The annual ritual of tax filing often culminates in a single, high-stakes question: “Where do you send IRS payments?” For millions of Americans, this isn’t just a logistical query—it is a critical step in maintaining financial health and avoiding the heavy hand of federal penalties. In an era where the Internal Revenue Service (IRS) is caught between legacy paper-based systems and a rapid digital transformation, knowing exactly how and where to direct your funds is a vital skill in personal and business finance.

Whether you are a freelancer making quarterly estimated payments, a small business owner settling payroll taxes, or an individual taxpayer resolving a balance due on a 1040 return, the “where” and “how” of your payment can impact your liquidity and your peace of mind. This guide explores the modern landscape of IRS payments, categorizing the options from digital portals to traditional mail, while offering strategic insights into managing your tax-related cash flow.

Digital Payment Channels: Navigating the IRS Modernization

The IRS has made significant strides in moving away from paper checks. For the modern taxpayer, digital channels are the preferred method because they offer immediate confirmation, higher security, and better integration with personal financial tracking software.

IRS Direct Pay for Individuals

For the average individual taxpayer, IRS Direct Pay is the most efficient tool available. This service allows you to pay your income tax directly from a checking or savings account without any processing fees. It is specifically designed for 1040 series forms, estimated taxes (1040-ES), and extensions.

The primary advantage of Direct Pay is that it requires no registration. You simply verify your identity using information from a previous year’s tax return. From a financial management perspective, Direct Pay allows for “look-back” accuracy, ensuring that the payment is applied to the correct tax year and the specific type of liability you intend to settle.

EFTPS: The Gold Standard for Businesses

The Electronic Federal Tax Payment System (EFTPS) is a free service provided by the U.S. Department of the Treasury. While individuals can use it, it is the cornerstone of business tax compliance. If you are managing payroll taxes (Form 941) or corporate income tax (Form 1120), EFTPS is often a requirement rather than an option.

Unlike Direct Pay, EFTPS requires a formal enrollment process, which includes receiving a PIN via physical mail. Once set up, however, it offers unparalleled tracking. You can schedule payments up to 365 days in advance, which is a powerful tool for business cash flow forecasting. By scheduling payments to exit your account exactly on the due date, you can maximize the interest-earned on your capital until the very last moment.

Digital Wallets and Credit Card Payments

In recent years, the IRS has expanded its acceptance of third-party payment processors. Taxpayers can now use digital wallets like PayPal or Click to Pay, as well as standard credit and debit cards.

From a personal finance standpoint, this option requires a cost-benefit analysis. While the IRS does not charge a fee for card payments, the third-party processors do. These fees typically range from 1.82% to 1.98% for credit cards. For those seeking to maximize credit card rewards or “churn” sign-up bonuses, the fee might be outweighed by the value of the points earned. However, for most, the convenience of a credit card is a high-price alternative to the free ACH transfers provided by Direct Pay.

The Traditional Route: Sending Payments via Mail

Despite the digital push, thousands of taxpayers still prefer—or are required—to send physical checks or money orders. The “where” in this scenario becomes significantly more complex, as the IRS maintains multiple processing centers across the United States.

Matching Your Location to the Correct Service Center

The IRS divides the United States into various regions for mail processing. Where you send your payment depends entirely on two factors: the state in which you live and whether or not you are enclosing a tax return with your payment.

For example, a taxpayer in California sending a payment with a Form 1040 might send it to a center in Fresno, while a taxpayer in New York might send theirs to a center in Philadelphia or Kansas City. These addresses change periodically based on the workload of the IRS service centers. It is imperative to check the “Where to File” charts on the official IRS website or the instructions for Form 1040-V (the Payment Voucher) to ensure your check isn’t delayed in a regional mail loop.

The Importance of the Payment Voucher (Form 1040-V)

If you choose to mail a check, you should never send it “naked.” The Form 1040-V is a small statement that tells the IRS exactly who you are and where the money should go. Without this voucher, your check may be manually processed, which increases the risk of it being credited to the wrong tax year or the wrong Social Security Number.

When writing the check, the financial best practice is to make it payable to the “United States Treasury” (not “IRS”). Include your name, address, daytime phone number, Social Security Number (or ITIN), and the tax year/form number in the memo line. This redundancy is your primary defense against administrative errors.

Certified Mail and Proof of Timely Filing

When sending significant sums of money through the mail, the “where” is less important than the “when.” Under the “Timely Mailing Treated as Timely Filing/Paying” rule, a payment is considered on time if it is postmarked by the due date.

To protect your financial interests, always send IRS payments via Certified Mail with a Return Receipt. This provides legal proof that the payment was sent and received. In the event of a lost check or an IRS system error, this receipt is the only evidence that can save you from late-payment penalties and interest.

Strategic Timing and Cash Flow Management

In the world of personal and business finance, “where” you send your money is often dictated by “when” you are required to pay. Effective tax management involves more than just a lump-sum payment in April; it requires a year-round strategy.

Quarterly Estimated Payments

For the self-employed, freelancers, and investors, the IRS operates on a “pay-as-you-go” system. These payments are generally sent four times a year: April 15, June 15, September 15, and January 15.

Strategically, these payments should be treated as a fixed business expense. Sending these payments to the IRS via EFTPS or Direct Pay allows for a more granular view of your net income. By settling your tax liability in real-time, you avoid the “tax cliff” in April, where a lack of liquidity can force a taxpayer to take out high-interest loans to pay the government.

Avoiding Underpayment Penalties

The IRS expects you to pay at least 90% of your current year’s tax or 100% of the previous year’s tax (whichever is smaller) throughout the year. If you fail to send your payments to the correct “location” (in this case, the specific quarterly deadline), you may be hit with an underpayment penalty.

A sophisticated financial strategy involves calculating your “safe harbor” amount. By ensuring your estimated payments meet the 100% (or 110% for high earners) of the prior year’s tax threshold, you can keep the rest of your money in high-yield savings accounts or investments until April 15, effectively earning interest on money that will eventually belong to the IRS.

Installment Agreements and Payment Plans

Sometimes, the question isn’t where to send the payment, but how to send it when you don’t have the full amount. The IRS offers online payment plans for those who owe $50,000 or less in combined income tax, penalties, and interest.

Choosing an installment agreement is a strategic financial move. While it incurs a setup fee and interest, it is significantly cheaper than the failure-to-pay penalty, which accrues at 0.5% per month. These payments are typically sent via a setup for automatic “Direct Debit,” ensuring you never miss a deadline and keeping your credit score and financial reputation intact.

Security Protocols: Protecting Your Financial Information

Sending money to a government entity makes you a prime target for sophisticated financial scams. Ensuring your payment reaches the IRS—and not a fraudster—is a critical component of digital security and personal finance.

Recognizing “Pay-to-IRS” Scams

The IRS will never initiate contact with taxpayers by email, text messages, or social media channels to request personal or financial information. Furthermore, the IRS does not accept payments via wire transfer (like Western Union), prepaid debit cards, or gift cards.

If you receive a request to send a payment to a “holding account” or a specific person’s name, it is a scam. Legitimate payments are only sent through the portals mentioned above (Direct Pay, EFTPS, or authorized processors) or to “United States Treasury” via physical mail to a verified IRS address.

Safe Browser Practices for Financial Transactions

When sending payments online, always ensure you are on a .gov website. Look for the padlock symbol in the browser bar and verify the URL starts with https://. Avoid using public Wi-Fi networks when making tax payments, as these are vulnerable to “man-in-the-middle” attacks where hackers can intercept your banking details. Using a VPN (Virtual Private Network) adds an extra layer of encryption to your financial data.

Verification of Payment Success

Your responsibility doesn’t end when you click “submit” or drop the check in the mail. Part of sound financial management is verifying that the transaction was successful.

- For Digital Payments, save the confirmation number immediately.

- For Checks, monitor your bank account to see when the check is cashed.

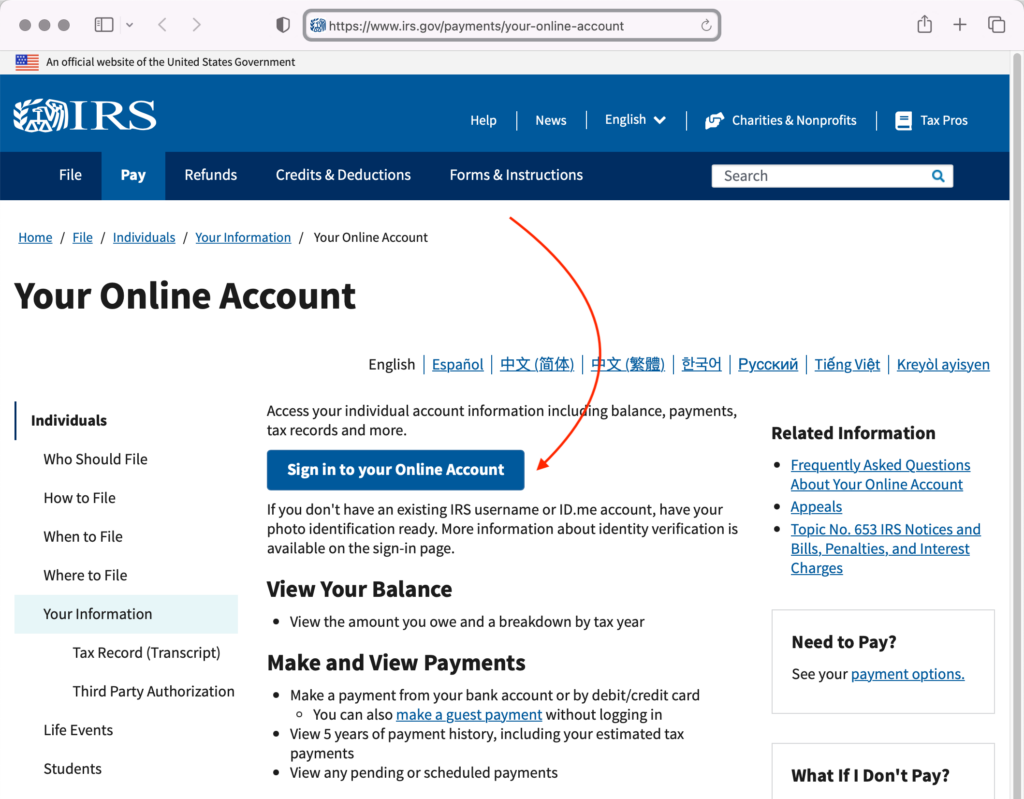

- For General Verification, you can log in to your “IRS Online Account” on the official website. It usually takes 1–3 weeks for a payment to reflect in your official transcript.

Conclusion: Achieving Financial Peace of Mind

Understanding where to send IRS payments is about more than just finding an address; it is about mastering the logistics of your financial life. In the modern age, the shift toward digital platforms like IRS Direct Pay and EFTPS offers taxpayers unprecedented control, speed, and security. However, the traditional mail system remains a fallback for those who prefer physical documentation and the “postmark rule.”

By aligning your payment methods with your broader financial strategy—optimizing for cash flow, avoiding penalties through estimated payments, and maintaining rigorous security—you transform tax season from a period of uncertainty into a streamlined administrative process. Whether you are clicking a button or licking a stamp, the goal remains the same: accurate, timely, and secure settlement of your obligations to the U.S. Treasury.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.