Purchasing a vehicle is one of the most significant financial decisions the average consumer will make, second only to buying a home. However, unlike real estate, which has the potential to appreciate, a vehicle is a rapidly depreciating asset. For many, the question “How much vehicle can I afford?” is often answered by a dealership’s finance office based on the maximum monthly payment a borrower can sustain. This is a narrow and often dangerous way to view personal mobility.

To truly understand affordability, one must look beyond the sticker price and the monthly installment. True affordability is a calculation of cash flow, opportunity cost, and long-term wealth impact. This guide explores the foundational financial frameworks, the hidden costs of ownership, and the strategic considerations necessary to ensure your next car purchase accelerates your life rather than stalling your financial future.

The Foundation of Affordability: The 20/4/10 Rule

In the world of personal finance, the “20/4/10 rule” serves as a gold standard for vehicle budgeting. While individual circumstances may allow for some flexibility, these three pillars provide a defensive barrier against becoming “car poor”—a state where a disproportionate amount of your income is swallowed by an oxidizing asset.

The 20% Down Payment

The first component of the rule is the 20% down payment. In an era of “zero-down” financing, this may seem outdated, but its purpose is twofold: equity and risk mitigation. Vehicles lose a significant portion of their value the moment they are driven off the lot. By putting 20% down, you ensure that you have immediate equity in the car. This prevents you from being “underwater” or “upside down” on your loan, where you owe the bank more than the car is worth. If you need to sell the vehicle unexpectedly or if it is totaled in an accident, having that equity buffer protects you from having to pay the bank out of pocket to settle the debt.

The 4-Year Loan Term

While 72-month and even 84-month (7-year) loans are becoming increasingly common, they are generally symptoms of buying “too much car.” A longer loan term lowers the monthly payment, making a luxury vehicle appear affordable on a modest income. However, long-term loans result in significantly higher interest costs and increase the likelihood that you will still be paying for the car long after the bumper-to-bumper warranty has expired. Limiting your loan to 48 months (4 years) ensures that you are paying off the principal at a rate that stays ahead of the vehicle’s depreciation curve.

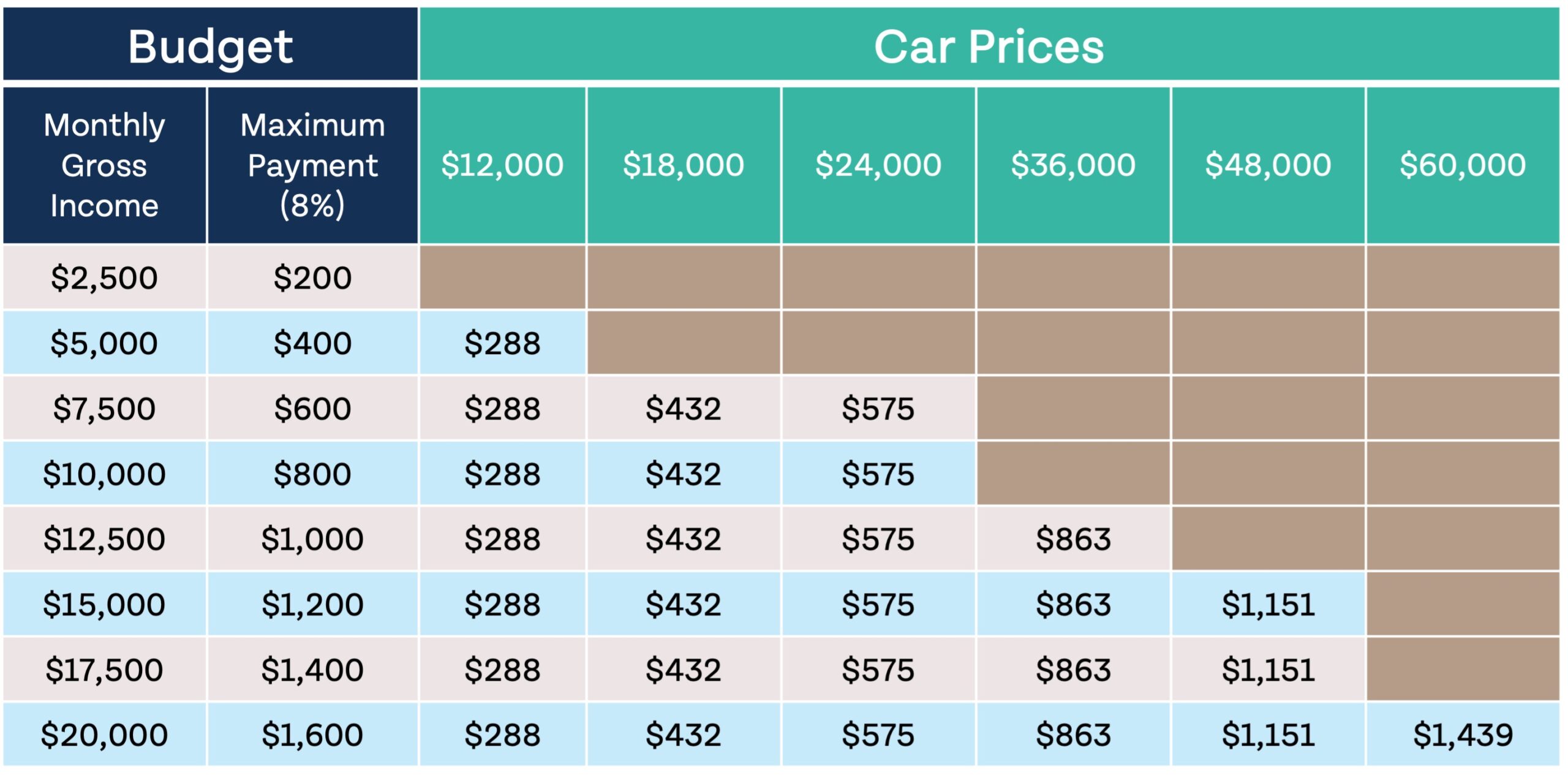

The 10% Monthly Income Limit

The final pillar states that your total transportation costs—including the loan payment, insurance, and fuel—should not exceed 10% of your gross monthly income. Some experts argue for 10% of net (take-home) income for a more conservative approach. By capping your spending at this level, you ensure that you have sufficient capital remaining for essential goals, such as retirement contributions, emergency fund building, and housing costs. If a $60,000 SUV requires 25% of your monthly income, you aren’t just buying a car; you are sacrificing your future financial independence for a leather interior.

Beyond the Monthly Payment: Calculating Total Cost of Ownership (TCO)

The “affordability” of a vehicle is not dictated solely by the check you write to the lender. The Total Cost of Ownership (TCO) encompasses every dollar that leaves your pocket as a result of owning that specific vehicle. Ignoring these variables is a common mistake that can lead to a monthly budget deficit.

Insurance and Registration

Insurance premiums vary wildly depending on the vehicle’s safety rating, theft rates, and repair costs. A high-performance sports car may have a similar monthly payment to a sturdy SUV, but the insurance premiums for the former could be double. Before signing a purchase agreement, it is vital to get an insurance quote for the specific VIN or model. Furthermore, registration fees and annual property taxes on vehicles vary by state and are often based on the vehicle’s current value. For a new luxury vehicle, these annual “hidden” costs can amount to thousands of dollars.

Maintenance, Repairs, and Fuel

Every vehicle has a different maintenance profile. A budget-friendly sedan might require inexpensive oil changes and standard tires, while a European luxury car may require specialized synthetic oils, premium fuel, and tires that cost $400 each. As a vehicle ages, the cost of “unscheduled maintenance” (repairs) increases. If you are buying a used vehicle to save on the purchase price, you must allocate a larger portion of your budget to a repair fund. A vehicle you can “afford” is one where a $1,200 alternator failure is an inconvenience, not a financial catastrophe.

Depreciation: The Silent Wealth Killer

Depreciation is the single largest cost of vehicle ownership, yet it is often ignored because it doesn’t result in a monthly bill. Most new cars lose 15% to 20% of their value in the first year and roughly 60% of their value over five years. When you calculate how much vehicle you can afford, you must consider the “resale value.” Buying a vehicle that holds its value well (such as certain trucks or high-reliability brands) means that your net cost of ownership over five years might be lower than a cheaper vehicle that depreciates to near zero.

Strategic Financing and the New vs. Used Dilemma

Once you have established your budget based on the 20/4/10 rule and TCO, the next step is determining the most efficient way to deploy your capital. This involves evaluating the current interest rate environment and the value proposition of different vehicle ages.

Credit Scores and Interest Rates

Your credit score is the primary lever in determining the cost of your loan. A buyer with a “Tier 1” credit score (usually 740+) may qualify for promotional 0.9% or 1.9% APR financing from a manufacturer. At these rates, the cost of borrowing is negligible, making it financially savvy to keep your cash invested in the market while using the bank’s money. Conversely, a buyer with a subprime score might face interest rates of 12% to 20%. At those rates, the interest alone can add $10,000 or more to the cost of a modest vehicle. If your credit score is low, the amount of vehicle you can “afford” drops significantly because so much of your payment is going toward interest rather than the car itself.

The Used Market and Certified Pre-Owned (CPO)

Traditionally, the “smart money” move was to buy a two-to-three-year-old vehicle to avoid the initial depreciation hit. While market fluctuations sometimes narrow the gap between new and used prices, the principle generally holds: someone else has already paid for the steepest part of the depreciation curve. Certified Pre-Owned (CPO) programs offer a middle ground, providing manufacturer-backed warranties that mitigate the risk of buying used. When calculating affordability, a three-year-old vehicle often allows you to move “up” in quality or features while staying within the same financial footprint as a base-model new car.

Leasing: Is it Ever the Right Choice?

Leasing is often marketed as a way to get more car for less money per month, but it is effectively a long-term rental of the vehicle’s most expensive years of life. From a pure wealth-building perspective, leasing is rarely the optimal choice because you never build equity and are locked into a cycle of perpetual payments. However, for business owners who can deduct lease payments or individuals who prioritize driving a new vehicle every three years and are willing to pay a premium for that lifestyle, it can be factored into a budget—provided the total cost still fits within the 10% income rule.

Integrating the Vehicle into Your Broader Financial Strategy

Ultimately, a vehicle is a tool meant to facilitate your life, not a status symbol meant to define it. To determine how much you can truly afford, you must look at your balance sheet holistically.

Opportunity Cost and Investing

Every dollar spent on a car is a dollar that isn’t being invested in the stock market, a business, or real estate. If you choose a $600 monthly car payment over a $300 payment, that $300 difference, if invested in an index fund yielding 7% annually, would grow to over $52,000 over 10 years. When you ask “How much vehicle can I afford?”, you should also ask “What am I giving up in 10 years to drive this today?” For those early in their careers, prioritizing a reliable, low-cost vehicle can result in hundreds of thousands of dollars in additional wealth by retirement due to the power of compound interest.

The Importance of the Emergency Fund

You cannot afford a vehicle—no matter how low the payment—if you do not have a liquid emergency fund. If a job loss or medical emergency occurs, a car payment becomes an immediate liability. Before committing to a new vehicle purchase, ensure you have 3 to 6 months of living expenses saved. This ensures that your vehicle doesn’t become the reason for a financial collapse during a period of volatility.

In conclusion, “how much vehicle you can afford” is a question of discipline over desire. By adhering to the 20/4/10 rule, accounting for the total cost of ownership, and respecting the opportunity cost of your capital, you can make a purchase that provides reliable transportation without compromising your long-term financial security. True luxury isn’t driving the most expensive car in the neighborhood; it’s the peace of mind that comes from knowing your vehicle is a well-managed line item in a thriving financial plan.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.