The S&P 500 index stands as a cornerstone of American financial markets, representing 500 of the largest publicly traded companies in the United States by market capitalization. For countless investors, both novice and seasoned, gaining exposure to this benchmark is a fundamental component of a diversified portfolio. It offers a convenient, low-cost way to invest in the broad performance of the U.S. economy, bypassing the complexities and higher risks associated with picking individual stocks.

However, the question “Which S&P 500 to buy?” is more nuanced than it initially appears. While the underlying index remains constant, the investment vehicles that track it — primarily Exchange-Traded Funds (ETFs) and index mutual funds — come with their own characteristics, fees, and operational nuances. Understanding these distinctions is crucial for making an informed decision that aligns with your financial goals, investment horizon, and personal preferences. This guide will demystify the options, helping you select the S&P 500 investment that’s right for you.

Understanding the S&P 500 Index: A Foundation for Investment

Before diving into specific products, it’s essential to grasp what the S&P 500 truly represents and why it holds such prominence in the investment world.

What is the S&P 500?

The S&P 500, or Standard & Poor’s 500, is a market-capitalization-weighted index of 500 of the largest U.S. publicly traded companies selected by S&P Dow Jones Indices. Unlike the Dow Jones Industrial Average, which tracks only 30 large companies, the S&P 500 offers a much broader snapshot of the U.S. stock market. Companies are chosen based on criteria such as market size, liquidity, and sector representation, ensuring the index is diversified across industries like technology, healthcare, financials, consumer discretionary, and more.

Being market-cap-weighted means that companies with larger market values, such as Apple, Microsoft, Amazon, and Google (Alphabet), have a greater impact on the index’s performance. The index’s value reflects the collective performance of these 500 economic powerhouses, making it a reliable indicator of the overall health and direction of the U.S. stock market.

Why Invest in the S&P 500?

Investing in the S&P 500 offers several compelling advantages that make it a favorite among long-term investors:

- Diversification: With 500 companies spanning numerous sectors, an S&P 500 investment inherently provides broad diversification. This significantly reduces the risk associated with investing in individual stocks; if one company performs poorly, its impact on your overall portfolio is mitigated by the performance of the other 499.

- Long-Term Growth Potential: Historically, the S&P 500 has demonstrated robust long-term growth. While past performance is no guarantee of future results, the index has averaged an annual return of around 10-12% over many decades, making it a powerful vehicle for wealth accumulation through compounding.

- Simplicity and Low Cost: Investing in an S&P 500 fund is a form of passive investing. You don’t need to research individual stocks or time the market. Fund managers simply track the index, leading to lower management fees (expense ratios) compared to actively managed funds.

- Accessibility: S&P 500 ETFs and mutual funds are readily available through most brokerage accounts, retirement plans (like 401(k)s and IRAs), and robo-advisors.

The Primary Avenues for S&P 500 Exposure

Once you’ve committed to investing in the S&P 500, the next step is choosing the right investment vehicle. The two most common and effective ways to gain this exposure are through Exchange-Traded Funds (ETFs) and S&P 500 Index Mutual Funds. Both aim to replicate the index’s performance but differ in their structure, trading mechanisms, and suitability for various investor profiles.

S&P 500 Exchange-Traded Funds (ETFs): Flexibility and Liquidity

ETFs are investment funds that hold a collection of underlying assets, in this case, the stocks that comprise the S&P 500 index. They trade on stock exchanges throughout the day, much like individual stocks, offering investors significant flexibility.

Key Characteristics of S&P 500 ETFs:

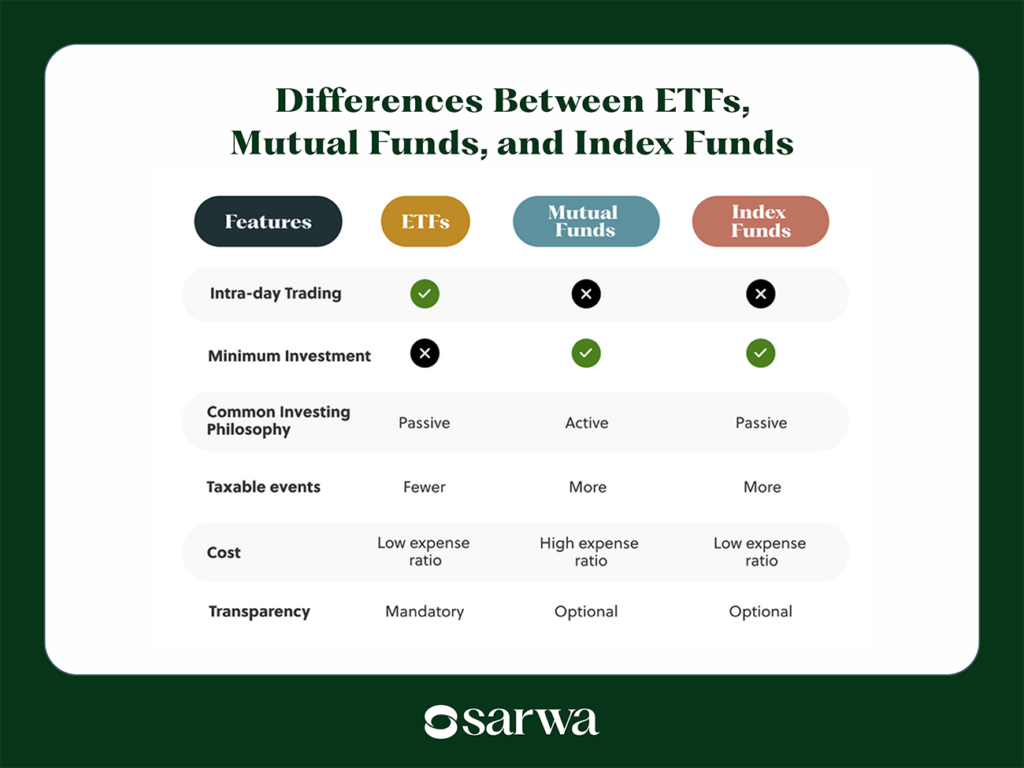

- Intraday Trading: You can buy and sell S&P 500 ETFs at any point during market hours, just like a stock. This allows for precise entry and exit points.

- Low Expense Ratios: Competition among ETF providers has driven expense ratios (annual fees) for S&P 500 ETFs to remarkably low levels, often below 0.10%.

- Tax Efficiency: ETFs are generally considered more tax-efficient than traditional mutual funds, particularly in taxable brokerage accounts. Their unique “in-kind” creation and redemption mechanism helps minimize capital gains distributions to shareholders.

- Popular Options: Some of the most widely recognized S&P 500 ETFs include:

- SPDR S&P 500 ETF Trust (SPY): The oldest and largest S&P 500 ETF, known for its high liquidity and tight bid-ask spreads. Its expense ratio is 0.09%.

- iShares Core S&P 500 ETF (IVV): Offered by BlackRock, IVV also boasts immense popularity and liquidity, with an expense ratio of 0.03%.

- Vanguard S&P 500 ETF (VOO): Vanguard’s offering, known for its extremely low expense ratio of 0.03%, reflecting Vanguard’s commitment to low-cost investing.

Choosing among SPY, IVV, and VOO often comes down to minor differences in expense ratios, trading volume (though all are highly liquid), and personal preference for the fund provider. For most long-term investors, the lower expense ratios of IVV and VOO make them slightly more attractive over the long run.

S&P 500 Index Mutual Funds: Simplicity for Long-Term Investors

S&P 500 index mutual funds also aim to track the performance of the S&P 500, but they operate differently than ETFs.

Key Characteristics of S&P 500 Index Mutual Funds:

- End-of-Day Trading: Unlike ETFs, mutual funds are priced only once per day, after the market closes. All buy and sell orders are executed at this Net Asset Value (NAV). This makes them less suitable for day trading but perfectly fine for long-term investors.

- Automatic Reinvestment: Many mutual funds offer automatic dividend reinvestment, allowing your earnings to seamlessly buy more shares, accelerating compounding.

- Suitability for Dollar-Cost Averaging: Their once-a-day pricing makes them ideal for automated, regular investments, which is a core principle of dollar-cost averaging.

- Provider-Specific Options: Major mutual fund providers offer their own S&P 500 index funds:

- Vanguard 500 Index Fund (VFIAX – Admiral Shares, VOO for ETF shares): Vanguard is a pioneer in index investing, and its S&P 500 fund is a staple. VFIAX (Admiral Shares) has an expense ratio of 0.04%.

- Fidelity 500 Index Fund (FXAIX): Fidelity’s comparable offering, also with a very competitive expense ratio of 0.015%.

- Schwab S&P 500 Index Fund (SWPPX): Schwab provides a similar low-cost option with an expense ratio of 0.02%.

For investors who prefer to set up recurring investments and not worry about intraday price fluctuations, index mutual funds can be slightly simpler to manage, especially if you hold other investments with the same provider. Many brokerage firms also offer “no-transaction-fee” mutual funds, further reducing costs.

Key Factors to Consider When Choosing an S&P 500 Fund

While the goal of all S&P 500 funds is the same—to mirror the index—the execution and costs can vary. Paying attention to these factors can significantly impact your long-term returns.

Expense Ratios: Minimizing Your Costs

The expense ratio is the annual fee you pay for the fund’s management, expressed as a percentage of your total investment. Even seemingly small differences can accumulate into substantial amounts over decades. For instance, an extra 0.10% in fees might seem negligible, but over 30 years on a $100,000 investment with a 7% average annual return, it could cost you tens of thousands of dollars.

When choosing an S&P 500 fund, always aim for the lowest expense ratio possible, ideally below 0.05%. The fierce competition among providers means there’s no reason to pay more.

Tracking Error and Fund Performance: How Closely Does It Match the Index?

Tracking error measures how closely a fund’s performance matches that of its underlying index. While all S&P 500 funds aim for perfect replication, minor deviations can occur due to factors like transaction costs, cash drag, and dividend reinvestment timing.

Reputable S&P 500 funds from major providers generally have minimal tracking error. You can usually find a fund’s tracking error information in its prospectus or on the provider’s website. Prioritize funds with a consistently low tracking error, indicating efficient management and accurate index replication.

Fund Provider and Assets Under Management (AUM): Stability and Scale

While less critical for established S&P 500 funds, considering the fund provider and its Assets Under Management (AUM) can offer additional reassurance.

- Reputable Providers: Large, well-established firms like Vanguard, BlackRock (iShares), Fidelity, and Schwab have a proven track record, robust infrastructure, and significant resources dedicated to managing their funds.

- High AUM: Funds with substantial AUM often benefit from economies of scale, which can contribute to lower expense ratios and better liquidity. A higher AUM also signals investor confidence and the fund’s stability.

Tax Efficiency: ETFs vs. Mutual Funds

In taxable brokerage accounts, tax efficiency can be an important consideration. ETFs generally hold an advantage here due to their unique structure that allows them to minimize capital gains distributions to shareholders. When investors sell ETF shares, they typically do so on the open market, not directly to the fund, which avoids forcing the fund to sell underlying securities. Mutual funds, particularly older ones, may have to sell securities to meet redemptions, potentially distributing capital gains to remaining shareholders.

For investments held in tax-advantaged accounts like 401(k)s, IRAs, or HSAs, this distinction is irrelevant, as all gains are tax-deferred or tax-free.

Strategic Considerations for Your S&P 500 Investment

Beyond selecting the right fund, how you incorporate the S&P 500 into your broader financial strategy is equally important.

Investment Horizon and Risk Tolerance: Aligning with Your Goals

Investing in the S&P 500 is generally considered a long-term strategy. While the index has a strong history of growth, it is subject to market volatility. Short-term corrections and bear markets are normal occurrences. Investors should ideally have an investment horizon of 5-10 years or more to ride out these fluctuations and fully benefit from the long-term upward trend.

Assess your personal risk tolerance. While diversified, the S&P 500 is 100% equity. If significant market downturns cause you undue stress or prompt impulsive selling, it might be wise to combine your S&P 500 allocation with less volatile assets like bonds or cash equivalents.

Dollar-Cost Averaging (DCA): A Prudent Approach

Dollar-cost averaging involves investing a fixed amount of money at regular intervals (e.g., $200 every month), regardless of market conditions. This strategy helps to mitigate the risk of investing a large sum at an unfortunate market peak. When prices are high, your fixed investment buys fewer shares; when prices are low, it buys more shares. Over time, this averages out your purchase price and reduces emotional decision-making. S&P 500 index funds and ETFs are excellent vehicles for employing a DCA strategy.

Where to Hold Your S&P 500 Investment: Account Types

The type of account you use to hold your S&P 500 investment significantly impacts its tax treatment:

- Taxable Brokerage Accounts: These offer flexibility but subject investment gains (dividends and capital gains) to taxation in the year they are realized. As discussed, ETFs can offer tax advantages here.

- Tax-Advantaged Accounts (IRAs, 401(k)s, HSAs): These accounts offer significant tax benefits, such as tax-deferred growth or tax-free withdrawals in retirement. Maximize contributions to these accounts first, as the tax savings can dramatically enhance your long-term returns, regardless of whether you choose an ETF or a mutual fund.

Diversification Beyond the S&P 500: A Holistic Portfolio

While the S&P 500 offers excellent diversification within U.S. large-cap equities, it is not a complete portfolio on its own. A truly diversified portfolio often includes:

- International Stocks: To gain exposure to global economic growth and reduce reliance on a single country’s market.

- Bonds: To provide stability, generate income, and act as a counterbalance to stocks during market downturns.

- Other Asset Classes: Depending on your goals, this might include real estate, commodities, or alternative investments.

The S&P 500 should be viewed as a core component of a well-rounded portfolio, not the entirety of it.

Conclusion

The question “Which S&P 500 to buy?” ultimately leads to a choice between highly similar, low-cost investment vehicles. For most long-term investors, the difference between a top-tier S&P 500 ETF and a leading S&P 500 index mutual fund will be minimal in terms of performance, especially after accounting for ultra-low expense ratios.

Your decision should hinge on practical considerations:

- Cost: Prioritize funds with the lowest expense ratios (ideally below 0.05%).

- Trading Preference: Do you prefer the intraday flexibility of ETFs or the set-it-and-forget-it simplicity of mutual funds for regular contributions?

- Account Type: For taxable accounts, ETFs might offer a slight tax efficiency edge. For retirement accounts, this difference is negligible.

- Provider Loyalty: If you already have accounts with Vanguard, Fidelity, or Schwab, choosing their respective S&P 500 offerings can streamline management.

Regardless of your choice, committing to a consistent investment strategy, embracing dollar-cost averaging, and maintaining a long-term perspective are far more impactful than agonizing over fractional differences between highly efficient S&P 500 funds. Investing in the S&P 500 is a proven path to long-term wealth creation; the key is to start and stay invested.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.