The question “who owns Meta” might seem straightforward at first glance, but the answer delves into the intricate world of corporate finance, stock market dynamics, and the unique governance structures often employed by tech behemoths. Far from being owned by a single entity beyond its founder, Meta Platforms, Inc. – the parent company of Facebook, Instagram, WhatsApp, and Oculus – is a publicly traded company. This means its ownership is distributed among a vast array of shareholders, from individual retail investors to colossal institutional funds. However, the true power behind the throne, the ultimate controlling interest, remains firmly in the hands of its visionary, and often controversial, founder: Mark Zuckerberg. Understanding this complex web of ownership is crucial for anyone interested in the financial power structures that underpin the global economy, the nuances of investing, and the future trajectory of one of the world’s most influential companies.

The Architect of Control: Mark Zuckerberg’s Unwavering Grip

While Meta is a public company, trading under the ticker symbol META on NASDAQ, its ownership structure is designed to grant Mark Zuckerberg disproportionate control. This isn’t an accident but a deliberate mechanism implemented since the company’s early days, solidified during its 2012 IPO. This founder-centric model is common among tech giants, allowing visionaries to pursue long-term strategic goals without the constant pressure of short-term market demands from a diverse shareholder base.

The Genesis of Ownership: From Founder to Billionaire

Mark Zuckerberg’s journey began in a Harvard dorm room, and as Facebook rapidly scaled, so did his ownership stake. Early funding rounds from venture capitalists diluted his percentage ownership but never his absolute control. When Facebook went public, a critical juncture for any founder relinquishing some degree of control, Zuckerberg meticulously structured the company’s share classes to ensure his continued dominance. This foresight has been a defining characteristic of Meta’s governance, enabling Zuckerberg to steer the company through numerous controversies and transformative shifts, including the pivotal rebranding to Meta Platforms in 2021. His initial ownership, combined with strategic share class structures, laid the foundation for an enduring financial and strategic command.

The Power of Dual-Class Shares: A Fortress of Voting Rights

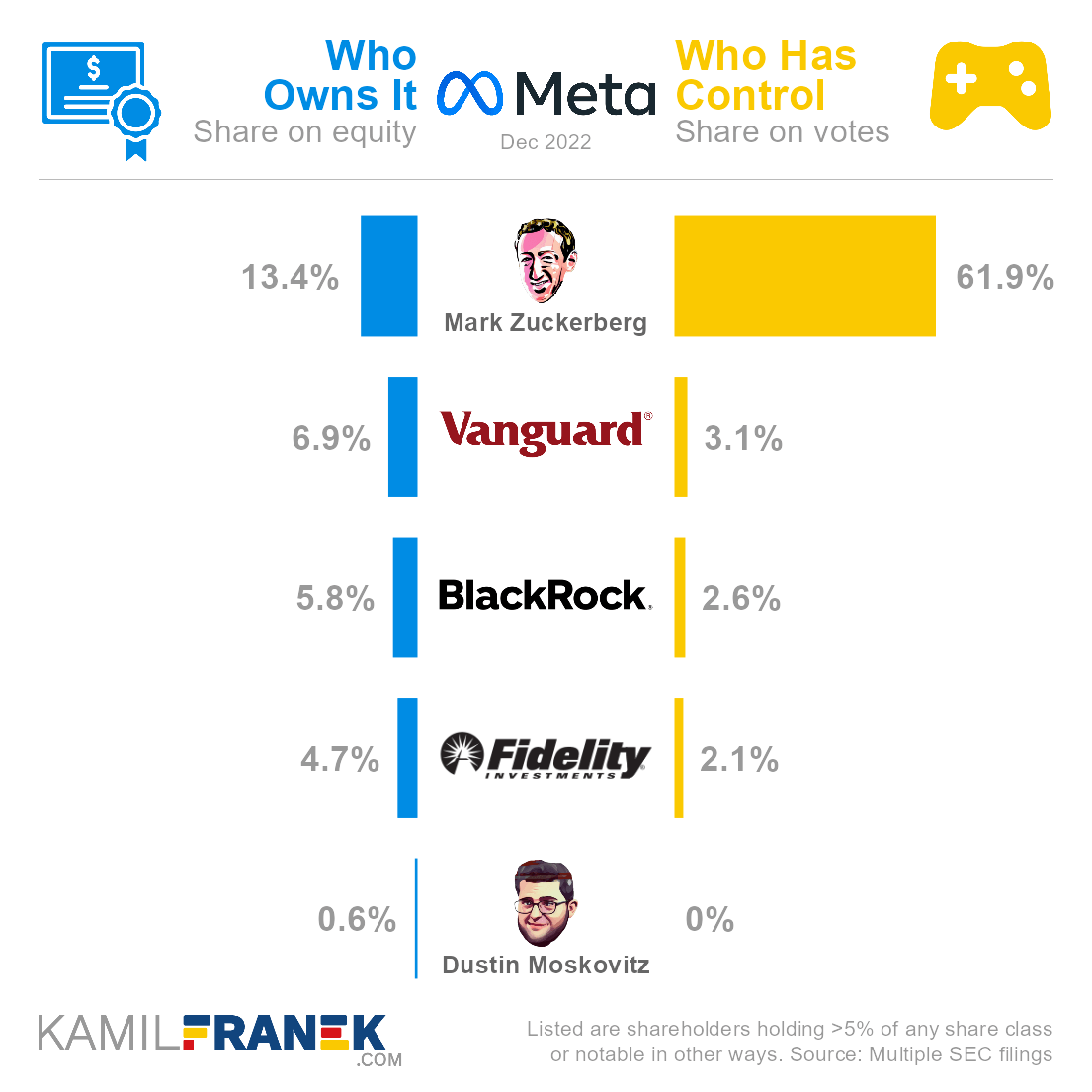

The cornerstone of Zuckerberg’s control is Meta’s dual-class stock structure. The company issues two primary types of common stock: Class A and Class B.

- Class A Shares: These are the shares traded on the NASDAQ. Each Class A share typically grants one vote. These are the shares held by most public investors, including institutional funds and individual retail investors.

- Class B Shares: These shares are not publicly traded and are primarily held by Mark Zuckerberg and a select few early insiders. Crucially, each Class B share carries ten votes. This super-voting power is the lynchpin of Zuckerberg’s control.

Despite owning significantly less than 50% of the total outstanding shares, Zuckerberg’s Class B shares grant him a clear majority of the voting power. This means he effectively controls the outcome of all major shareholder votes, including the election of directors to Meta’s board, significant corporate transactions, and changes to the company’s bylaws. This dual-class structure acts as a formidable defense against hostile takeovers or activist investors seeking to alter the company’s strategic direction against Zuckerberg’s will, solidifying his position as the ultimate decision-maker in the company’s financial and operational destiny.

Financial Implications of Founder-Led Control

Zuckerberg’s concentrated control has profound financial implications. It allows Meta to prioritize long-term, capital-intensive projects, such as the ambitious metaverse initiative, which may not yield immediate returns and could be viewed skeptically by short-term focused investors. This control enables sustained investment in research and development, often at the expense of quarterly profit margins that might otherwise appease a more demanding public shareholder base. While this can provide stability and strategic clarity, it also means that shareholders have limited recourse if they disagree with Zuckerberg’s vision or capital allocation decisions. The financial narrative of Meta is, in many ways, an extension of Zuckerberg’s personal vision for its future, with less direct pressure from external financial stakeholders than many other public companies.

A Distributed Empire: The Landscape of Public Ownership

While Mark Zuckerberg holds the reins of control, the vast majority of Meta’s economic ownership—the right to future profits and the value of the company—rests with its public shareholders. These shareholders collectively represent a diverse and global investor base, each with their own financial motivations and investment horizons. Their collective capital fuels Meta’s operations and expansion, making them crucial, albeit less influential in terms of direct control, stakeholders.

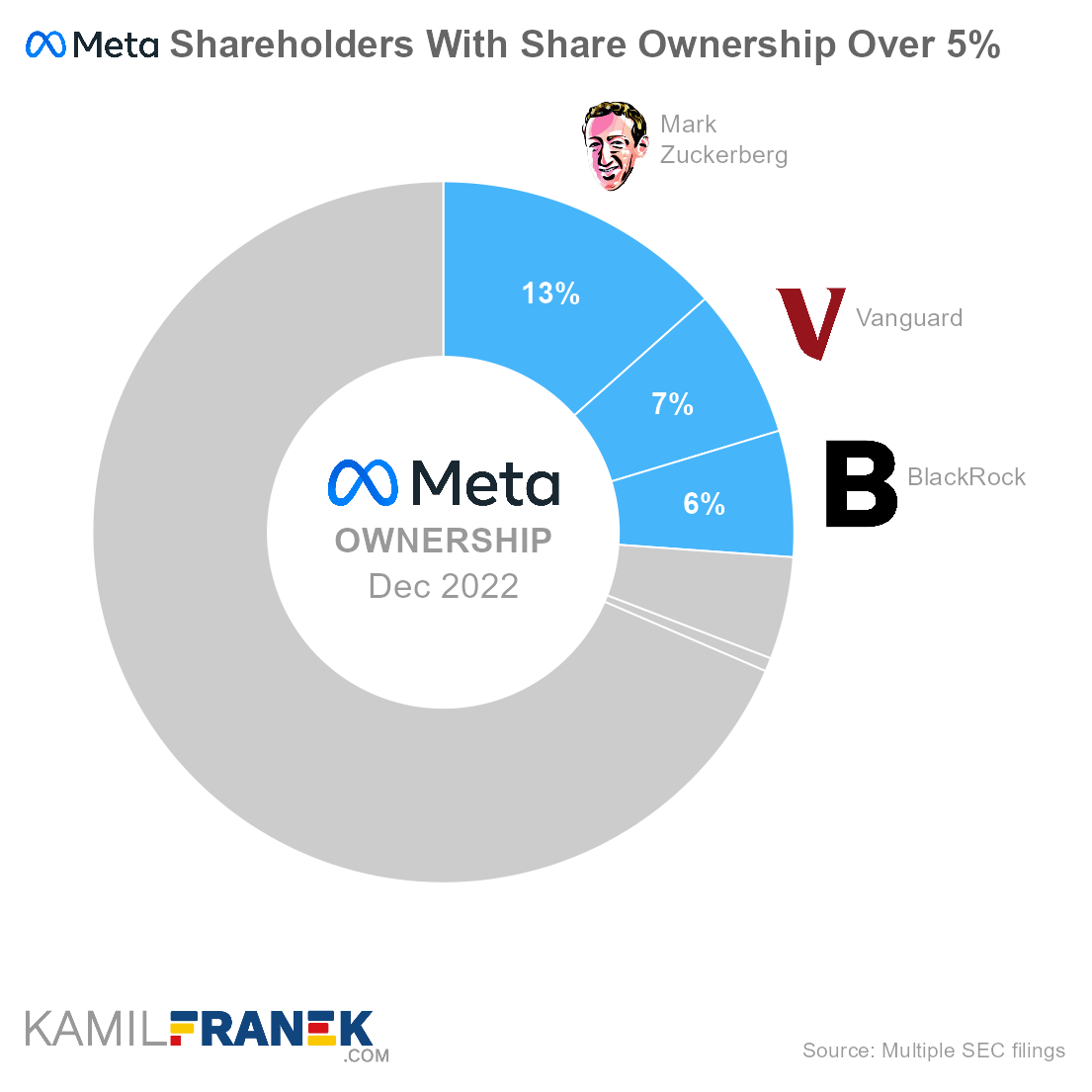

Institutional Investors: The Whale Shareholders

The largest block of Meta’s publicly traded Class A shares is held by institutional investors. These are massive financial entities that manage vast pools of capital on behalf of their clients. They include:

- Mutual Funds: Companies like Vanguard, Fidelity, and BlackRock manage funds that invest in broad market indices or specific sectors, making Meta a common holding in many portfolios.

- Pension Funds: Public and private pension funds invest to secure future retirement benefits for millions, and Meta’s stock often features prominently in their diversified portfolios due to its size and growth potential.

- Hedge Funds: These sophisticated investment vehicles often take larger, more concentrated positions, sometimes aiming to influence corporate strategy, though this is challenging with Meta’s dual-class structure.

- Endowments: University endowments and charitable foundations also invest significant capital in public equities like Meta to support their missions.

These “whale shareholders” often hold billions of dollars worth of Meta stock. While they typically don’t have super-voting rights, their collective ownership of Class A shares means they possess significant economic interest. Their decisions to buy, hold, or sell Meta stock can profoundly impact its market valuation and liquidity, even if they cannot directly outvote Zuckerberg. They engage with Meta management on issues ranging from environmental, social, and governance (ESG) practices to financial performance and capital allocation, leveraging their economic weight to advocate for shareholder value.

Retail Investors: The Collective Voice of Millions

Beyond the institutional giants, millions of individual retail investors own a piece of Meta. These are everyday people who invest through brokerage accounts, retirement funds (like 401(k)s and IRAs), or direct stock purchase plans. Their motivations vary from long-term growth investing to speculative trading. While each individual retail investor’s stake is typically small, their collective ownership forms a substantial portion of the publicly traded float. The ease of access to the stock market through online trading platforms has democratized investment, allowing anyone to become a co-owner of a tech titan like Meta. The cumulative decisions of retail investors, often influenced by market sentiment, news, and social media, can contribute to significant fluctuations in Meta’s stock price, reflecting their belief in the company’s future financial prospects.

Index Funds and ETFs: Passive Ownership, Active Impact

A significant and growing segment of public ownership comes from passive investment vehicles, specifically index funds and Exchange Traded Funds (ETFs). These funds don’t actively pick stocks but rather track a specific market index, such as the S&P 500 or NASDAQ 100. Since Meta is a component of these major indices (and often a very heavily weighted one due to its large market capitalization), any investor buying an S&P 500 index fund is automatically buying a proportionate slice of Meta.

This “passive ownership” is incredibly impactful. Index funds and ETFs represent trillions of dollars in assets, ensuring a constant, stable demand for Meta’s shares as long as it remains a constituent of key indices. While managers of these funds typically don’t engage in activist investing, their sheer size means they are often among the largest shareholders and their proxy voting decisions, guided by institutional guidelines, carry weight in corporate governance issues that are not subject to Zuckerberg’s super-vote. They represent a fundamental layer of Meta’s ownership base, reflecting the company’s entrenched position in the broader market.

Beyond Common Stock: Other Forms of Equity and Compensation

While common stock (Class A and Class B) represents the primary forms of ownership, Meta’s capital structure also includes other financial instruments that convey ownership or future ownership rights, particularly to its employees. These mechanisms are crucial for talent acquisition, retention, and aligning employee incentives with the company’s financial success.

Employee Stock Options and Restricted Stock Units (RSUs)

A significant portion of Meta’s employees receive compensation not just in salary and bonuses, but also in equity, primarily through Restricted Stock Units (RSUs).

- Restricted Stock Units (RSUs): RSUs are grants of company shares that vest over a period (e.g., four years). Once vested, the employee receives the actual shares, which can then be sold or held. This aligns employee interests with shareholder interests, as the value of their compensation directly ties to Meta’s stock performance. This means thousands of Meta employees become de facto shareholders, holding a vested interest in the company’s financial health and growth.

- Stock Options: While less common now for broad-based compensation at mature tech companies compared to RSUs, stock options grant employees the right to buy company shares at a pre-determined price (the “strike price”) at a future date. If the stock price rises above the strike price, the options become valuable, offering a financial incentive for employees to contribute to increasing shareholder value.

These equity compensation plans mean that a broad base of Meta’s workforce holds a financial stake in the company. Their collective ownership, while individually smaller than institutional holdings, represents a significant pool of shares that can influence market dynamics through selling or holding decisions once vested. It fosters a culture where employees are directly rewarded for the company’s financial performance and growth.

Convertible Debt and Preferred Shares (As Potential Financial Instruments)

While Meta primarily relies on common equity and retained earnings for funding, it’s worth noting that other financial instruments can also grant ownership or future ownership rights, though they may not be prominent in Meta’s current capital structure.

- Convertible Debt: This is a type of bond that can be converted into a pre-determined number of common shares at certain times or under certain conditions. Companies might issue convertible debt to raise capital at lower interest rates, offering investors the upside potential of equity conversion if the stock performs well.

- Preferred Shares: These are typically non-voting shares that pay a fixed dividend and have priority over common shares in receiving payments in case of liquidation. They represent a hybrid form of equity and debt.

For a cash-rich, well-established company like Meta, these instruments might be used for specific strategic financing needs rather than broad capital raising. However, understanding their existence is part of a comprehensive view of corporate ownership possibilities, highlighting how financial engineering can create diverse forms of stakeholding beyond simple common stock.

Ownership’s Echo: Impact on Corporate Governance and Financial Strategy

The unique ownership structure of Meta, particularly Mark Zuckerberg’s super-voting control, has profound implications for its corporate governance and overall financial strategy. It shapes how decisions are made, how capital is deployed, and how the company interacts with its broader investor base.

Board Composition and Decision-Making

Zuckerberg’s control over voting shares gives him undeniable influence over the composition of Meta’s Board of Directors. He can effectively appoint directors who align with his long-term vision and strategic priorities. This allows for a streamlined decision-making process, often with fewer dissenting voices than in companies where independent directors have more power or where shareholder activism can more easily sway board elections. While this can lead to agility and bold strategic bets, it also raises concerns about accountability and potential conflicts of interest, as the founder’s personal vision can sometimes overshadow the collective interests of minority shareholders seeking short-term financial returns. The balance between founder vision and independent oversight is a perpetual tension in such governance models.

Capital Allocation: Buybacks, Dividends, and R&D Investment

How Meta allocates its enormous capital resources is directly influenced by its ownership structure. With Zuckerberg’s long-term focus, the company often prioritizes massive investments in future technologies, such as the metaverse, even if these projects demand significant capital expenditures and may not generate profits for years.

- R&D Investment: Meta consistently pours billions into research and development, a strategy supported by Zuckerberg’s control, enabling it to push technological boundaries.

- Share Buybacks: Meta frequently engages in significant share buyback programs, returning capital to shareholders by reducing the number of outstanding shares. This increases earnings per share and can boost stock value. These decisions are made by the board, effectively controlled by Zuckerberg.

- Dividends: Unlike many mature, profitable companies, Meta has historically not paid regular cash dividends. This is a strategic financial decision, as it allows the company to retain more earnings for reinvestment in growth initiatives, a preference likely championed by its controlling shareholder who favors reinvestment over immediate payouts.

These capital allocation choices reflect a specific financial philosophy that values long-term growth and strategic innovation over short-term payouts, a philosophy that a founder with super-voting power can enforce.

Shareholder Activism and Engagement

While Meta’s dual-class structure largely insulates it from hostile takeovers or direct challenges to Zuckerberg’s control, it doesn’t entirely eliminate shareholder activism. Institutional investors, especially those focused on ESG (Environmental, Social, and Governance) issues, often engage with Meta’s management through shareholder proposals and direct dialogue. These proposals, while unlikely to pass if opposed by Zuckerberg, serve as a platform for expressing investor concerns on topics such as data privacy, content moderation, executive compensation, and climate change. Such engagement, even without direct voting power, can exert pressure on Meta to address public concerns and adjust certain aspects of its operations or reporting, impacting its brand reputation and long-term financial stability. These engagements highlight the complex interplay between economic ownership and ethical responsibility in the modern corporate landscape.

The Enduring Question: The Future of Meta’s Ownership Structure

The current ownership structure of Meta has been a defining characteristic of its journey, enabling its founder to pursue ambitious visions. However, no corporate structure is immutable. The future holds potential shifts driven by market dynamics, strategic decisions, and the eventual question of succession.

Succession Planning and Long-Term Vision

A critical, albeit distant, question for Meta’s ownership structure revolves around succession planning for Mark Zuckerberg. What happens when the founder-CEO eventually decides to step down or passes on? The dual-class share structure makes his Class B shares convertible into Class A shares upon sale or transfer under certain conditions. This means that while his direct heirs might inherit the economic value, the super-voting power might not automatically transfer in the same concentrated form. Any future leadership transition could trigger a re-evaluation of the share structure, potentially diluting the concentrated voting power and ushering in a more traditional corporate governance model where public shareholders have a greater say. Such a shift would dramatically alter the company’s financial trajectory and investor relations, potentially bringing it more in line with other large-cap companies.

Market Dynamics and Investor Confidence

The market’s perception of Meta’s ownership structure continuously influences its stock price and investor confidence. While some investors appreciate the stability and long-term vision afforded by Zuckerberg’s control, others might view it as a governance risk, limiting their ability to influence the company. Major strategic shifts, such as the costly pivot to the metaverse, are closely watched by investors for their financial implications. Any significant loss of investor confidence due to perceived missteps or a lack of accountability could lead to sustained downward pressure on the stock, regardless of the underlying ownership structure. Conversely, if Zuckerberg’s vision proves financially successful, his control will be seen as an asset, further solidifying investor trust.

Potential Shifts: Divestitures, Acquisitions, and Capital Raises

While unlikely given Meta’s robust financial position, future strategic moves could theoretically alter its ownership landscape.

- Major Acquisitions: A large, dilutive acquisition funded by issuing new Class A shares could slightly dilute the overall voting power, though Zuckerberg’s Class B shares would maintain control.

- Divestitures: Selling off major assets could impact the company’s valuation and strategic direction, indirectly affecting how investors perceive the value of their ownership.

- New Capital Raises: While Meta has vast reserves, a highly improbable scenario of raising substantial new capital through new share issuances could slightly change the overall distribution of economic ownership.

In conclusion, “who owns Meta” is a question with a multi-faceted answer. While Mark Zuckerberg holds undeniable control through a meticulously designed dual-class share structure, the economic ownership is broadly distributed among millions of institutional and retail investors globally. This unique blend of concentrated control and public economic interest defines Meta’s corporate identity, its financial strategy, and its long-term trajectory as a technological and financial powerhouse. For investors and market observers, understanding this complex interplay is key to navigating the future of one of the world’s most influential companies.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.