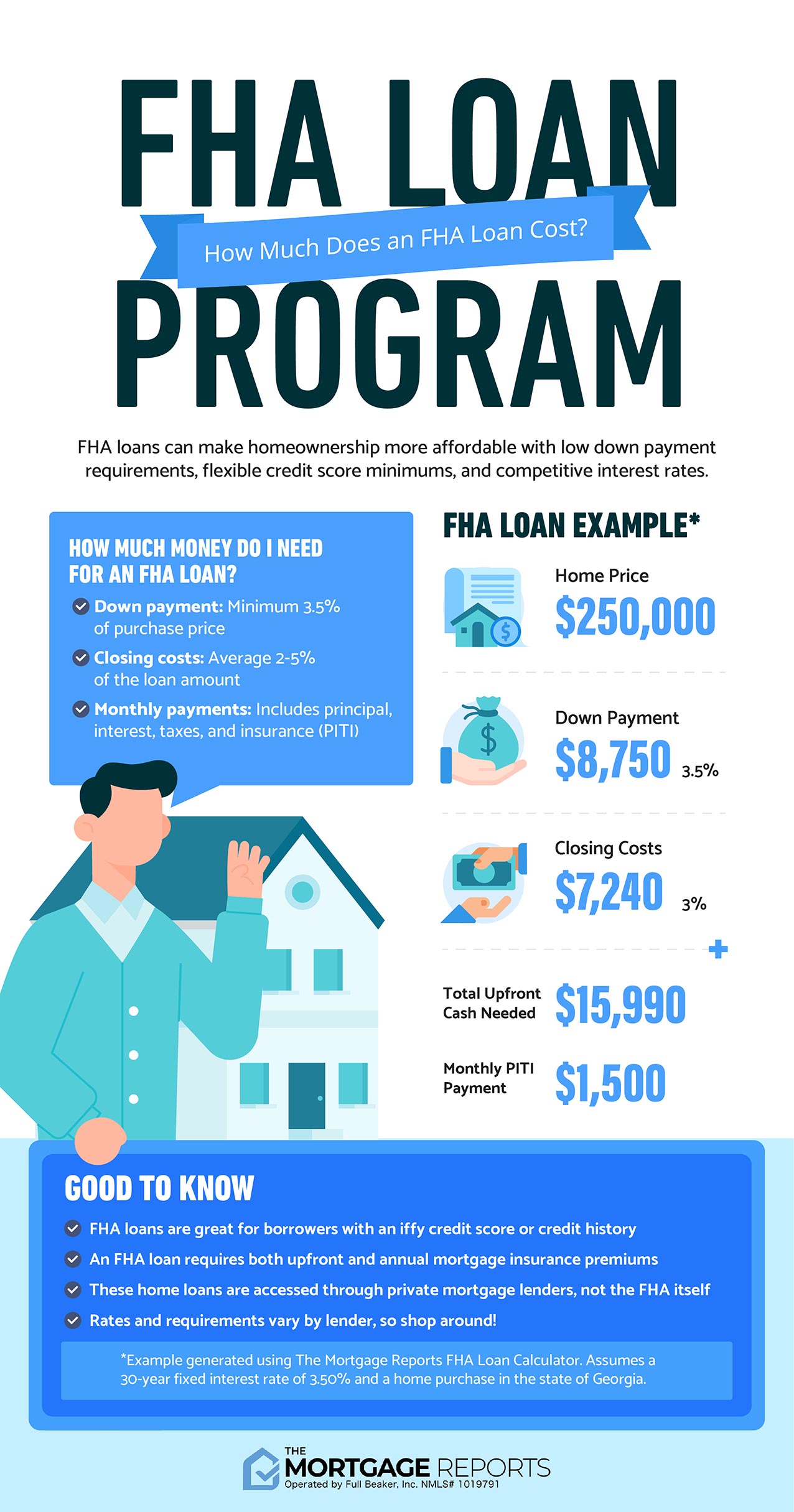

Mortgage calculators are the most complex. They must account for the “PITI” acronym: Principal, Interest, Taxes, and Insurance. Additionally, if you are putting down less than 20%, the calculator must factor in Private Mortgage Insurance (PMI). Some specialized mortgage calculators also include HOA (Homeowners Association) fees, which can significantly eat into your borrowing power in certain real estate markets.

Personal Loan and Auto Loan Estimators

These tools are generally more straightforward as they usually deal with shorter terms (3 to 7 years) and fixed interest rates. For auto loans, calculators often include a field for “trade-in value,” which acts as a down payment. Personal loan calculators are particularly useful for debt consolidation, helping you see if the new loan’s monthly payment is lower than the combined payments of your current high-interest debts.

Business Loan Eligibility Tools

For entrepreneurs, “how much can I qualify for” takes on a different meaning. These calculators focus on Debt Service Coverage Ratio (DSCR) rather than personal DTI. They look at the business’s annual net operating income compared to its annual debt payments. If you are looking for a business loan, ensure the tool you are using is designed for commercial lending, as the criteria are vastly different from consumer finance.

How to Improve Your Qualification Odds Before Applying

If the calculator provides a number that is lower than you hoped for, do not despair. There are several strategic moves you can make to “prime the pump” and increase your borrowing capacity over a period of three to six months.

Reducing Your Debt Load

The fastest way to increase the loan amount you qualify for is to lower your monthly debt payments. Paying off a small car loan or aggressive credit card debt directly improves your DTI ratio. For every $100 you remove from your monthly debt obligations, you potentially add tens of thousands of dollars to your mortgage borrowing power.

Boosting Your Credit Score Effectively

Check your credit report for errors. Inaccuracies in reported late payments or outdated debt can artificially suppress your score. By correcting these, you might move from a “Fair” interest rate bracket to a “Good” one, which directly lowers the cost of borrowing and increases the total loan amount the calculator will display.

The Impact of a Larger Down Payment

While it doesn’t technically increase the “loan amount” you qualify for in terms of debt, a larger down payment increases your “purchase power.” Furthermore, putting more money down reduces the lender’s “Loan-to-Value” (LTV) ratio. A lower LTV often results in better interest rates and the removal of insurance requirements like PMI, making the overall loan more affordable.

Moving Beyond the Calculator: The Human Element of Lending

While digital calculators provide an excellent baseline, they are ultimately simulations. The actual lending process involves a human element—or at least a more sophisticated AI underwriting system—that looks at the nuances of your financial life.

Manual Underwriting vs. Automated Systems

In some cases, especially for those with “thin” credit files or non-traditional income sources, a manual underwriter will review the application. They may consider “compensating factors,” such as significant cash reserves (savings) or a long history of on-time rent payments, which a standard online calculator simply cannot factor in. If a calculator says “no,” a specialized lender might still say “yes” based on these nuances.

Preparing Your Documentation

To turn a calculator’s estimate into a reality, you must be prepared with documentation. This includes W-2s, 1099s, bank statements, and tax returns. The accuracy of the “how much loan can I qualify for” calculator is only as good as the data you provide. If you estimate your income or forget to mention a student loan, the final offer from the bank will differ significantly from your online estimate.

In conclusion, using a loan qualification calculator is a vital first step in any major financial journey. It provides a reality check, helps you set a budget, and highlights areas where you can improve your financial profile. By understanding DTI ratios, the impact of credit scores, and the specific requirements of different loan types, you can move from the “estimation” phase to the “approval” phase with confidence and clarity. Remember, the goal isn’t just to qualify for the most money possible, but to qualify for a loan that fits comfortably within a healthy, long-term financial plan.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.