In the realm of personal and business finance, numbers are the language of progress. However, raw data rarely tells the full story. To understand the health of an investment, the efficiency of a budget, or the growth of a side hustle, one must master the art of the percentage. Learning how to find the percentage of two numbers is not merely a middle-school math exercise; it is a fundamental skill for financial literacy that allows you to compare disparate values on a level playing field.

Whether you are calculating the interest on a high-yield savings account, determining your debt-to-income ratio, or evaluating the dividend yield of a stock, the percentage is the metric that provides context. In this guide, we will explore the mechanics of percentage calculations and their vital applications in the world of money.

The Mathematical Foundation of Financial Percentages

Before diving into complex financial models, it is essential to master the basic formula. At its core, a percentage is a way of expressing a number as a fraction of 100. In finance, this helps us understand the “weight” of a specific expense or the “rate” of a specific return.

The Basic Formula for Comparing Two Numbers

To find what percentage one number is of another, you use a simple three-step process:

- Divide the “part” (the number you want to analyze) by the “whole” (the total amount).

- Take the resulting decimal.

- Multiply by 100 to convert it into a percentage.

For example, if you saved $500 out of a $4,000 monthly paycheck, you would divide 500 by 4,000 to get 0.125. Multiplying by 100 gives you 12.5%. In financial terms, your savings rate for that month is 12.5%.

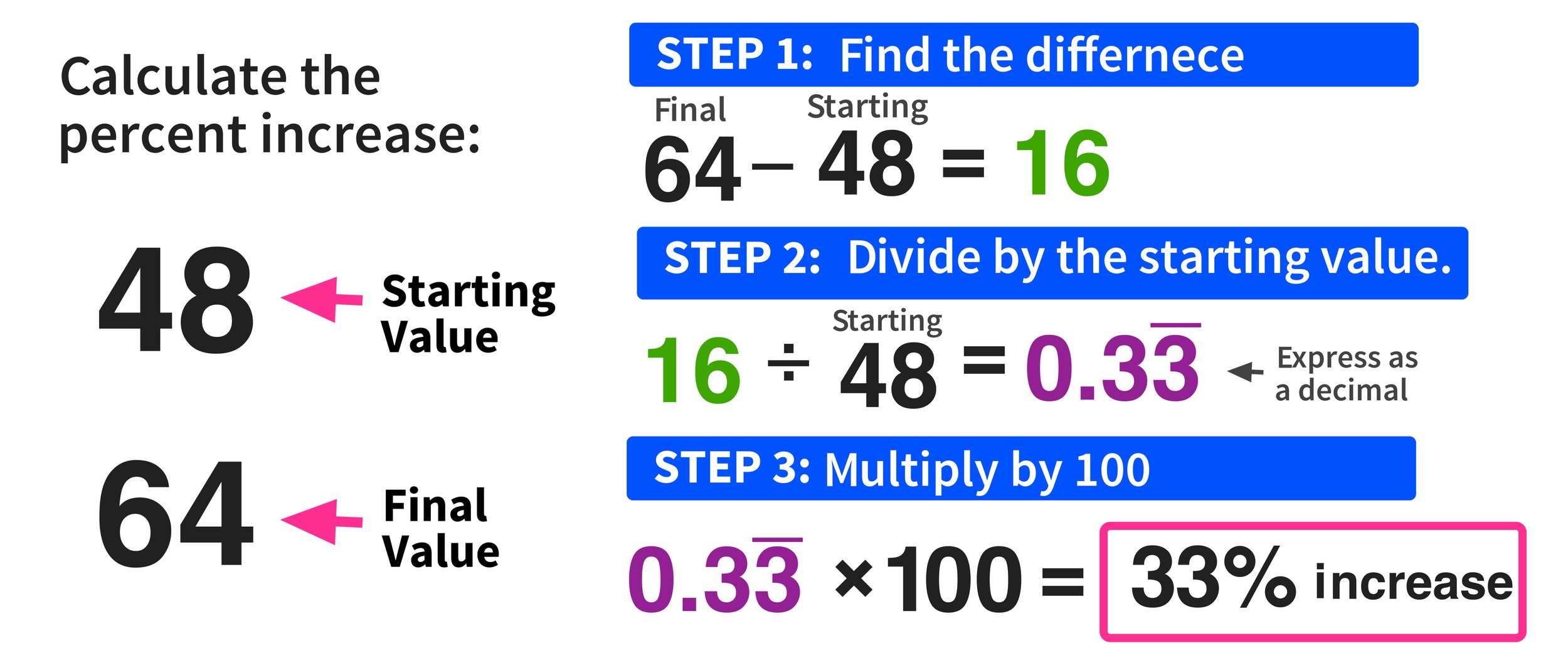

Calculating Percentage Increase and Decrease

In the world of investing and budgeting, we are often more concerned with the change between two numbers over time. This is known as percentage increase or decrease. The formula is:

[(New Value - Old Value) / Old Value] * 100

If your portfolio was worth $10,000 last year and is worth $11,500 today, the calculation would be ($11,500 – $10,000) / $10,000 = 0.15. Multiplying by 100 shows a 15% return on investment. Mastering this allows you to see past the dollar amounts and understand the actual velocity of your wealth creation.

Applying Percentages to Personal Finance and Budgeting

Personal finance is less about how much you make and more about the percentages of how you allocate it. High-income individuals can still find themselves in financial distress if their percentage of discretionary spending is too high, while those with modest incomes can build significant wealth by maintaining a high savings percentage.

The 50/30/20 Rule

One of the most popular budgeting frameworks relies entirely on the percentage of two numbers: your income and your expenses. The 50/30/20 rule suggests that:

- 50% of your after-tax income should go to “Needs” (housing, utilities, groceries).

- 30% should go to “Wants” (dining out, hobbies, travel).

- 20% should be allocated to “Savings and Debt Repayment.”

By calculating these percentages monthly, you can identify “lifestyle creep.” If your “Wants” have climbed to 45% of your income, you know exactly where to prune your spending to regain financial equilibrium.

Understanding Your Debt-to-Income (DTI) Ratio

Lenders, especially mortgage providers, use the percentage of two numbers to determine your creditworthiness. Your Debt-to-Income ratio is calculated by dividing your total monthly debt payments by your gross monthly income.

A DTI of 36% or lower is generally considered healthy. If you earn $6,000 a month and your debts (car loan, student loans, credit cards) total $3,000, your DTI is 50%. This high percentage signals to financial institutions that you are “over-leveraged,” making it difficult to secure new loans or favorable interest rates. Knowing this percentage allows you to target debt aggressively before applying for a mortgage.

Percentage Calculations in Investing and Wealth Building

For the savvy investor, percentages are the ultimate tool for performance evaluation. Raw gains are deceptive; a $1,000 profit on a $10,000 investment is excellent (10%), but a $1,000 profit on a $100,000 investment is lackluster (1%).

Calculating Return on Investment (ROI)

ROI is the gold standard for measuring the efficiency of an investment. By finding the percentage difference between the cost of the investment and its current value, you can compare different asset classes.

For instance, if you invested $2,000 in a cryptocurrency and sold it for $2,600, your ROI is 30%. If you invested $2,000 in a blue-chip stock and it grew to $2,200, your ROI is 10%. By looking at these percentages, you can make informed decisions about risk-adjusted returns and where to allocate your future capital.

Portfolio Allocation and Diversification

Modern Portfolio Theory suggests that risk can be managed by maintaining specific percentages of different asset classes. An investor might decide on a “60/40” split—60% in equities (stocks) and 40% in fixed income (bonds).

As the market fluctuates, these percentages will shift. If stocks perform exceptionally well, they might grow to represent 70% of the portfolio. To “rebalance,” the investor must calculate the percentage of the current total and sell off the excess to return to the original target. This disciplined approach, rooted in percentage calculation, forces you to “buy low and sell high” automatically.

The Power of Dividend Yield

For income-focused investors, the dividend yield is a critical percentage. It is calculated by dividing the annual dividend payment by the current share price. If a company pays $2.00 per year in dividends and the stock costs $50, the yield is 4%. This percentage allows you to compare the income potential of a stock against the interest rate of a savings account or a government bond.

Business Finance: Margin and Profitability Analysis

If you run a business or a side hustle, understanding the percentage relationship between your costs and your revenue is the difference between scaling and going bankrupt. Many entrepreneurs confuse “markup” with “margin,” a mistake that can lead to significant financial losses.

Gross Profit Margin vs. Net Profit Margin

Profitability is always measured in percentages.

- Gross Profit Margin: This is calculated by taking your total revenue minus the Cost of Goods Sold (COGS), then dividing that number by the total revenue. It tells you how much money is left to cover operating expenses after the direct costs of the product are paid.

- Net Profit Margin: This is the “bottom line” percentage. It is your final profit (after all taxes, interest, and operating expenses) divided by total revenue.

A business might have a high gross margin of 70%, but if its net margin is only 2%, it is likely suffering from excessive overhead or inefficient operations.

Markup vs. Margin: The Essential Distinction

This is a common area of confusion in business finance.

- Markup is the percentage added to the cost to get the selling price. (If a product costs $80 and you sell it for $100, the markup is 25% of the cost).

- Margin is the percentage of the selling price that is profit. (Using the same numbers, the $20 profit divided by the $100 selling price is a 20% margin).

Failing to understand the difference can lead to underpricing services. If you want a 25% profit margin, you cannot simply mark up your costs by 25%. You must calculate the percentage correctly to ensure your business remains solvent.

Conclusion: Mastery of Percentages as a Tool for Financial Freedom

In every facet of money management—from the granular details of a household budget to the macro-analysis of an investment portfolio—the ability to find the percentage of two numbers is indispensable. It transforms raw, intimidating data into actionable insights.

By mastering these calculations, you gain the power to evaluate your financial health objectively. You can see exactly where your money is going, how fast it is growing, and whether your business ventures are truly profitable. In the pursuit of financial freedom, the percentage is not just a math concept; it is the compass that ensures you are moving in the right direction. Whether you are calculating a 20% tip at a restaurant or a 7% annual return on a retirement fund, these numbers provide the clarity needed to make the most of every dollar you earn.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.