Budgeting is often perceived as a financial straitjacket—a restrictive set of rules designed to sap the joy out of spending. In reality, a well-constructed budget is the ultimate tool for financial freedom. It provides a roadmap for your money, ensuring that your resources are allocated toward the things that truly matter to you, rather than disappearing into a void of impulse purchases and overlooked subscriptions.

To master your finances, you must move beyond the idea of “tracking spending” and embrace the concept of “intentional allocation.” This guide explores the strategic frameworks, practical steps, and psychological shifts required to create a budget that doesn’t just look good on paper but actually transforms your financial life.

The Foundations of Financial Clarity

Before you can determine where your money should go, you must have an unflinching understanding of where it currently is. Budgeting is not a one-time event; it is a continuous process of assessment and adjustment.

Shifting the Mindset: Budgeting as a Tool, Not a Restriction

The primary reason most budgets fail is psychological. When we view a budget as a “diet” for our wallet, our natural instinct is to rebel against it. To succeed, you must reframe the budget as a value-based spending plan. Instead of thinking, “I can’t spend money on X,” think, “I am choosing to spend money on Y because it aligns with my long-term goals.” A budget gives you permission to spend without guilt on the things you value because you have already accounted for your obligations and savings.

Assessing Your Current Financial Health

Creating a budget without knowing your net worth and cash flow is like trying to navigate a new city without a map. Start by calculating your net income—the amount that actually hits your bank account after taxes and deductions. Next, conduct a “financial audit” by reviewing the last three months of bank and credit card statements. This historical data is crucial because it reveals the difference between what you think you spend and what you actually spend. Identify recurring fixed costs (rent, insurance, utilities) versus variable costs (dining out, entertainment, groceries).

Choosing the Right Budgeting Framework

There is no “one size fits all” approach to money management. The best budget is the one you can actually stick to. Depending on your personality and financial complexity, one of the following frameworks will likely serve you best.

The 50/30/20 Rule: Simplicity for Beginners

For those who find detailed spreadsheets overwhelming, the 50/30/20 rule offers a balanced, high-level approach. Under this model:

- 50% of income goes to Needs: Housing, utilities, basic groceries, and minimum debt payments.

- 30% goes to Wants: Dining out, travel, hobbies, and streaming services.

- 20% goes to Savings and Debt Repayment: Building an emergency fund, contributing to retirement accounts, or paying down high-interest debt.

This framework is effective because it forces you to prioritize savings while still allowing for a lifestyle that you enjoy.

Zero-Based Budgeting: Giving Every Dollar a Job

Zero-based budgeting is the gold standard for those who want total control over their cash flow. The goal is to ensure that your Income minus your Expenses equals exactly zero at the end of the month. This doesn’t mean you have zero dollars in your bank account; it means that every single dollar has been assigned a specific task—whether that is paying the electric bill, buying coffee, or being moved into a brokerage account. This method eliminates “leaky” spending where money simply vanishes into unaccounted-for categories.

The Pay-Yourself-First Method

Also known as “reverse budgeting,” this strategy prioritizes your future self above all else. Instead of budgeting for expenses and saving what is left over, you determine your savings goals first. Once you have automated your savings and debt payments, you are free to spend the remainder of your income however you wish. This is an excellent strategy for high-earners or those with relatively low fixed expenses who want to ensure they hit their investment targets without tracking every latte.

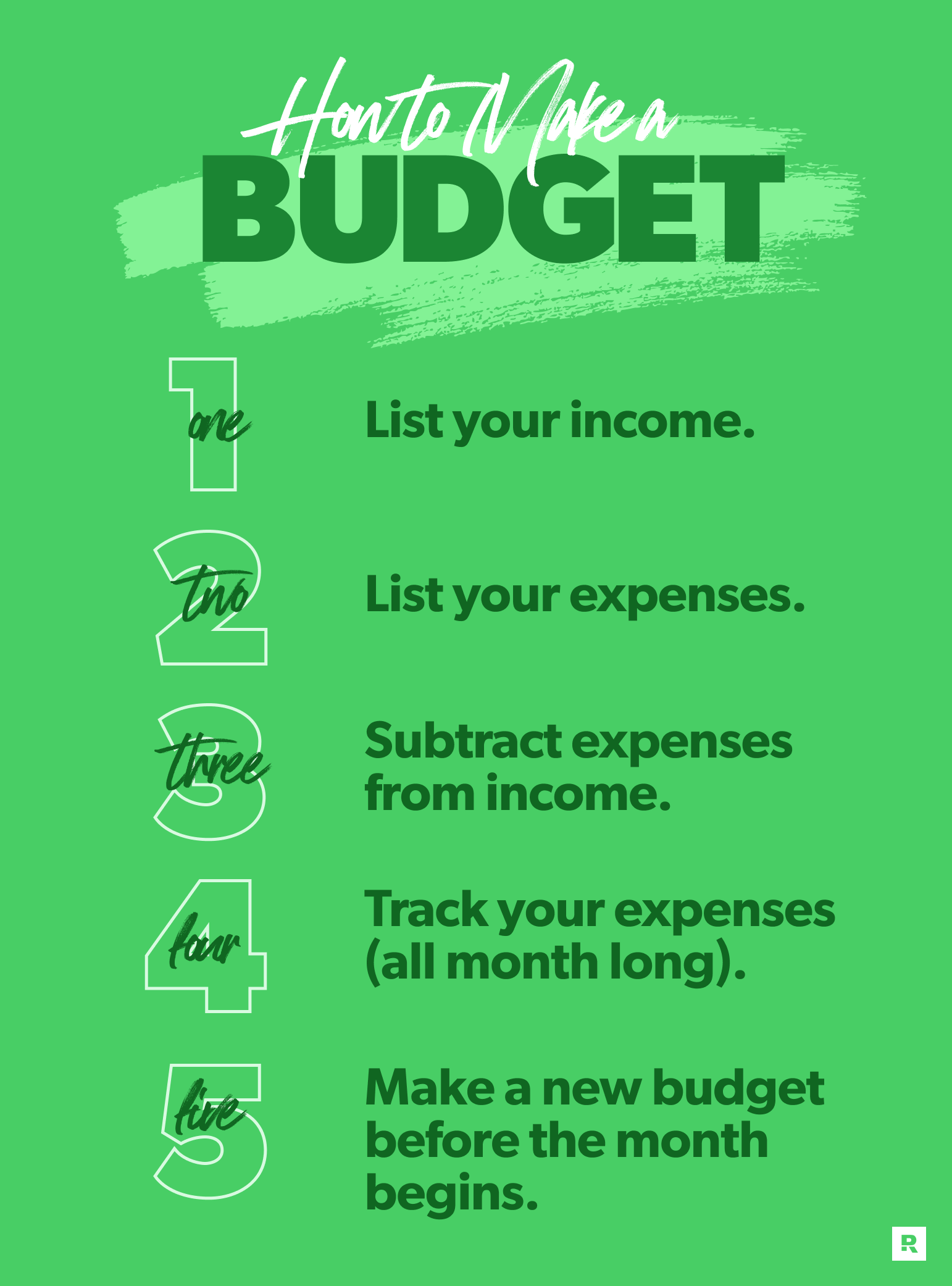

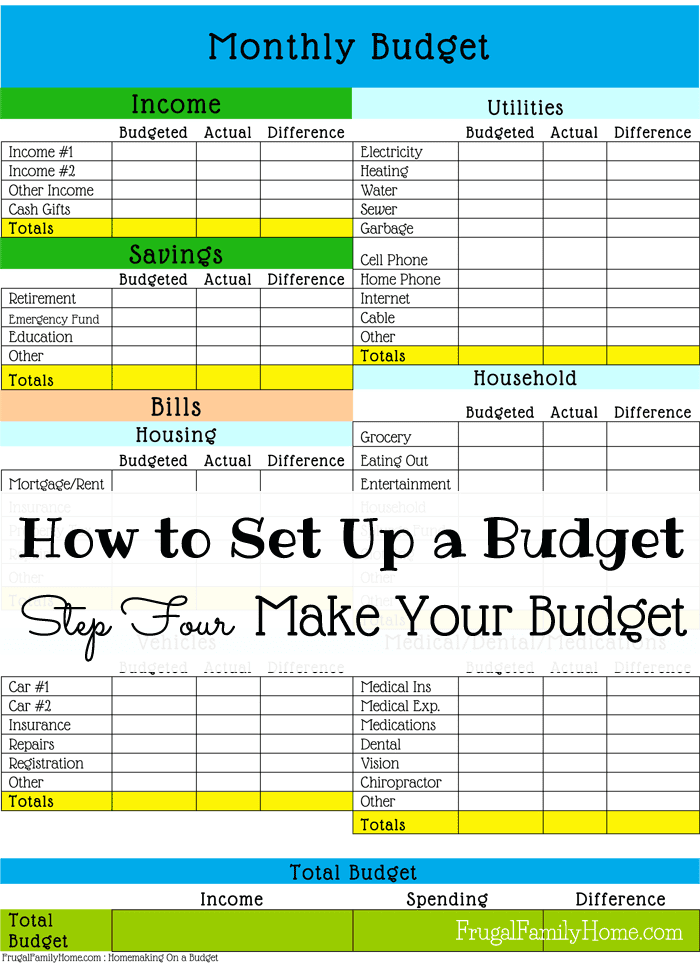

Step-by-Step Guide to Creating Your First Budget

Once you have selected a framework, it is time to build the actual budget. This requires a granular look at your lifestyle and a commitment to honest self-reflection.

Identifying Fixed vs. Variable Expenses

Start by listing your non-negotiables. Fixed expenses are the easiest to budget for because they rarely change: mortgage/rent, car payments, insurance premiums, and internet bills. Variable expenses are where the “battle” of the budget is won or lost. These include groceries, gas, and entertainment. To handle variable expenses, it is best to set a “cap” based on your historical averages and challenge yourself to stay under it.

Tracking Non-Monthly Costs

One of the most common budget-killers is the “surprise” expense that isn’t actually a surprise. These are annual or semi-annual costs like car registrations, holiday gifts, or annual software subscriptions. To manage these, use “sinking funds.” Calculate the total annual cost of these items, divide by 12, and set that amount aside each month in a separate savings account. When the bill arrives, the money is already there, preventing a budget crisis.

Establishing an Emergency Fund Buffer

A budget is a fragile thing without an emergency fund. Life is unpredictable—medical emergencies, car repairs, or sudden job loss can happen to anyone. A robust budget must include a line item for an emergency fund until you have at least three to six months of essential living expenses saved. This fund acts as insurance for your budget, ensuring that a single bad break doesn’t force you into high-interest debt.

Advanced Strategies for Budget Optimization

A budget is a living document. As your career progresses and your life changes, your financial strategy must evolve to remain effective.

Leveraging Financial Tools and Automation

While manual tracking is great for building awareness, automation is the key to long-term consistency. Set up automatic transfers to your savings and investment accounts to occur the same day you get paid. Use financial apps that sync with your bank accounts to categorize spending in real-time. By removing the “friction” of manual labor, you make it much harder to fail. However, be sure to review these automated systems monthly to ensure they still align with your goals.

Reviewing and Adjusting for Life Transitions

Major life events—marriage, the birth of a child, a promotion, or moving to a new city—require a total budget overhaul. A promotion, in particular, carries the risk of “lifestyle creep,” where your spending increases at the same rate as your income, leaving your net savings rate stagnant. When you receive a raise, consider the “50% rule”: allocate half of the increase to your lifestyle and the other half directly to your savings or debt repayment. This allows you to enjoy your success while accelerating your path to financial independence.

Balancing Debt Repayment with Wealth Building

A common dilemma in budgeting is whether to pay off debt or invest. The answer lies in the interest rates. High-interest debt (like credit cards) is a financial emergency and should be prioritized over almost all other goals. However, if you have low-interest debt (like a mortgage or some student loans), it may be mathematically superior to pay the minimum and invest your extra cash in the stock market, where historical returns may exceed the cost of the debt. A sophisticated budget balances these competing priorities to maximize your total net worth over time.

Conclusion: Consistency Over Perfection

The most important thing to remember about making a budget is that your first month will likely be a failure—and that’s okay. You will forget an expense, or an unexpected event will throw your numbers off. The goal of budgeting isn’t to be perfect; it’s to be aware.

By consistently reviewing your spending, choosing a framework that fits your lifestyle, and prioritizing your long-term goals over short-term impulses, you gain a level of power over your life that few people ever achieve. Money is a tool, and the budget is the instruction manual. When you master the manual, you master the tool, and when you master the tool, you can build whatever life you desire.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.