In the modern economic landscape, financial literacy is no longer a luxury—it is a survival skill. At the heart of financial literacy lies the budget. Contrary to popular belief, a budget is not a financial straightjacket designed to restrict your enjoyment of life; rather, it is a strategic roadmap that provides you with the freedom to spend without guilt and the security to face the future without fear. Creating a budget is the foundational step in transitioning from passive financial participation to active wealth management. This guide explores the intricate process of building a robust financial plan, ensuring your money works as hard for you as you do for it.

Establishing the Pillars of Your Financial Blueprint

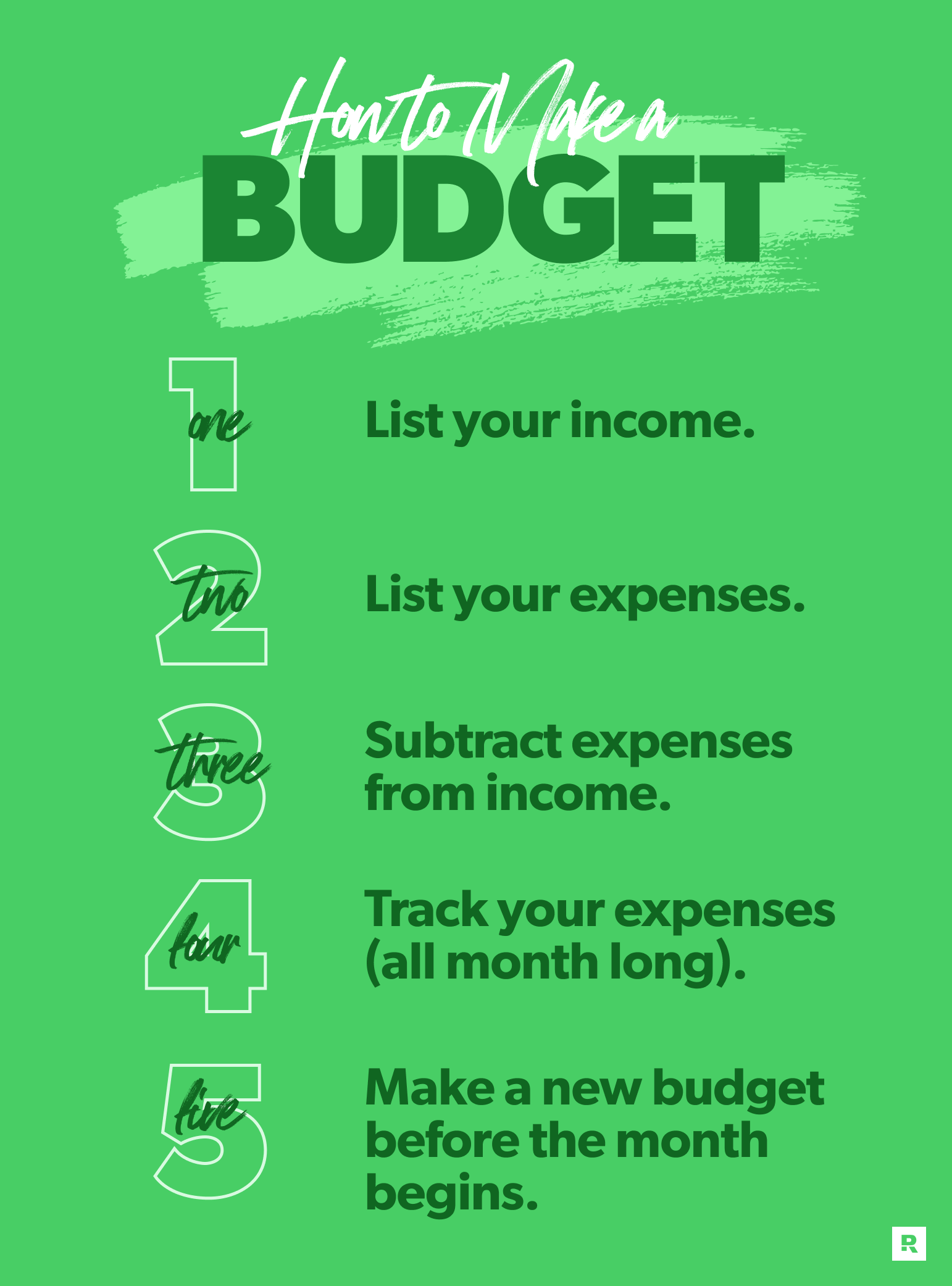

Before you can determine where your money should go, you must have an unflinching understanding of where it currently goes. The first pillar of budgeting is a comprehensive financial audit. This process involves more than just glancing at a bank statement; it requires a deep dive into your spending habits, income stability, and the psychological triggers that lead to discretionary spending.

Tracking Income vs. Total Expenses

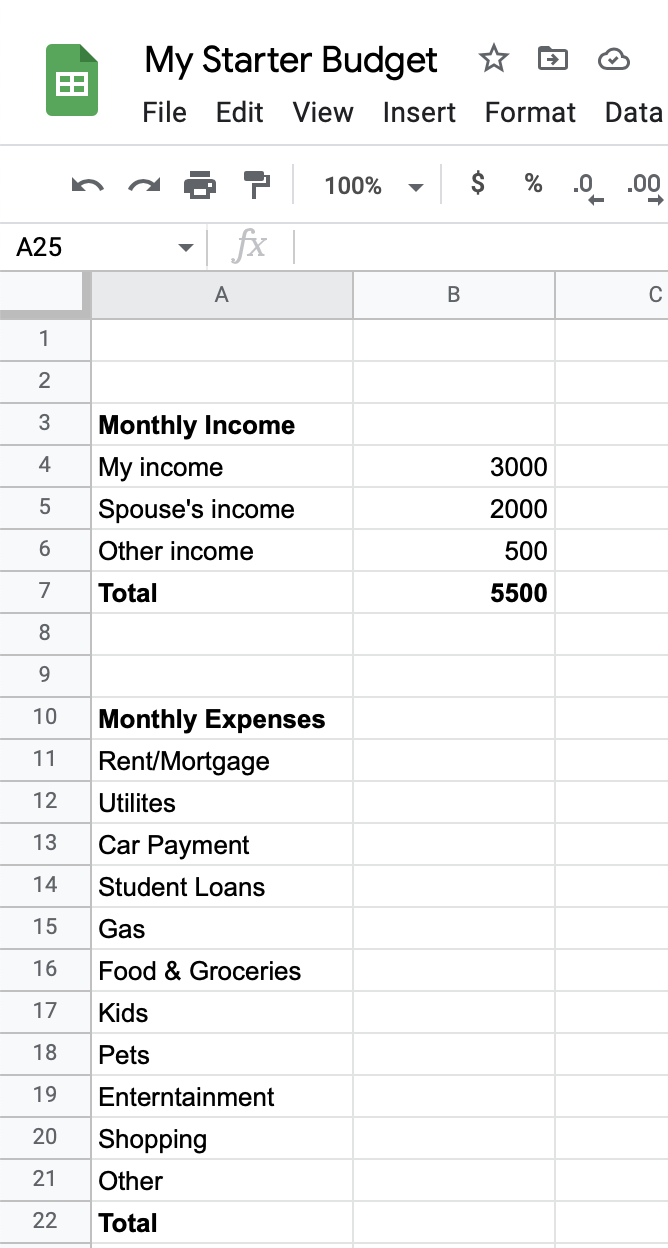

The most basic equation in finance is “Income – Expenses = Net Cash Flow.” To begin, document every source of income, including your primary salary, side hustles, dividends, and any passive income streams. Use your “take-home” pay (after-tax) as your baseline.

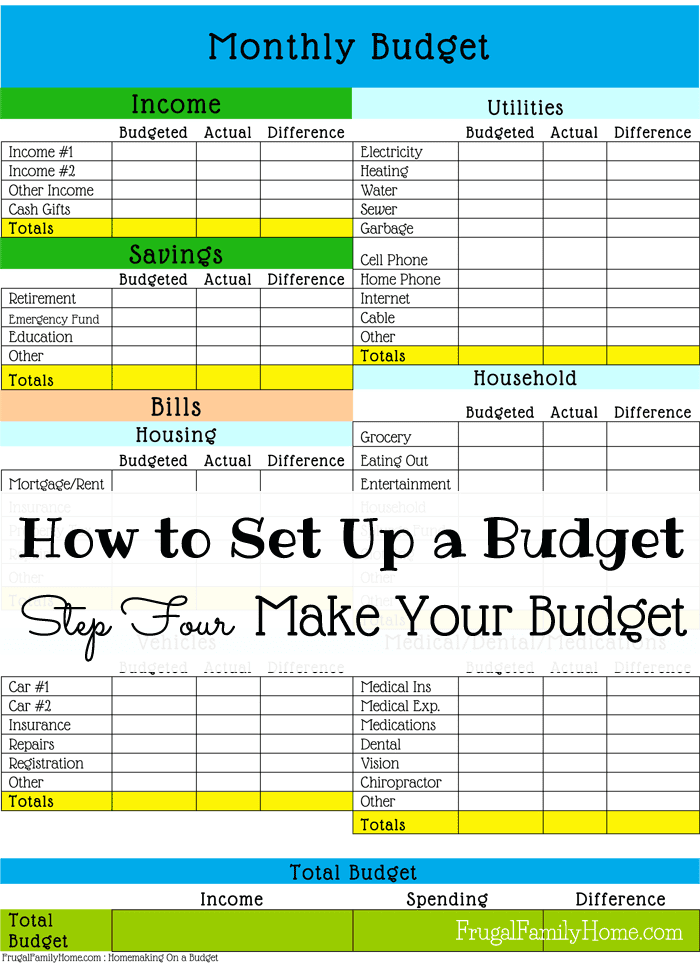

Once your income is established, track every penny spent over the last 30 to 60 days. This historical data is vital because it reveals “phantom expenses”—those small, recurring subscriptions or daily habits that seem insignificant but accumulate into substantial annual outflows. Categorizing these expenses into “Fixed” (rent, insurance) and “Variable” (groceries, entertainment) allows you to see exactly where your liquidity is being trapped.

Identifying Fixed vs. Variable Costs

A successful budget distinguishes between obligations and choices. Fixed costs are the non-negotiables: the roof over your head, the lights in your home, and the minimum payments on your debts. These are generally predictable and stable. Variable costs, however, are where the most significant optimization occurs. These include dining out, hobbies, and even utility bills that fluctuate with usage. By identifying the ratio between these two, you can determine how much “flex” your budget has. If your fixed costs exceed 60% of your take-home pay, your financial structure may be brittle, leaving you vulnerable to economic shocks.

Implementing the 50/30/20 Framework

For those new to personal finance, the 50/30/20 rule offers an excellent structural starting point. Developed by Senator Elizabeth Warren, this method suggests allocating 50% of your income to “Needs” (housing, utilities, basic groceries), 30% to “Wants” (hobbies, vacations, dining), and 20% to “Financial Priorities” (debt repayment, emergency funds, and investments). While these percentages can be adjusted based on local cost of living or aggressive financial goals, they provide a balanced benchmark that ensures you are living for today while preparing for tomorrow.

Selecting a Budgeting Strategy Tailored to Your Lifestyle

No two financial journeys are identical, which means the “best” budgeting method is the one you can actually stick to. Once you have your data, you must choose a methodology that aligns with your personality and financial goals.

The Zero-Based Budgeting Method

Zero-based budgeting is the gold standard for those who want maximum control over their capital. The philosophy is simple: every single dollar you earn is assigned a specific “job” until there are zero dollars left over. If you earn $5,000 a month, you must account for all $5,000. This doesn’t mean you spend it all; it means you intentionally direct it toward expenses, savings, or debt. This method is highly effective because it prevents “money leaks” and forces you to prioritize your spending based on current needs rather than habit.

The Envelope System: Tangible and Digital

For many, the abstract nature of digital transactions leads to overspending. The Envelope System is a classic behavioral finance tool where you allocate cash into physical envelopes for different categories (e.g., $400 for groceries, $100 for entertainment). Once the envelope is empty, spending in that category stops for the month.

In the modern era, many people use “digital envelopes” by opening multiple sub-savings accounts or using specialized apps. This creates a psychological barrier between different “buckets” of money, making it much harder to accidentally spend your rent money on a weekend getaway.

Leveraging Financial Tools and Automation

The greatest enemy of a budget is human friction. If tracking your expenses feels like a chore, you will eventually stop doing it. This is where financial technology becomes an ally. Aggregator tools can sync with your bank accounts to automatically categorize transactions, providing real-time visualizations of your spending.

Furthermore, automation is the “secret sauce” of wealthy individuals. Setting up automatic transfers to your savings and investment accounts on payday ensures that you “pay yourself first.” By removing the decision-making process, you eliminate the temptation to spend money that should be earmarked for your future.

Integrating Debt Management and Wealth Creation

A budget is not merely about maintenance; it is a tool for growth. To truly master your money, your budget must address the twin pillars of debt reduction and asset accumulation.

Debt Repayment Strategies: Snowball vs. Avalanche

High-interest debt is the primary obstacle to wealth. Within your budget, you must decide on a strategy to eliminate it. The “Debt Snowball” method focuses on psychological wins by paying off the smallest balances first, creating momentum. Conversely, the “Debt Avalanche” method focuses on mathematical efficiency, targeting the debts with the highest interest rates first. While the Avalanche saves more money in interest over time, the Snowball is often more effective for those who need the motivational boost of seeing accounts close. Your budget should clearly state which method you are using and exactly how much “extra” capital is being funneled toward these liabilities.

Building and Maintaining an Emergency Fund

A budget without an emergency fund is a house built on sand. Before investing heavily in the stock market or luxury purchases, your budget must prioritize a liquidity cushion. Ideally, this should cover three to six months of essential living expenses. This fund acts as your personal insurance policy against job loss, medical emergencies, or unforeseen repairs. By including a “Savings” line item in your budget specifically for this fund, you transform it from an afterthought into a primary financial objective.

Strategic Investing for Long-Term Growth

Once your high-interest debt is managed and your emergency fund is established, your budget should pivot toward wealth creation. This involves allocating funds to retirement accounts (like 401ks or IRAs) and brokerage accounts. The key here is consistency. Even small, monthly contributions benefit from the power of compounding interest. Your budget should treat your investment contributions as a non-negotiable “bill” that you owe to your future self.

Optimization and Long-Term Sustainability

Creating a budget is an event; maintaining a budget is a lifestyle. The final stage of a professional budgeting plan involves fine-tuning your habits and preparing for the irregularities of life.

Managing Sinking Funds for Irregular Expenses

One of the most common reasons budgets fail is the “surprise” expense—the annual car registration, the holiday season, or a semi-annual insurance premium. Sinking funds are a proactive solution. By calculating the annual cost of these items and dividing by twelve, you can save a small amount each month. This prevents “budget shock” and ensures that these predictable events do not derail your financial progress.

Combating Lifestyle Creep

As your career progresses and your income increases, there is a natural tendency for your expenses to rise in tandem—a phenomenon known as lifestyle creep. A well-structured budget provides a defense against this. Instead of automatically increasing your spending when you get a raise, maintain your current standard of living and direct the surplus toward your financial goals. This widens the gap between what you earn and what you spend, which is the ultimate engine of wealth creation.

The Monthly Financial Review

Finally, a budget is a living document. At the end of every month, conduct a “Financial Post-Mortem.” Compare your actual spending against your planned budget. Did you overspend on dining? Did you forget to account for a subscription? Use these insights to adjust the following month’s plan. This iterative process allows you to refine your categories and goals, ensuring that your budget remains a realistic reflection of your life and your aspirations.

In conclusion, the journey toward financial independence begins with the intentionality of a budget. By understanding your cash flow, choosing a strategy that fits your psychology, and remaining disciplined in your execution, you transform money from a source of stress into a powerful tool for achieving your life’s ambitions. Budgeting is not about deprivation; it is about empowerment. It is the process of telling your money where to go, instead of wondering where it went.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.