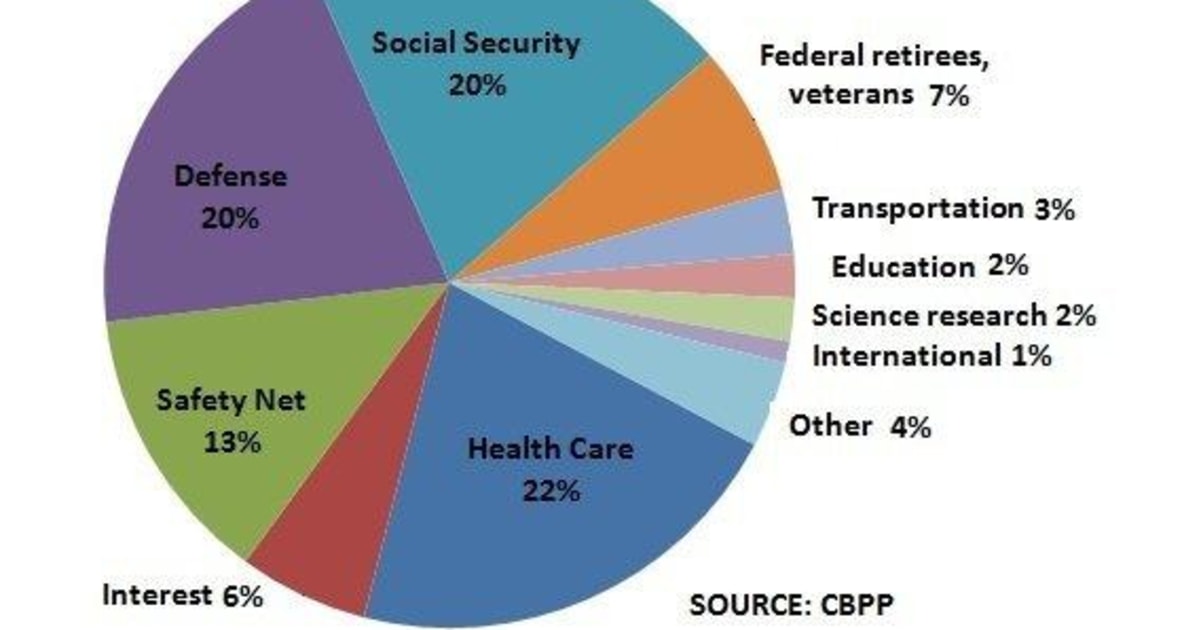

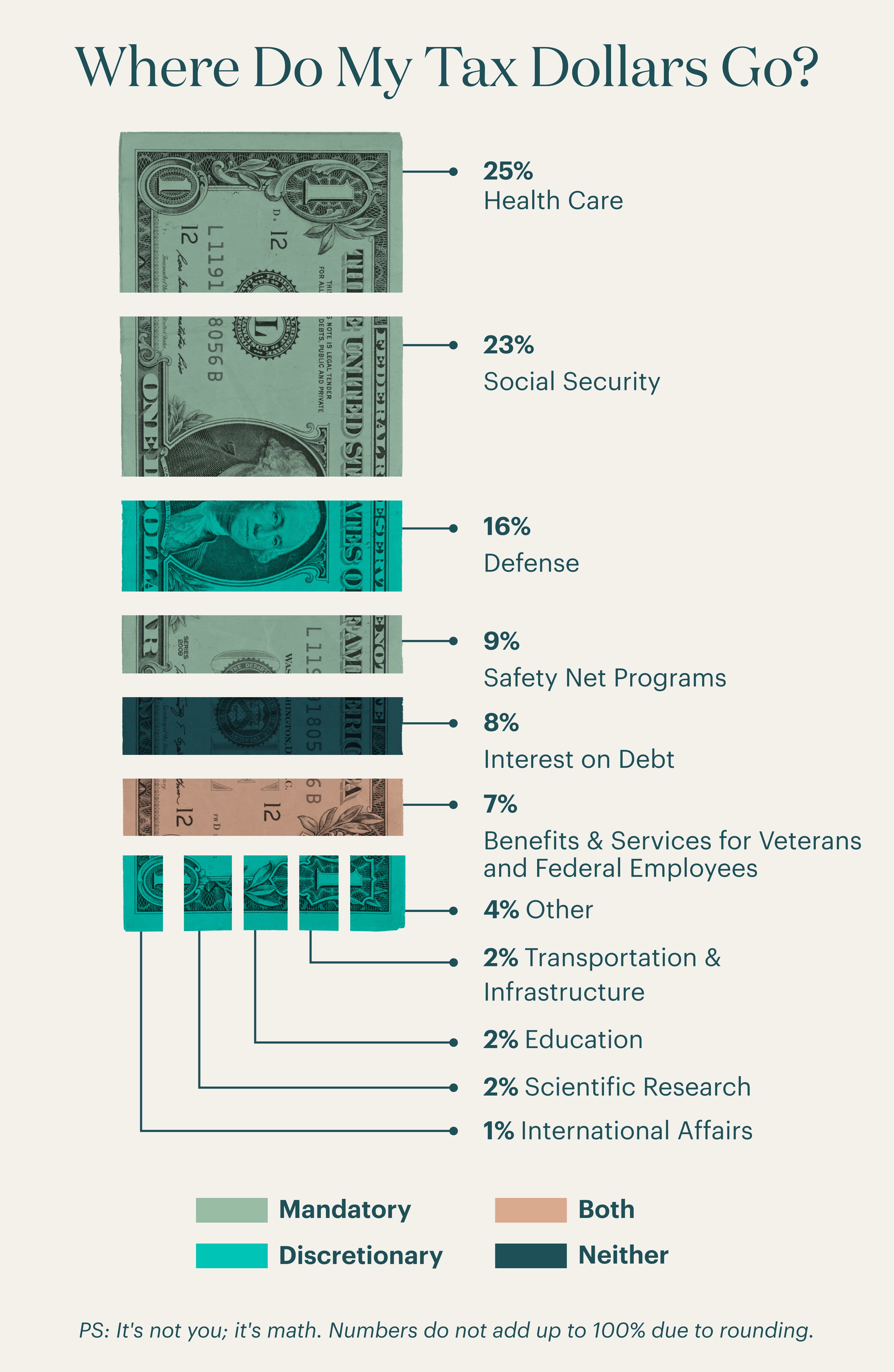

Navigating the landscape of federal tax obligations is a cornerstone of responsible personal and business finance. Whether you are an individual filer, a freelancer, or a small business owner, understanding exactly where and how to pay federal taxes is essential for maintaining a healthy financial profile. The Internal Revenue Service (IRS) has modernized its infrastructure significantly over the last decade, moving away from a purely paper-based system toward a sophisticated digital ecosystem.

Choosing the right payment method is not just a matter of convenience; it is a strategic financial decision. The method you choose can affect your cash flow, your record-keeping accuracy, and even your eligibility for certain financial protections. This guide explores the diverse avenues available for fulfilling your federal tax obligations, categorized by their utility, speed, and impact on your broader financial strategy.

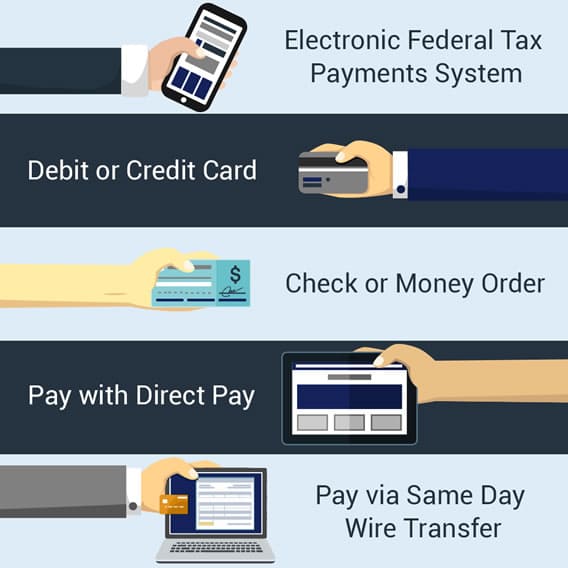

1. Digital Payment Portals: The Efficiency of IRS Direct Pay and EFTPS

In the modern financial era, digital transactions are the gold standard for speed and security. For federal taxes, two primary systems dominate the landscape: IRS Direct Pay and the Electronic Federal Tax Payment System (EFTPS).

IRS Direct Pay for Individuals

IRS Direct Pay is the most straightforward option for individual taxpayers. It allows you to pay your income tax directly from your checking or savings account without any processing fees. This tool is ideal for those filing Form 1040, as well as for making estimated tax payments or paying for extensions.

The beauty of Direct Pay lies in its simplicity. You do not need to create an account or remember a password; you simply verify your identity using information from a previous year’s tax return. Once the payment is authorized, you receive an immediate confirmation number, which serves as a vital digital receipt for your financial records.

The Electronic Federal Tax Payment System (EFTPS) for Businesses

While Direct Pay is tailored for individuals, EFTPS is the powerhouse for businesses and high-net-worth individuals with complex tax requirements. Unlike Direct Pay, EFTPS requires a formal registration process, which includes the mailing of a physical PIN to your registered address for enhanced security.

EFTPS is particularly useful for paying corporate taxes, employment taxes (Form 941), and excise taxes. From a financial management perspective, EFTPS offers a “payment history” feature that allows users to track their payments over the last 15 months. This level of transparency is invaluable for business owners who need to reconcile their books and ensure they are meeting their quarterly obligations without error.

Advantages of Digital Tracking and Instant Confirmation

The shift toward digital portals offers more than just convenience; it provides a robust audit trail. In personal finance, “leakage”—money spent or moved without proper documentation—is a common pitfall. By utilizing digital portals, you create an instantaneous, time-stamped record of your transaction. This reduces the risk of penalties due to lost mail or processing delays at the IRS service centers, ensuring your funds are credited to your account on the exact day you intended.

2. Credit, Debit, and Mobile: Leveraging Modern Financial Tools

For many taxpayers, the ability to use a credit or debit card offers a layer of flexibility that bank transfers cannot. While the IRS does not collect fees for these transactions, it utilizes third-party payment processors that do.

Third-Party Processors and Associated Fees

When you choose to pay by card, you are redirected to one of several IRS-authorized payment processors. It is important to understand the fee structure: debit card payments usually carry a flat fee (often under $3.00), while credit card payments incur a percentage-based fee, typically ranging from 1.8% to 2.0%.

From a financial planning standpoint, you must weigh the cost of these fees against the benefits. If you are using a rewards card that offers 2% cash back, the fee and the reward may cancel each other out, making it a “neutral” transaction that allows you to keep cash in your high-yield savings account for a few extra weeks.

Paying via Mobile Apps (IRS2Go)

For the mobile-first generation, the IRS2Go app provides a streamlined interface for making payments. Available on both iOS and Android, the app acts as a mobile gateway to Direct Pay and the authorized card processors. This tool is particularly useful for “gig economy” workers who may need to make quick estimated payments while on the go. The integration of mobile technology into tax compliance reflects a broader trend in financial tools where accessibility is prioritized to improve user compliance and reduce friction.

The Pros and Cons of Using Credit for Tax Liabilities

Using a credit card to pay federal taxes can be a strategic move if managed correctly. It can provide a short-term “float,” allowing you to meet a tax deadline even if your liquid cash is tied up in other investments or business expenses. However, this should only be done if you can pay off the credit card balance before interest accrues. If you carry the balance, the double-digit interest rates of most credit cards will far exceed any IRS underpayment penalties, leading to a net loss in your overall net worth.

3. Traditional Methods: When Mail and In-Person Payments Still Make Sense

Despite the digital revolution, traditional payment methods remain available for those who prefer tangible records or who lack access to digital banking.

Paying by Check or Money Order

You can still pay your federal taxes by mailing a check or money order to the IRS. When using this method, it is crucial to include Form 1040-V (Payment Voucher). The check must be made out to the “United States Treasury” and should include your Social Security number, the tax year, and the specific form number in the memo line.

From a security perspective, mailing a check is higher risk than digital transfers. To mitigate this, financial advisors recommend using certified mail with a return receipt requested. This provides legal proof that your payment was sent on time, which is critical if the IRS claims a payment was late.

Cash Payments at Retail Partners

In an effort to be inclusive of the unbanked or underbanked population, the IRS has partnered with retail chains like 7-Eleven, Walgreens, and CVS to accept cash payments. This process requires an online pre-verification through a provider like ACI Payments, after which the taxpayer receives a code to present at the store. There is usually a daily limit (around $1,000) and a small convenience fee. While not the most efficient for large sums, it serves as a vital financial tool for those who operate primarily in a cash economy.

Ensuring Compliance and Postmark Deadlines

The “mailbox rule” is a fundamental concept in tax law. If a payment is postmarked by the due date, it is generally considered on time, even if it reaches the IRS days later. However, relying on this requires precision. If you are making a substantial payment via mail, the risk of a lost envelope can lead to significant stress and potential financial penalties. Consequently, while traditional methods are a valid “where” for your taxes, they are increasingly viewed as a secondary option to more secure electronic methods.

4. Strategic Financial Planning for Tax Liabilities

Identifying where to pay is only half the battle; the other half is managing how and when to pay to maintain financial stability.

Setting Up Installment Agreements and Payment Plans

If you find yourself in a position where you cannot pay your federal taxes in full, the IRS offers Online Payment Agreements. These can be short-term (paying within 180 days) or long-term (monthly installments).

Strategically, an installment agreement is often better than putting a massive tax bill on a high-interest credit card. While the IRS charges interest and a setup fee, the rates are often more favorable than those offered by commercial lenders. Proactively setting up a plan demonstrates financial responsibility and prevents the IRS from initiating more aggressive collection actions, such as levies or liens.

Managing Estimated Quarterly Payments

For business owners and freelancers, paying taxes is not an annual event but a quarterly obligation. Using the digital tools mentioned earlier to automate these payments can prevent “tax season shock.” By calculating your estimated liability and paying it in four installments, you ensure that you aren’t hit with a massive bill in April that could deplete your business’s operating capital. This disciplined approach to cash flow is a hallmark of successful financial management.

Incorporating Tax Payments into Your Personal Budget

Ultimately, federal taxes should be treated as a non-negotiable line item in your budget. By utilizing the various “where” options—whether it’s a monthly “set-aside” in a dedicated savings account or using EFTPS to schedule future payments—you take control of your financial destiny. Modern financial tools have made it easier than ever to ensure that your obligations to the Treasury are met with minimal friction, allowing you to focus your energy on growing your wealth and managing your assets.

In conclusion, the question of “where to pay federal taxes” has multiple answers depending on your specific financial situation. From the high-speed efficiency of IRS Direct Pay to the flexible but fee-based card processors, and even the traditional mail-in check, each method has its place in a well-rounded financial strategy. By choosing the method that offers the best balance of security, record-keeping, and cash-flow management, you can navigate tax season with confidence and professional precision.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.