In the modern financial landscape, few tickers command as much attention as NVDA. As the vanguard of the artificial intelligence revolution, NVIDIA has transitioned from a niche hardware manufacturer for gamers into a systemic pillar of the global equity markets. When NVIDIA’s stock price dips, it isn’t just a concern for individual shareholders; it often triggers a ripple effect across the Nasdaq and the S&P 500. Understanding “why NVIDIA is down” requires a sophisticated look beyond the surface-level news, diving deep into the mechanics of institutional investing, macroeconomic shifts, and the high-stakes world of corporate valuation.

The Gravity of Valuation: When Growth Meets Reality

One of the most common reasons NVIDIA experiences a downward trend is the sheer weight of its own success. In the world of investing, there is a concept known as being “priced for perfection.” When a company’s valuation reaches the stratospheric levels NVIDIA has seen, every piece of data—no matter how positive—is scrutinized for the slightest hint of deceleration.

The Phenomenon of Profit-Taking and Institutional Rebalancing

For many institutional investors and hedge funds, NVIDIA has been the “trade of the decade.” However, portfolio management mandates often require diversification. When NVIDIA’s stock price surges, it can become an oversized portion of a fund’s total assets. To maintain risk management protocols, fund managers are often forced to sell portions of their winners to rebalance their portfolios. This “success-induced selling” can create downward pressure on the stock price even when the company’s fundamentals remain flawless. It is a technical correction rather than a fundamental one, driven by the logistics of the capital markets.

Mean Reversion and the “Priced for Perfection” Trap

NVIDIA’s price-to-earnings (P/E) ratio has historically fluctuated between high-growth premiums and speculative peaks. When the market senses that the “forward guidance”—the company’s prediction of future earnings—cannot possibly maintain its vertical trajectory, investors begin to pull back. A “beat and raise” earnings report (where the company beats expectations and raises future guidance) is often not enough; if the “raise” isn’t substantial enough to satisfy the most optimistic projections, the stock may sell off as the market undergoes a period of mean reversion.

Macroeconomic Headwinds and the Cost of Capital

NVIDIA does not exist in a vacuum. It is a “risk-on” asset, meaning it thrives when investors are confident and capital is cheap. When the broader economic environment shifts, high-growth tech stocks are usually the first to feel the impact.

Interest Rates and the Discounted Cash Flow Model

The Federal Reserve’s monetary policy is a primary driver of NVIDIA’s daily fluctuations. High-growth companies like NVIDIA are valued based on their future cash flows. When interest rates rise, the “discount rate” used to value those future earnings also rises, which mathematically lowers the present value of the stock. Even if NVIDIA’s business is booming, a hawkish stance from the Fed—suggesting that rates will stay “higher for longer”—can cause a sector-wide sell-off in technology, dragging NVIDIA down regardless of its individual performance.

Sector Rotation: The Great Migration of Capital

The stock market often operates in cycles. There are periods where “Growth” stocks (like NVIDIA) outperform, and periods where “Value” stocks (like utilities or consumer staples) are preferred. If economic data suggests a cooling economy or a potential recession, investors may move their money out of high-volatility tech names and into “defensive” sectors. This sector rotation can lead to significant outflows from NVIDIA as big money seeks the safety of dividends and stable earnings over high-growth potential.

Geopolitical Risks and Regulatory Constraints

As a company that sits at the center of the global technology supply chain, NVIDIA is uniquely sensitive to the geopolitical climate. Its products are not just consumer goods; they are strategic assets for national security and economic dominance.

Export Controls and the China Factor

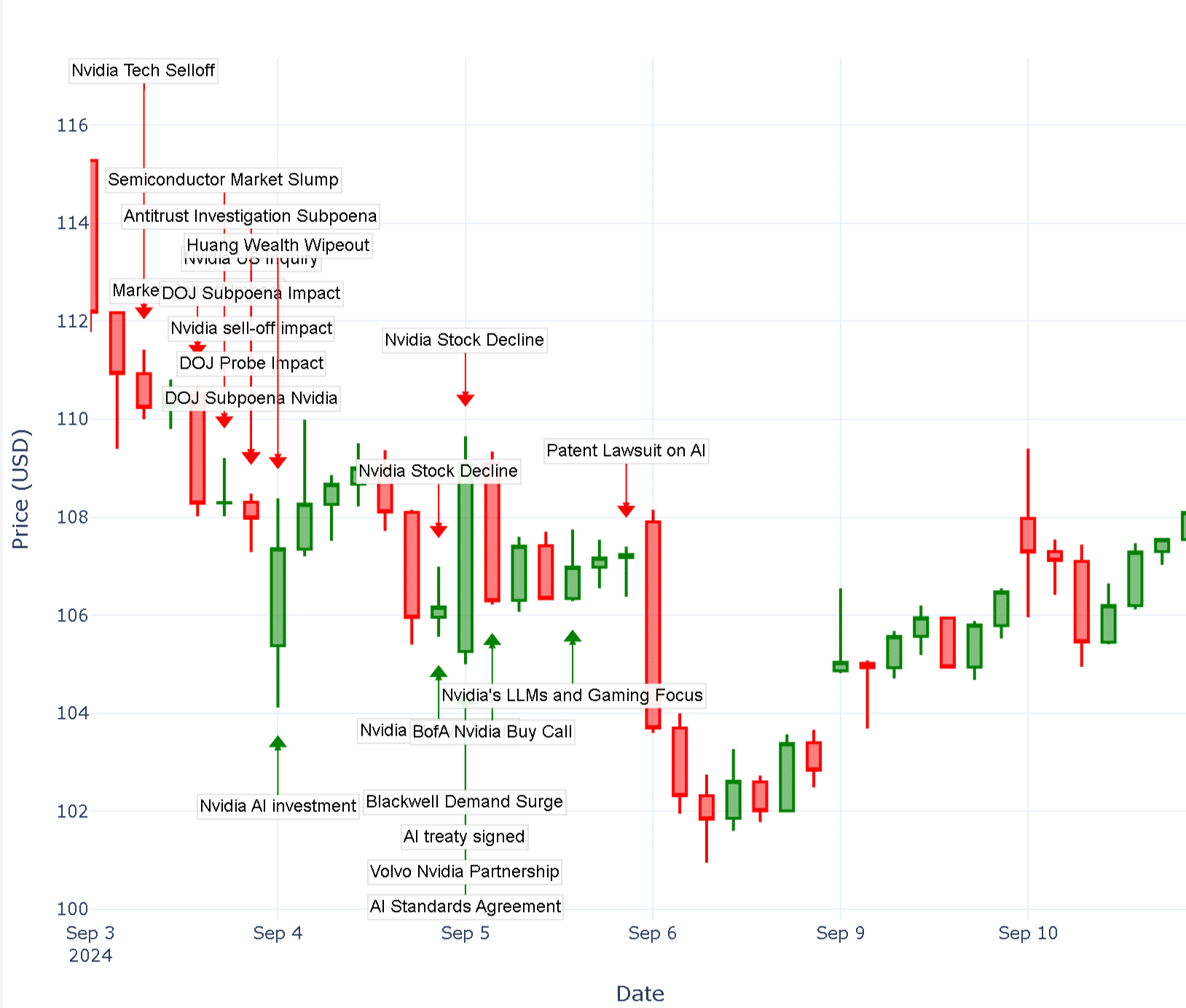

A significant portion of NVIDIA’s historical and projected revenue comes from the Chinese market. When the U.S. Department of Commerce imposes or tightens export controls on high-performance semiconductors, it directly threatens NVIDIA’s total addressable market (TAM). Any news suggesting new restrictions on the sale of AI chips to sovereign competitors often leads to an immediate drop in share price. Investors fear that these lost revenues cannot be easily replaced by other regions, creating a “ceiling” on the company’s growth.

Antitrust Scrutiny and Market Dominance

With dominance comes the eye of the regulator. As NVIDIA captures the lion’s share of the AI chip market, it faces increasing scrutiny from antitrust bodies in the U.S., the EU, and beyond. Rumors or formal announcements of investigations into NVIDIA’s business practices—such as how it bundles software with hardware or its dominance in the data center space—can spook the market. Regulatory hurdles introduce uncertainty, and the market notoriously hates uncertainty. The threat of fines, forced divestitures, or restricted business models can lead to a sustained downward trend as the “regulatory risk premium” is factored into the stock price.

Competitive Pressures and the “Hyperscaler” Shift

While NVIDIA currently holds a near-monopoly on the high-end GPUs required for large language models, the investment community is always looking at the “moat”—the competitive advantage that protects a company from rivals.

The Rise of Custom Silicon (ASICs)

NVIDIA’s largest customers are also its greatest potential threats. Companies like Amazon (AWS), Google (GCP), and Microsoft (Azure) are currently spending billions on NVIDIA chips. However, to reduce their dependence and lower costs, these “hyperscalers” are increasingly developing their own custom AI chips (ASICs). If the market perceives that these internal projects are becoming viable alternatives to NVIDIA’s H100 or Blackwell architectures, the long-term revenue projections for NVIDIA are revised downward.

Traditional Rivals and the Price Wars

While NVIDIA remains the performance leader, competitors like AMD and Intel are constantly nipping at its heels. If a competitor announces a product that offers better “performance per dollar” or if NVIDIA is forced to lower its margins to maintain market share, investors react negatively. In the world of high-finance, margins are everything. A dip in gross margins suggests that the company is losing its pricing power, which is a red flag for those who invested in NVIDIA specifically for its unrivaled market position.

Conclusion: Navigating the Volatility

To the casual observer, a 5% or 10% drop in NVIDIA’s stock price might seem like a sign of trouble. However, for the seasoned investor, these movements are often the natural “breathing” of a high-performance asset. Whether the dip is caused by institutional rebalancing, macroeconomic shifts in interest rates, geopolitical tensions, or the inevitable rise of competition, understanding the underlying “Money” niche factors is essential.

NVIDIA remains a barometer for the broader market’s appetite for risk and its belief in the future of artificial intelligence. While the “why” behind a daily drop can be complex, it usually boils down to a recalibration of value in an ever-changing financial ecosystem. For those focused on long-term wealth creation, these moments of downward volatility are often viewed not as a failure of the company, but as a necessary correction in the long and winding road of a transformative technological era. Understanding these financial levers allows investors to move past the headlines and make informed decisions based on the rigorous logic of the markets.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.