Deciding when to claim Social Security benefits is arguably the most significant financial decision most Americans will make in their lifetime. For many, Social Security represents a guaranteed, inflation-adjusted stream of income that serves as the foundation of their retirement floor. However, the timing of this decision is fraught with complexity, involving a delicate balance of actuarial math, personal health, tax implications, and lifestyle goals.

While the earliest age to claim is 62, and the latest age to see a benefit increase is 70, the “correct” age is rarely the same for two different individuals. This guide explores the strategic nuances of Social Security timing to help you optimize your long-term financial security.

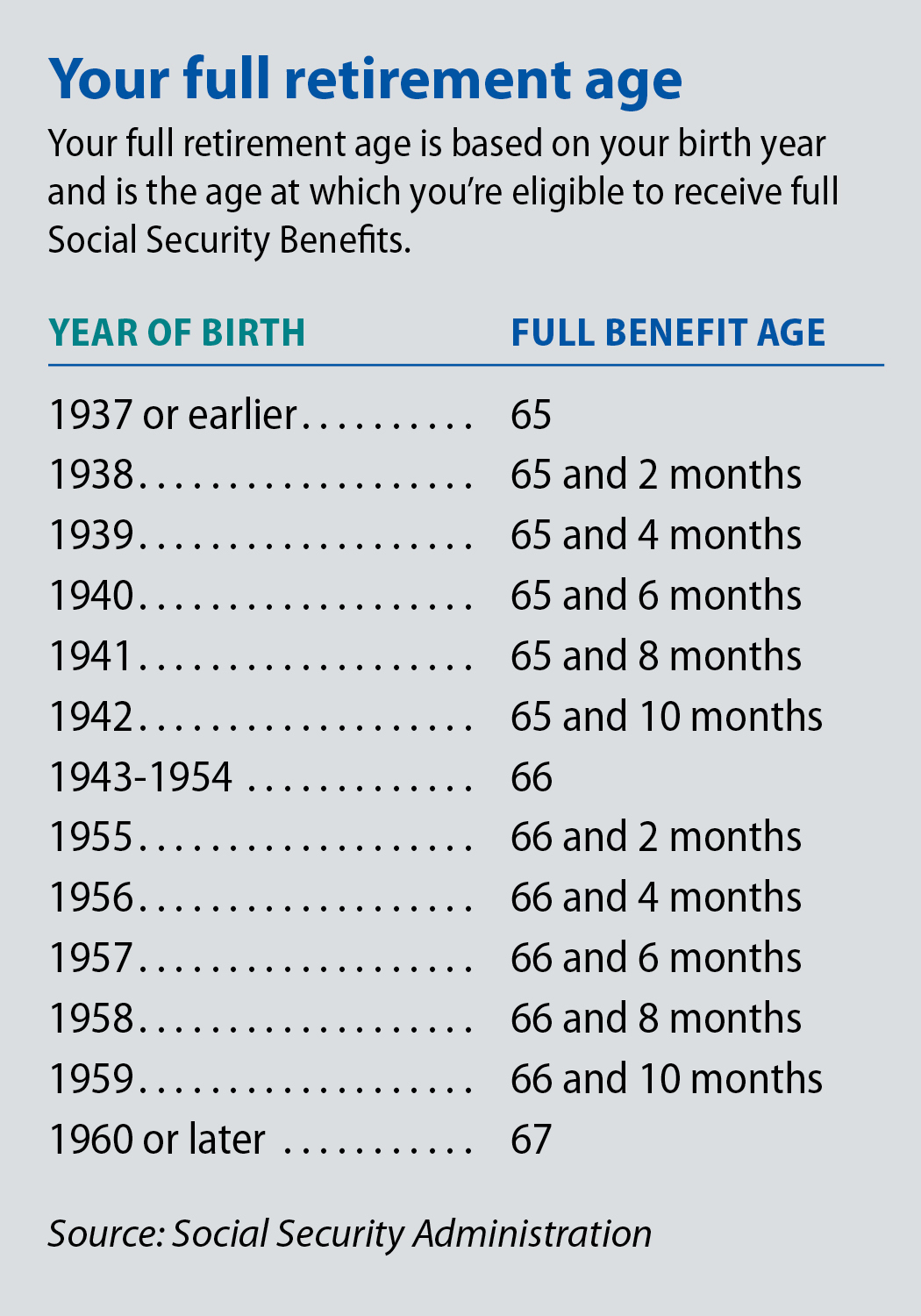

Understanding the Foundation: Full Retirement Age and the Impact of Timing

To make an informed decision, one must first understand the benchmark set by the Social Security Administration: the Full Retirement Age (FRA). Your FRA is the age at which you are entitled to 100% of your primary insurance amount (PIA), determined by your birth year. For those born in 1960 or later, the FRA is 67.

What is Full Retirement Age?

The FRA is the pivot point for all Social Security calculations. If you claim before this age, your monthly check is permanently reduced. If you claim after this age, your monthly check is permanently increased. Understanding your specific FRA is the first step in calculating the “opportunity cost” of your timing.

The Financial Cost of Filing Early

Filing as early as possible—at age 62—offers the immediate gratification of cash flow, but it comes at a steep price. For someone with an FRA of 67, claiming at 62 results in a permanent reduction of roughly 30% in monthly benefits. This reduction is designed to be “actuarially neutral” if you live to average life expectancy, but for many who live longer, the cumulative loss of income can be hundreds of thousands of dollars over a lifetime.

The Reward for Delaying Benefits

Conversely, delaying benefits beyond your FRA triggers “Delayed Retirement Credits.” For every year you wait past your FRA up until age 70, your benefit increases by approximately 8% annually. This is a guaranteed, simple interest return that is virtually impossible to find in any other fixed-income investment. By waiting from age 67 to 70, a retiree can increase their monthly payout by 24%, providing a significantly higher “real” income for the remainder of their life.

Key Factors Influencing Your Decision

The mathematical advantage of waiting must be weighed against the realities of your personal life. Financial advisors often suggest looking at three primary pillars: health, wealth, and work.

Life Expectancy and Health Considerations

Social Security is essentially insurance against longevity. If you are in excellent health and have a family history of living into your 90s, the “break-even” analysis strongly favors waiting until age 70. However, if you have chronic health issues or a shorter life expectancy, claiming early may be the most rational choice to ensure you receive as much from the system as possible while you are still able to enjoy it.

Financial Need and Cash Flow Requirements

Theory often clashes with reality. If you have lost your job, have insufficient retirement savings, or are facing immediate debt, claiming Social Security at 62 may be a necessity rather than a choice. On the other hand, if you have a robust 401(k) or IRA, it may be beneficial to draw down those taxable assets first while allowing your Social Security benefit to grow at that guaranteed 8% rate.

Employment Status and the Earnings Test

A common mistake is claiming benefits early while continuing to work a high-paying job. If you are under your FRA and earn more than a certain threshold ($22,320 in 2024), the Social Security Administration will withhold $1 in benefits for every $2 you earn above that limit. While these withheld benefits are eventually added back to your check once you reach FRA, the immediate “tax” on your benefits can make early claiming a poor tactical move for the still-employed.

Strategic Considerations for Couples and Dependents

The decision-making process becomes exponentially more complex for married couples. Because Social Security offers spousal and survivor benefits, a husband and wife should not view their benefits in isolation but as a combined household asset.

Spousal Benefits and Coordination

A spouse is generally entitled to up to 50% of the other spouse’s PIA. If one spouse earned significantly more over their lifetime, it might make sense for the lower-earning spouse to claim their own benefit early to provide immediate cash flow, while the higher-earning spouse delays until age 70. This maximizes the total “pool” of wealth available to the couple.

Survivor Benefits: Protecting the Long-Term

The most critical aspect of the “couples’ strategy” is the survivor benefit. When one spouse passes away, the surviving spouse is entitled to the higher of the two checks. By the higher earner delaying until age 70, they are effectively “buying” a larger life insurance policy for their spouse. This ensures that the survivor—who may face increased healthcare costs or the loss of a pension—has the highest possible monthly income for the rest of their life.

Tax Implications and Investment Strategies

The interaction between Social Security and the IRS is a crucial part of the “Money” niche that is often overlooked. Your “provisional income”—a combination of your adjusted gross income, tax-exempt interest, and 50% of your Social Security benefits—determines how much of your benefit is taxable.

Is Social Security Taxable?

For many retirees, Social Security benefits are not entirely tax-free. If your provisional income exceeds certain thresholds ($32,000 for joint filers), up to 85% of your benefits may be subject to federal income tax. Strategic planners often time their Social Security claims to coincide with “low-income years” or use Roth IRA conversions in the years before claiming to reduce future taxable income.

The “Break-Even” Analysis

A break-even analysis calculates the age at which the total cumulative benefits of waiting (the larger check) surpass the total cumulative benefits of starting early (more checks). Typically, the break-even point for waiting until 70 versus starting at 62 is around age 78 to 80. If you believe you will live past 80, the “math” says wait. If not, the math says take it now.

Opportunity Cost and Reinvesting Benefits

Some investors argue for taking benefits at 62 and investing the proceeds in the stock market. While the S&P 500 has historically returned more than 8% over long periods, this strategy introduces market risk. Social Security’s 8% increase is guaranteed and inflation-adjusted (via COLAs), making it a “risk-free” return that is almost impossible to beat on a risk-adjusted basis.

Common Pitfalls and How to Avoid Them

Despite the wealth of information available, many people make emotional rather than financial decisions regarding Social Security. Understanding these pitfalls is essential for a sound financial plan.

Falling for the “System Failure” Myth

A frequent reason cited for claiming at 62 is the fear that Social Security will “go bankrupt.” While the trust funds are projected to face shortfalls in the mid-2030s, this does not mean benefits will vanish; it means they may be reduced (likely to around 77-80% of scheduled benefits) if Congress does not act. Claiming early out of fear often locks in a permanent 30% reduction today to avoid a potential 20% reduction tomorrow—a logic that rarely pays off.

Neglecting the Role of Inflation

Social Security is one of the few retirement income sources with a Cost-of-Living Adjustment (COLA). Because the COLA is a percentage of your benefit, a larger base benefit (from waiting) leads to larger annual raises. Over 20 or 30 years of retirement, the compounding effect of COLAs on a higher age-70 benefit can create a massive difference in purchasing power compared to a reduced age-62 benefit.

Choosing the Path of Least Resistance

Many people claim Social Security simply because they reach 62 and “can.” However, retirement planning is about the long game. Before filing, consult with a financial advisor or use a Social Security optimization tool to model different scenarios. A few months of extra planning can result in tens of thousands of dollars of extra income in your later years.

In conclusion, there is no universal “best” age to take Social Security. It is a deeply personal financial decision that depends on your health, your marital status, your tax bracket, and your other sources of income. By shifting the perspective from “How soon can I get my money?” to “How can I maximize my lifetime wealth?” you can ensure that Social Security serves its true purpose: providing financial dignity and security throughout your retirement years.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.