The United Services Automobile Association, universally known as USAA, stands as a titan in the American financial landscape. Unlike traditional retail banks that cater to the general public, USAA operates on a foundation of exclusivity, service, and specialized financial care. For those within the military community, the name is synonymous with competitive insurance rates, robust banking features, and a deep understanding of the unique financial stressors that come with a life of service. However, the question of “who is eligible for USAA” remains one of the most frequent inquiries in the world of personal finance. Understanding these eligibility requirements is the first step toward unlocking a suite of financial tools designed specifically for those who wear, or have worn, the uniform.

The Core Mission: Aligning Financial Stability with Military Service

USAA was founded in 1922 by a group of 25 Army officers who decided to insure each other’s vehicles when no one else would. This origin story is vital to understanding their current eligibility rules. Their mission is not just to provide banking services, but to facilitate the financial security of the military community. In the realm of personal finance, niche banking allows for specialized products that general institutions cannot always offer, such as low-interest loans tailored for deployment or insurance policies that cover military gear.

A Legacy of Exclusive Membership

The exclusivity of USAA is a strategic choice. By focusing on a specific demographic—the military and their families—USAA can manage risk more effectively. Historically, military members are seen as a disciplined and reliable cohort, which allows the organization to pass savings back to its members in the form of lower premiums and higher interest rates on savings. This “mutual” structure means that, in many ways, the members are the stakeholders.

Why Personal Finance Experts Recommend Checking Eligibility

Financial advisors often point to USAA as a benchmark for excellence in customer service and product value. From their highly-rated homeowners’ insurance to their diverse range of credit cards with military-specific rewards, the benefits are substantial. For any individual looking to optimize their personal balance sheet, determining if they qualify for USAA membership is often a high-priority task.

The Specific Categories of Eligibility

Eligibility for USAA is primarily tiered around direct service and family legacy. While the rules have evolved over the decades, the core focus remains the “Military Family.” Understanding which category you fall into is essential for a smooth application process.

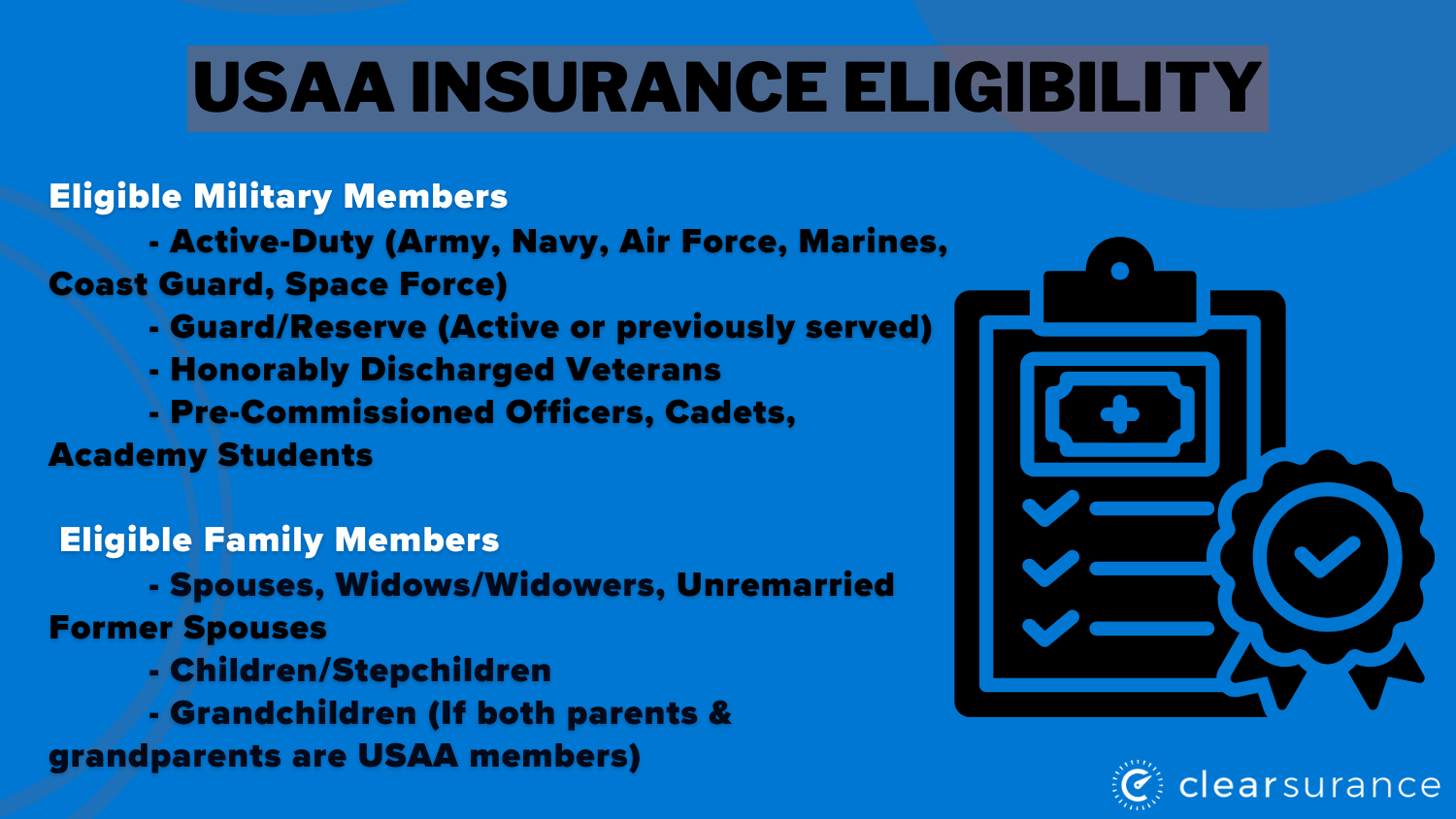

Active Duty, Guard, and Reserve Members

The most straightforward path to membership is through current service. This includes all individuals currently serving in the U.S. Air Force, Army, Coast Guard, Marine Corps, Navy, and Space Force. Whether you are a full-time active-duty soldier or a member of the National Guard or Reserves, you are eligible to join. This eligibility extends the moment you begin your service, allowing young recruits to establish a financial foundation early in their careers.

Veterans and Retired Personnel

Those who have served honorably and have since transitioned to civilian life retain their eligibility. This includes retirees who completed a full military career and veterans who served a single term and received an honorable discharge. For many veterans, USAA provides a sense of continuity, offering financial products that respect their history of service even decades after they have hung up the uniform.

Cadets and Midshipmen

USAA recognizes the leaders of tomorrow by offering membership to those currently enrolled in U.S. service academies, as well as students in ROTC programs on scholarship or within their final two years of the program. By capturing this demographic early, USAA helps future officers manage their stipends, save for their first vehicles, and prepare for the financial realities of their first duty station.

Family Members and Spouses

One of the most powerful aspects of USAA eligibility is its “inheritance” factor. Spouses, widows, and widowers of USAA members are eligible to join. More importantly, children of USAA members can also join, effectively “inheriting” the eligibility from their parents. This creates a multi-generational financial legacy. It is important to note that the parent must have established a USAA account for the children to be eligible. Once a child becomes a member, they can then pass that eligibility down to their own children.

The Financial Ecosystem of USAA: Beyond Just Banking

Once eligibility is confirmed, the member gains access to a comprehensive ecosystem of financial tools. In the world of personal finance, having your insurance, banking, and investments under one roof can lead to better “financial synergy,” where data is shared across platforms to provide a holistic view of your net worth.

Specialized Insurance Products

USAA is perhaps most famous for its insurance. For members, this means auto, home, and life insurance policies that account for military life. For example, their auto insurance often includes discounts for vehicles stored during deployment. Their renters’ insurance is also highly regarded because it typically covers military equipment—such as uniforms and gear—which many standard civilian policies exclude or require expensive riders for.

Banking and Credit Solutions

The banking arm of USAA offers features that cater to a mobile lifestyle. This includes a massive network of fee-free ATMs and early direct deposit, which allows members to receive their military pay up to two days early. In terms of credit, USAA offers cards that provide rewards on base purchases (like at the Commissary or BX/PX) and low APRs that are particularly beneficial during the transition periods of a Permanent Change of Station (PCS).

Investment and Retirement Planning

For members looking toward long-term wealth building, USAA provides access to brokerage services, IRAs, and managed portfolios. While they have partnered with other firms (like Victory Capital and Charles Schwab) for certain investment products in recent years, the integration remains seamless for the member. They provide educational resources specifically aimed at military retirement, helping members navigate the complexities of the Thrift Savings Plan (TSP) and the Blended Retirement System (BRS).

Maximizing the Value of Your Membership

Being eligible is only half the battle; the real advantage comes from strategically using the tools available. In personal finance, “optimization” is the key to building wealth, and USAA offers several avenues to do just that.

Leveraging the Subscriber’s Savings Account

Unique to USAA is the Subscriber’s Savings Account (SSA). Because USAA is a reciprocal inter-insurance exchange, a portion of the organization’s capital is held in accounts designated for its members. In years where the association performs well financially, members may receive distributions or “dividends” from these accounts. This is essentially “found money” that can be reinvested or used to pay down debt, a feature rarely found in traditional corporate banking.

Financial Tools for Deployment and PCS

Moving and deploying are two of the most financially taxing events a military family can face. USAA offers specific toolkits and advice for these transitions. This includes “deployment task lists” that cover everything from setting up powers of attorney to adjusting insurance coverages. By utilizing these resources, members can avoid the common financial pitfalls—like overspending during a move or neglecting bills during a deployment—that often plague service members.

Educational Resources and Financial Advice

USAA invests heavily in the financial literacy of its members. Their platform is filled with calculators, articles, and webinars on topics ranging from “Buying Your First Home with a VA Loan” to “Understanding Military Survivor Benefits.” For a member, these resources act as a free financial advisory service, helping them make informed decisions about big-ticket items and long-term goals.

Navigating the Application: Myths and Realities

There are several misconceptions surrounding USAA eligibility that often prevent qualified individuals from applying. Clearing these up is essential for anyone on the fence about their status.

Myth: “Only Officers Can Join”

This is a relic of the past. While USAA started as an organization for officers, it has been open to all ranks—enlisted and NCOs alike—for many years. Every branch and every rank is welcomed with the same level of service and the same access to products.

Myth: “I Can Join Because My Grandfather Was in the Military”

This is a common point of confusion. Eligibility is passed from parent to child. If your grandfather was a USAA member, he would have had to pass that eligibility to your parent. If your parent is a USAA member, they can then pass it to you. You cannot “skip” a generation if the middle generation never established a membership. However, if your parent is still alive and eligible but not yet a member, they can join today, which immediately makes you eligible.

Required Documentation for Verification

To confirm eligibility, USAA typically requires basic information such as your Social Security number, details of your (or your family member’s) military service, and sometimes a Discharge Document (DD214) or an Enlisted Records Brief (ERB). The process is mostly automated and can often be completed online in a matter of minutes.

Conclusion: The Strategic Advantage of USAA

In the competitive world of personal finance, USAA remains a gold standard for a reason. For those who are eligible, it offers more than just a place to park cash or buy a policy; it offers a specialized financial partnership. By focusing on the unique needs of the military community—from the tactical requirements of deployment to the long-term goals of retirement—USAA helps its members build a more resilient financial future.

Whether you are a new recruit just starting your journey or the child of a veteran looking to carry on a legacy, checking your eligibility for USAA is one of the smartest financial moves you can make. It provides access to a suite of products that prioritize your service, your family, and your long-term financial health. In an era of impersonal “big bank” service, the community-focused approach of USAA continues to be a powerful tool for those dedicated to the defense of the nation.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.