In an era dominated by instant wire transfers, mobile payment apps, and cryptocurrency, the humble paper cheque remains a cornerstone of the global financial system. Whether you are setting up a direct deposit for a new job, paying a significant tax bill, or establishing a recurring payment for a mortgage, the data printed on your cheque is the bridge between your liquid assets and the rest of the world. Among these data points, the routing number is arguably the most critical.

Understanding where to find the routing number on a cheque and, more importantly, understanding its function is a fundamental skill in personal and business finance. This guide provides a deep dive into the anatomy of a cheque, the mechanical role of routing numbers in the banking system, and how to manage this sensitive information in a digital-first economy.

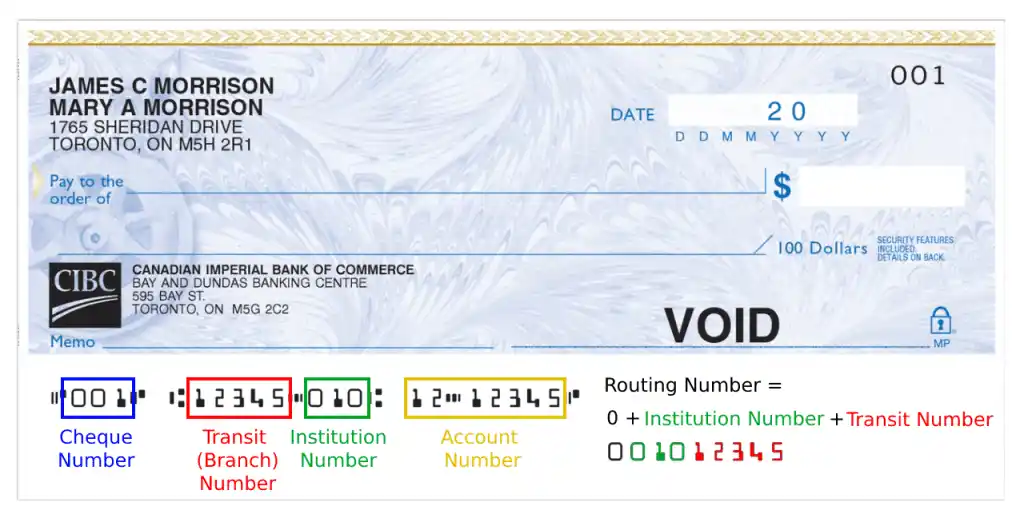

Decoding the Anatomy of a Paper Check

When you look at a cheque, you are looking at a standardized financial instrument designed for machine readability. Since the 1950s, the banking industry has utilized a specific system to ensure that cheques can be processed quickly and accurately by high-speed scanners. This system relies on the line of numbers at the bottom of the document.

The Routing Transit Number (RTN)

On a standard personal or business cheque, the routing number—officially known as the Routing Transit Number (RTN)—is the nine-digit code located at the bottom-left corner. It is always nine digits long and is flanked by a specific symbol known as a “transit character” in the Magnetic Ink Character Recognition (MICR) font.

The routing number acts as an address for your financial institution. Just as a zip code tells the postal service which town to deliver a letter to, the routing number tells the Federal Reserve and other banks exactly where the funds should be sent or requested from.

The Account Number

To the right of the routing number is your unique account number. While the routing number is shared by every customer at your specific branch or bank, the account number is yours alone. It typically ranges from 8 to 12 digits, though this varies by institution. In the sequence at the bottom of the cheque, the account number is usually the middle set of digits, separated from the routing number by a “on-us” symbol.

The Check Number

The third component of the bottom line is the cheque number. This is a short sequence (usually 3 or 4 digits) that corresponds to the number printed in the top-right corner of the cheque. This is used for record-keeping and fraud prevention, allowing you and your bank to track which specific cheques have been cashed.

The MICR Line: Why the Font Matters

You may notice that the numbers at the bottom of a cheque look slightly “blocky” or unusual. This is the MICR line, printed with specialized magnetic ink. This technology allows computers to read the information even if there are stamps, signatures, or cancelation marks over the numbers. In the niche of business finance, understanding the MICR line is essential for ensuring that custom-printed cheques are compliant with banking standards to avoid processing delays or fees.

The Role of Routing Numbers in Personal and Business Finance

The routing number is not merely a label; it is the “DNA” of a transaction. Without this nine-digit code, the infrastructure of the American banking system—specifically the Automated Clearing House (ACH) and the Check 21 system—would cease to function.

Facilitating Automated Clearing House (ACH) Transfers

Most modern financial transactions, such as the electronic transfer of funds from one bank to another, happen via the ACH network. When you provide your routing number to an employer or a utility company, you are giving them the map required to navigate the ACH network. The first two digits of the routing number actually identify the Federal Reserve district where the bank is located, ensuring the electronic “handshake” between institutions happens in the correct jurisdiction.

Setting Up Direct Deposits and Side Hustles

For individuals looking to maximize their online income or manage multiple side hustles, the routing number is the key to getting paid. Whether you are a freelancer receiving payments via a platform or a corporate employee, the accuracy of the routing number is paramount. A single digit error can result in a “returned item” or, worse, the funds being routed to the wrong institution, leading to significant delays in liquidity.

Managing Recurring Bill Payments

From a personal finance perspective, using your routing and account numbers for bill pay (rather than a debit card) can often be more secure and cost-effective. Many service providers charge convenience fees for credit card transactions but waive them for ACH transfers. By locating the routing number on your cheque, you can automate your financial life, ensuring bills are paid on time while maintaining a clearer paper trail for your accounting software.

How to Find Your Routing Number Without a Physical Check

We are increasingly living in a “checkless” society. Many modern “neobanks” and digital-only accounts do not even issue physical chequebooks by default. However, the need for a routing number persists. If you do not have a cheque handy, there are several professional ways to retrieve this information.

Utilizing Online Banking Portals and Mobile Apps

The most efficient way to find your routing number is through your bank’s secure mobile app or website. Usually, under “Account Details” or “Direct Deposit Information,” the bank will list both the routing number and your account number. It is important to note that some large national banks have different routing numbers for different states or different types of transactions (e.g., one for ACH and another for domestic wire transfers).

Checking Monthly Bank Statements

Every formal bank statement—whether delivered via mail or as a PDF—contains your account information. Look at the header of your statement or the summary page. While it may not always display the routing number as prominently as a cheque does, it is legally required to provide enough information for you to identify the financial institution.

Contacting Your Financial Institution Directly

If you are unsure which routing number to use—particularly for high-value business finance transactions like a down payment on a property—the safest route is to call your bank or visit their official website’s FAQ section. Using the “paper” routing number for a “wire” transfer can sometimes result in the transaction being rejected, so verifying the specific use case is a hallmark of savvy financial management.

Security Best Practices: Protecting Your Routing and Account Details

In the world of digital security and personal finance, your routing and account numbers are “static” credentials. Unlike a credit card, which can be easily canceled and replaced with a new number, your bank account details often remain the same for decades. This makes them a high-value target for fraudsters.

The Risks of MICR Information Exposure

If a bad actor obtains your routing and account numbers, they have the two primary components needed to print fraudulent cheques or initiate unauthorized ACH withdrawals. While banks have sophisticated fraud detection algorithms, the onus of “first-line defense” remains with the account holder. Never share a photo of a voided cheque on social media, and be wary of providing this information over unsecured email.

How to Safely Dispose of Old Checks

Many people keep old chequebooks from closed accounts in “junk drawers.” From a financial security standpoint, this is a significant liability. If you close an account or move to a new bank, you should use a cross-cut shredder to destroy all remaining cheques. This ensures that the MICR line—containing your routing and account data—cannot be reconstructed by identity thieves.

Monitoring for Unauthorized Transactions

The best defense in personal finance is active monitoring. Most banking apps now allow you to set up “push notifications” for any ACH transaction or cheque cleared against your account. By staying engaged with your daily transaction logs, you can spot the unauthorized use of your routing number immediately, allowing you to trigger a “stop payment” or freeze the account before significant capital is lost.

The Future of Banking: Will Routing Numbers Become Obsolete?

As we look toward the future of money, the relevance of the routing number system is often questioned. With the rise of FinTech, are we moving toward a world where these nine-digit codes are no longer necessary?

The Rise of Real-Time Payments (RTP) and FedNow

The U.S. Federal Reserve recently launched “FedNow,” a service designed to allow banks to process payments instantly, 24/7. While these systems aim to modernize the speed of transactions, they still largely rely on the existing infrastructure of routing numbers to identify participating institutions. For the foreseeable future, the routing number will remain the primary “ID card” for banks within the American domestic market.

Blockchain and Decentralized Finance (DeFi) Alternatives

In the world of cryptocurrency and DeFi, the “routing number” is replaced by a “wallet address.” These alphanumeric strings serve a similar purpose—directing funds to a specific destination. However, the traditional banking sector and the DeFi sector are currently operating on parallel tracks. Until there is a total convergence of traditional fiat currency and blockchain technology, the routing number on your cheque remains the gold standard for mainstream financial reliability.

Why the ABA Routing System Remains the Gold Standard

The American Bankers Association (ABA) created the routing system over a century ago to bring order to a chaotic financial landscape. Its longevity is a testament to its design. For the business owner, the investor, and the everyday consumer, the routing number represents stability. It is the foundation upon which direct deposits, tax refunds, and multi-million dollar business acquisitions are built.

In conclusion, knowing where the routing number is on a cheque is only the beginning. By understanding its role in the broader financial ecosystem, you gain better control over your personal finance, enhance your digital security, and ensure that your money moves with the precision and speed required in the modern world. Whether you are writing a physical cheque or copy-pasting digits into a payroll portal, those nine numbers are the keys to your financial mobility.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.