For anyone venturing into the world of personal finance and investing, the term “S&P 500” is perhaps the most ubiquitous phrase they will encounter. It is frequently cited on evening news broadcasts, referenced by financial advisors as the “gold standard” for market performance, and served as the foundation for millions of retirement accounts worldwide. But what is it exactly? More than just a list of names or a ticker moving across a screen, the Standard & Poor’s 500 Index represents the heartbeat of American capitalism and the primary vehicle through which modern investors build long-term wealth.

In the realm of money and finance, understanding the S&P 500 is not merely an academic exercise; it is a fundamental requirement for making informed decisions about your capital. This guide explores the mechanics, the strategic importance, and the practical methods of utilizing the S&P 500 to secure your financial future.

Decoding the S&P 500: Mechanics and Methodology

At its simplest level, the S&P 500 is a stock market index that tracks the performance of 500 of the largest companies listed on stock exchanges in the United States. Created in its modern form in 1957, it was the first computer-weighted stock market index, and today it covers approximately 80% of the available market capitalization of the U.S. equity market.

What Exactly is a Market Index?

A market index is essentially a statistical measure of a section of the stock market. Think of it as a “sample platter” or a “basket” that represents the whole. Instead of tracking the thousands of individual companies trading on the New York Stock Exchange (NYSE) or the Nasdaq, investors look at an index like the S&P 500 to get a quick snapshot of how the economy and the corporate sector are performing. If the S&P 500 is “up,” it generally means that the largest engines of the American economy are thriving.

The Power of Market Cap Weighting

Unlike the Dow Jones Industrial Average, which is price-weighted (meaning a stock with a higher share price has more influence), the S&P 500 is float-adjusted market capitalization-weighted. In this system, the “weight” or influence of a company is determined by its total market value—the share price multiplied by the number of shares available for public trading.

This means that massive corporations like Apple, Microsoft, and Amazon have a significantly larger impact on the index’s movement than smaller members. For an investor, this methodology is logical because it ensures that the index reflects the actual economic weight of these giants within the marketplace.

The Selection Criteria: Who Gets In?

It is a common misconception that the S&P 500 simply consists of the 500 largest companies in America. In reality, the index is maintained by the S&P Dow Jones Indices, and a committee decides which companies are included based on strict eligibility criteria.

- Market Cap: A company must have an unadjusted market cap of $14.5 billion or greater (though this number is periodically updated).

- Liquidity: The stock must be highly liquid, meaning it is easy to buy and sell without moving the price significantly.

- Profitability: The company must have reported positive earnings over the most recent quarter and the sum of the previous four quarters.

- Domicile: It must be a U.S. company.

This “curation” ensures that the index remains a high-quality representation of the leading edge of the U.S. business landscape.

The Strategic Importance of the S&P 500 in Personal Finance

For the individual investor, the S&P 500 serves two primary roles: it is a benchmark for performance and a core building block for a diversified portfolio. Understanding why this index is so revered allows you to move past the noise of daily market fluctuations and focus on long-term wealth creation.

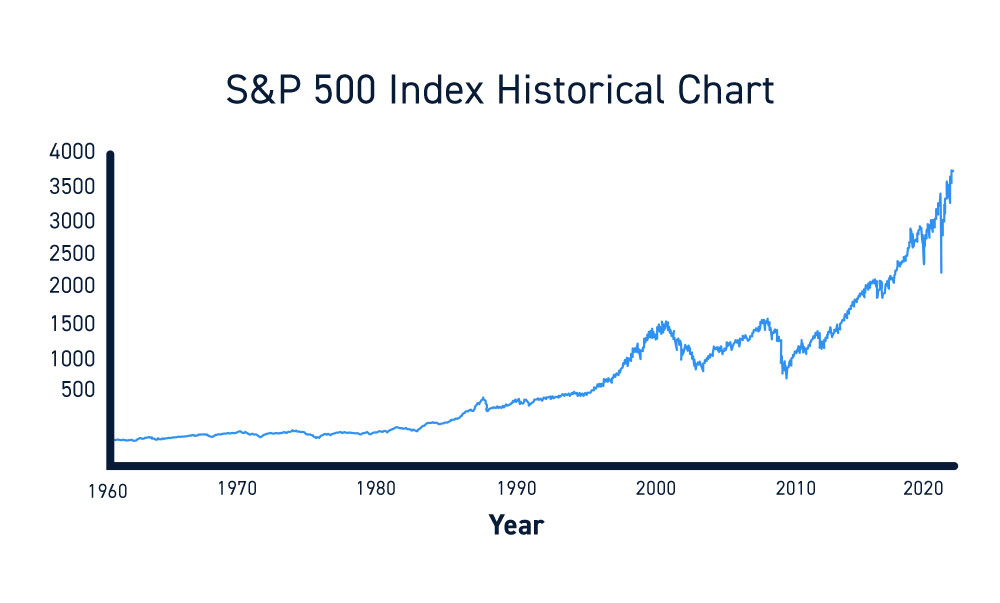

Historical Performance and the 10% Rule

One of the most compelling reasons money managers focus on the S&P 500 is its historical track record. Over the last several decades, the index has provided an average annual return of approximately 10% before inflation. While there are years where the market drops significantly (such as 2008 or 2022), the long-term trajectory has been consistently upward.

For a personal finance strategy, this historical reliability is vital. It allows for the “magic” of compound interest to take hold. An investor who consistently puts money into an S&P 500-tracking fund often finds that their wealth grows exponentially over twenty or thirty years, simply by capturing the broad growth of the U.S. corporate sector.

Diversification Across the 11 GICS Sectors

Risk management is the cornerstone of successful investing, and the S&P 500 offers “built-in” diversification. The index is divided into 11 Global Industry Classification Standard (GICS) sectors, including:

- Information Technology

- Health Care

- Financials

- Consumer Discretionary

- Communication Services

- Industrials

- Consumer Staples

- Energy

- Utilities

- Real Estate

- Materials

By owning the S&P 500, you aren’t just betting on tech or banking; you are betting on the collective ingenuity of the entire American economy. If one sector, like Energy, is struggling due to low oil prices, another sector, like Technology or Health Care, may be booming, helping to stabilize the overall value of your investment.

The “Buffett” Endorsement of Passive Investing

Warren Buffett, arguably the greatest investor of all time, has famously advocated for the S&P 500 for the average person. He argues that most people (and even most professional money managers) cannot consistently “beat the market” by picking individual stocks. In his 2013 letter to shareholders, he instructed that his wife’s inheritance be invested 90% in a very low-cost S&P 500 index fund. This endorsement highlights a key financial truth: for most people, the most efficient way to grow wealth is to stop trying to outsmart the market and simply “own” the market.

How to Invest: Turning Knowledge into Wealth

Knowing what the S&P 500 is represents the first step; the second is implementation. In the modern era of financial tools, accessing this index has never been easier or more cost-effective.

Index Funds vs. ETFs

There are two primary ways to invest in the S&P 500: Mutual Funds and Exchange-Traded Funds (ETFs).

- S&P 500 Index Mutual Funds: These are priced once at the end of the trading day. They are excellent for automated investing, where you set a specific dollar amount to be deducted from your bank account every month.

- S&P 500 ETFs: These trade like individual stocks on an exchange throughout the day. Popular examples include the SPDR S&P 500 ETF Trust (SPY), the Vanguard S&P 500 ETF (VOO), and the iShares Core S&P 500 ETF (IVV). ETFs are often preferred for their tax efficiency and lower entry costs.

The Critical Role of Expense Ratios

In the world of money, fees are the silent killer of returns. One of the greatest advantages of S&P 500 funds is their incredibly low “expense ratios.” Because these funds are “passively managed”—meaning a human isn’t sitting there deciding which stocks to buy and sell every day—the cost to run them is minimal.

Major providers like Vanguard or Fidelity offer S&P 500 funds with expense ratios as low as 0.03% or even 0.015%. This means for every $10,000 you invest, you might only pay $1.50 to $3.00 per year in fees. Compared to actively managed funds that charge 1.0% or more, this difference can result in hundreds of thousands of dollars more in your pocket over a lifetime of investing.

Dollar-Cost Averaging (DCA)

A common mistake in personal finance is trying to “time the market”—waiting for a dip to buy. However, because the S&P 500 represents 500 different companies, timing it perfectly is nearly impossible. A more effective strategy is Dollar-Cost Averaging. This involves investing a fixed amount of money at regular intervals, regardless of whether the index is up or down. When prices are high, your money buys fewer shares; when prices are low, your money buys more. Over time, this lowers your average cost per share and removes the emotional stress of market volatility.

Risks and Limitations: A Balanced Perspective

While the S&P 500 is a powerful tool, a professional approach to finance requires acknowledging its limitations. No investment is without risk, and the S&P 500 is no exception.

Concentration Risk and the “Magnificent Seven”

Because the index is market-cap weighted, it has become increasingly “top-heavy” in recent years. A handful of massive tech companies—often referred to as the “Magnificent Seven” (including Nvidia, Microsoft, and Apple)—now make up a significant percentage of the index’s total value.

The risk here is that if the tech sector faces a systemic downturn or regulatory crackdown, the entire S&P 500 will suffer, even if the other 493 companies are doing well. Investors should be aware that when they buy the S&P 500, they are heavily exposed to the valuation and performance of the technology industry.

Market Volatility and Macro Factors

The S&P 500 is a “paper asset,” meaning its value can fluctuate wildly based on investor sentiment, interest rate changes by the Federal Reserve, or geopolitical events. It is not uncommon for the index to see “corrections” (drops of 10%) or “bear markets” (drops of 20% or more). For an investor with a short-term horizon—such as someone needing their money in two years for a house down payment—the S&P 500 may be too volatile. It is best suited for capital that can remain invested for at least five to ten years.

The Absence of Small-Cap and International Exposure

While the S&P 500 covers the titans of U.S. industry, it excludes small-cap companies (which often have higher growth potential) and international markets. Many of the world’s fastest-growing economies are outside the U.S. Therefore, while the S&P 500 is a fantastic “core” holding, a truly sophisticated financial plan might supplement it with exposure to international stocks or smaller domestic companies to ensure a truly global diversification strategy.

Conclusion: The Bedrock of Financial Independence

The S&P 500 is more than just a number on a screen; it is a testament to the enduring growth of the modern economy. For the individual focused on “Money”—whether that means saving for retirement, building a legacy, or achieving early financial independence—the index provides a transparent, low-cost, and historically proven pathway to success.

By understanding how the index is constructed, why it has historically performed so well, and how to access it through low-cost ETFs and mutual funds, you move from being a spectator of the economy to a participant in its growth. While it requires patience to endure the inevitable market cycles, the S&P 500 remains one of the most effective tools ever created for turning consistent savings into substantial wealth. In the journey toward financial freedom, the S&P 500 isn’t just an option; for many, it is the most logical starting point.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.