The phrase “stock market crash” evokes a visceral sense of fear and uncertainty among investors. It conjures images of rapid wealth destruction, economic turmoil, and shattered financial dreams. While the stock market is a powerful engine for wealth creation over the long term, its journey is rarely a smooth, upward trajectory. Instead, it is punctuated by periods of volatility, corrections, and, on occasion, full-blown crashes. Understanding when and why these dramatic downturns occur is not about predicting the impossible, but rather about recognizing patterns, managing risk, and preparing for the inevitable cyclical nature of financial markets. Though impossible to time with precision, stock market crashes are not entirely random events. They are often the culmination of specific economic pressures, geopolitical tensions, and shifts in investor sentiment. This article will delve into the characteristics of market crashes, explore their common triggers, examine historical precedents, and, most importantly, provide strategies for investors to navigate these turbulent periods.

Defining a Stock Market Crash and Correction

Before delving into the ‘when,’ it’s crucial to establish a clear understanding of what constitutes a market crash and how it differs from more common market fluctuations. The financial lexicon is rich with terms describing market downturns, and distinguishing between them is vital for informed analysis and decision-making.

What Constitutes a Crash?

A stock market crash is characterized by a sudden, often dramatic, and unexpected drop in stock prices across a significant portion of the market. While there’s no universally agreed-upon percentage, a general rule of thumb defines a crash as a rapid decline of 20% or more in major market indices (like the S&P 500 or Dow Jones Industrial Average) within a very short period, often days or weeks. This sharp decline is typically accompanied by widespread panic, forced selling, and a significant loss of investor confidence. Crashes are distinct from bear markets, which are generally defined as a sustained decline of 20% or more from recent highs over a longer period, often months or even years. While a crash can initiate a bear market, the defining feature of a crash is its speed and severity. Historical examples include Black Monday in 1987, the dot-com bust of 2000, and the Global Financial Crisis of 2008, each illustrating varying scales of market destruction.

Distinguishing from a Market Correction

A market correction, in contrast to a crash, is a more common and generally less severe downturn. It typically involves a decline of 10% to 20% from a market index’s most recent peak. Corrections are a normal, healthy, and often necessary part of the market cycle. They serve to re-evaluate asset prices, shake out speculative excesses, and prevent markets from becoming excessively overvalued. Unlike crashes, which are often sparked by unforeseen events or the bursting of bubbles, corrections can occur due to a myriad of factors: rising interest rates, slowing economic growth, minor geopolitical tensions, or even just profit-taking after a strong bull run. While uncomfortable for investors, corrections rarely lead to widespread panic or systemic failures and are typically shorter-lived than crashes.

Key Economic and Geopolitical Triggers of Market Crashes

Stock market crashes are rarely solitary events without preceding conditions. They are often the catastrophic endpoint of a chain of economic imbalances, policy missteps, or unforeseen external shocks that erode confidence and trigger a cascade of selling.

Economic Bubbles and Overvaluation

One of the most classic precursors to a market crash is the formation and subsequent bursting of an economic bubble. A bubble occurs when asset prices, whether stocks, real estate, or commodities, detach from their underlying fundamental value and are driven higher by speculation, herd mentality, and irrational exuberance. Investors, fueled by the fear of missing out (FOMO) and the “greater fool theory” (the belief that someone else will pay even more for an overvalued asset), bid prices to unsustainable levels. When confidence wavers, or an external event punctures the speculative fervor, a rapid sell-off ensues, leading to a crash. The dot-com bubble of the late 1990s and the U.S. housing bubble leading to the 2008 financial crisis are prime examples of this phenomenon.

Interest Rate Hikes and Monetary Policy Shifts

Central banks, such as the U.S. Federal Reserve, use monetary policy tools, primarily interest rates, to manage inflation and economic growth. When inflation becomes a concern, central banks raise interest rates to cool down the economy. While necessary, aggressive or rapid interest rate hikes can significantly impact corporate profitability and investor sentiment. Higher borrowing costs reduce corporate earnings, making future growth less attractive. They also make bonds and other fixed-income investments more appealing relative to stocks, causing a shift in investment flows. If monetary tightening is perceived as too aggressive or risks tipping the economy into recession, it can trigger a sharp market sell-off.

Geopolitical Events and Black Swan Incidents

The global economy is intricately linked, and major geopolitical events can send shockwaves through financial markets. Wars, political instability in key regions, terrorist attacks, and, more recently, global pandemics (like COVID-19 in 2020) are “black swan” events—unpredictable and highly impactful. These events introduce extreme uncertainty, disrupt global supply chains, reduce consumer and business confidence, and can lead to immediate and widespread investor panic. The immediate aftermath of such events often sees a sharp flight to safety, with investors dumping riskier assets like stocks in favor of more stable investments like government bonds or gold.

Systemic Financial Risks and Regulatory Failures

The interconnectedness of the modern financial system means that failures in one area can quickly cascade throughout the entire system. Systemic risks, such as those exposed during the 2008 Global Financial Crisis, arise when the collapse of a major financial institution or a widespread issue within a critical sector (like the subprime mortgage market) threatens the stability of the entire financial system. Regulatory failures or inadequate oversight can allow these risks to build unchecked, leading to a crisis of confidence. When trust evaporates between financial institutions, credit markets freeze, and the flow of money grinds to a halt, prompting widespread market fear and selling.

The Role of Investor Psychology and Market Dynamics

While economic fundamentals and external events provide the fertile ground for a crash, the actual descent is often fueled by the powerful, sometimes irrational, forces of human psychology and the mechanics of market trading.

Fear, Panic, and Herd Behavior

Markets are not purely rational entities; they are driven by human participants, and human psychology plays a profound role, especially during times of stress. When prices begin to fall, fear can quickly transform into panic. Investors, witnessing their portfolios shrink, may abandon their long-term strategies and succumb to the urge to sell immediately, fearing even greater losses. This panic selling can create a self-fulfilling prophecy, accelerating the downturn. Herd behavior amplifies this effect, as individuals observe others selling and feel compelled to follow suit, regardless of underlying fundamentals. The rapid dissemination of news and social media in the modern age can exacerbate these psychological dynamics, leading to faster and more intense market reactions.

Liquidity Crises and Margin Calls

In a rapidly declining market, a liquidity crisis can emerge. This occurs when there are significantly more sellers than buyers, making it difficult to sell assets without significantly driving down their price. As prices fall, investors who have bought securities on margin (borrowed money from their broker) may face margin calls. A margin call demands that the investor deposit additional funds to cover potential losses or sell assets to reduce their leveraged position. Forced selling due to margin calls can further depress prices, creating a vicious cycle and accelerating the market’s decline. Automated trading algorithms, designed to react to price movements, can also contribute to flash crashes, where markets drop dramatically in minutes due to rapid, automated selling before recovering somewhat.

Historical Precedents: Learning from Past Crashes

History offers invaluable lessons about the nature of stock market crashes. While each crash has unique triggers and characteristics, recurring themes emerge, highlighting vulnerabilities and the market’s enduring capacity for recovery.

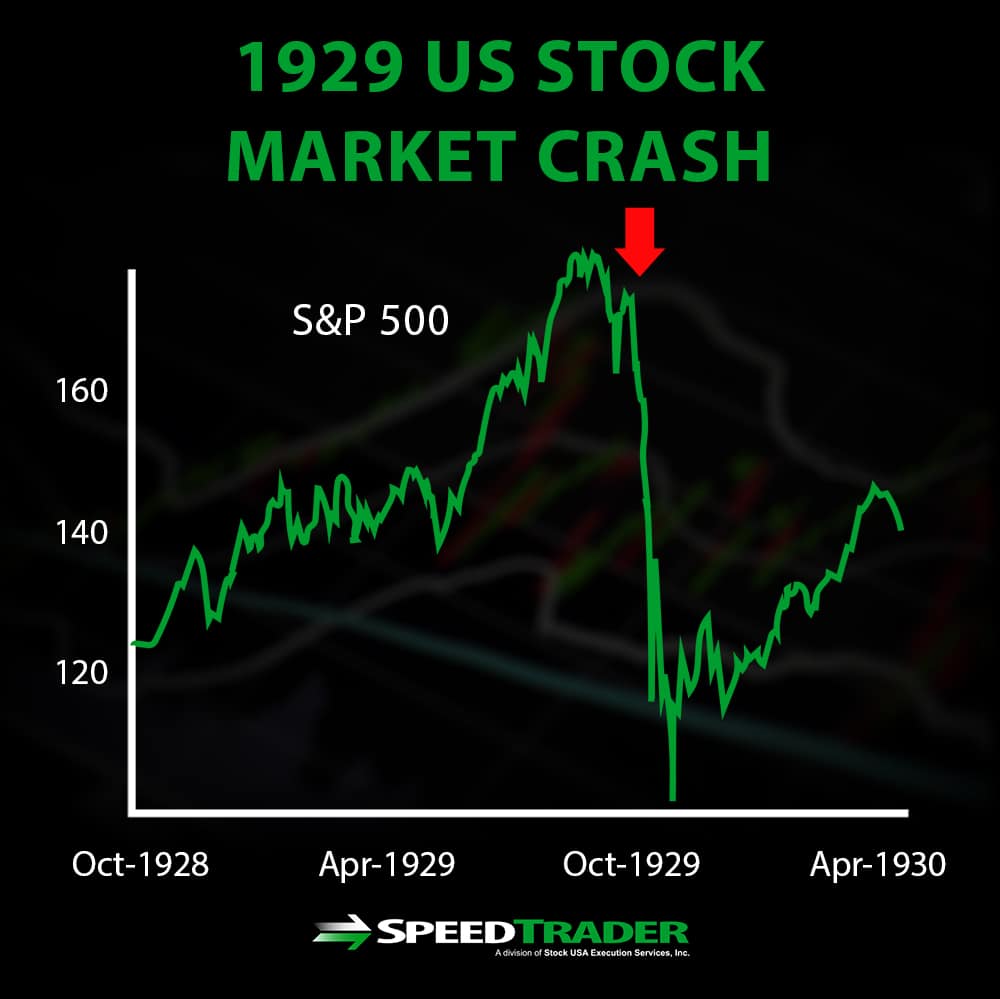

The Great Depression (1929)

The Wall Street Crash of 1929, often dubbed “Black Tuesday,” marked the beginning of the Great Depression. Fueled by rampant speculation, excessive debt, and an unregulated market, the crash saw the Dow Jones Industrial Average lose 89% of its value over three years. Its profound economic and social impact led to significant regulatory changes, including the creation of the Securities and Exchange Commission (SEC).

Black Monday (1987)

On October 19, 1987, global stock markets experienced their largest one-day percentage drop in history, with the Dow Jones Industrial Average falling by 22.6%. The crash was attributed to a combination of factors, including program trading, portfolio insurance strategies, and macroeconomic imbalances. Despite the severity, the market recovered relatively quickly, and the broader economy avoided a recession, demonstrating the resilience of markets and the importance of liquidity.

Dot-Com Bubble Burst (2000-2002)

The late 1990s saw an unprecedented boom in technology and internet-related stocks, driven by speculative excitement rather than profitability. When the bubble burst in early 2000, particularly among NASDAQ-listed companies, trillions of dollars in market value were wiped out. Many internet companies, or “dot-coms,” went bankrupt, and it took several years for the technology sector and broader market to recover fully.

Global Financial Crisis (2008)

Originating from the collapse of the U.S. housing market and widespread subprime mortgage lending, the Global Financial Crisis was a systemic breakdown. Major financial institutions failed, credit markets froze, and a worldwide recession ensued. The stock market experienced a dramatic decline, though unprecedented government interventions and monetary easing eventually stabilized the financial system and paved the way for recovery.

COVID-19 Market Plunge (2020)

The onset of the COVID-19 pandemic triggered an abrupt and severe global market downturn in early 2020. The uncertainty surrounding the virus’s spread, lockdowns, and economic impact led to a rapid 34% drop in the S&P 500 in just 33 days—the fastest bear market in history. However, massive fiscal stimulus and aggressive monetary policy by central banks facilitated an equally rapid, V-shaped recovery, highlighting the impact of policy responses.

Preparing for and Navigating Market Crashes

While the exact timing of a stock market crash remains elusive, savvy investors can adopt strategies to mitigate their impact and even find opportunities amidst the turmoil. The core principle is preparedness and a long-term, disciplined approach.

Diversification and Asset Allocation

The cornerstone of risk management is diversification. By spreading investments across various asset classes—such as stocks, bonds, real estate, and commodities—and within different sectors and geographies, investors can reduce the impact of a downturn in any single area. A well-considered asset allocation, tailored to an individual’s risk tolerance and time horizon, ensures that not all eggs are in one basket. During a stock market crash, for example, bonds often act as a buffer, appreciating in value as investors seek safety.

Long-Term Perspective and Dollar-Cost Averaging

One of the most critical lessons from past crashes is that markets eventually recover. Investors with a long-term horizon (many years or decades) should resist the urge to panic sell during a downturn. Instead, maintaining a steady investment strategy, such as dollar-cost averaging (investing a fixed amount of money at regular intervals), can be highly effective. This strategy means buying more shares when prices are low and fewer when prices are high, potentially leading to a lower average cost per share over time. “Time in the market” consistently outperforms “timing the market.”

Maintaining an Emergency Fund

A robust emergency fund, typically three to six months’ worth of living expenses held in a liquid, easily accessible account, is crucial. This fund provides a financial safety net, ensuring that you don’t have to sell your investments at a loss to cover unexpected expenses during a market downturn or job loss. It separates your short-term cash needs from your long-term investment goals.

Understanding Your Risk Tolerance

Every investor has a unique capacity and willingness to take on risk. Understanding your personal risk tolerance is fundamental to constructing an investment portfolio that you can stick with, even during volatile periods. If you’re highly risk-averse, a more conservative allocation with a higher proportion of bonds might be appropriate. Conversely, those with a higher tolerance for risk and a longer time horizon might allocate more to equities. This self-awareness prevents emotional decisions during market stress.

Seeking Professional Financial Advice

During periods of heightened uncertainty, the guidance of a qualified financial advisor can be invaluable. An advisor can help you objectively assess your financial situation, establish appropriate goals, craft a diversified portfolio, and, perhaps most importantly, provide emotional support and prevent impulsive decisions during market panic. They can help you stick to your long-term plan and rebalance your portfolio strategically.

Conclusion

The question “when does the stock market crash?” is one that fascinates and vexes investors, yet its precise answer remains beyond human foresight. What we can discern are the common conditions that precede a crash: speculative bubbles, restrictive monetary policies, unforeseen geopolitical shocks, and systemic financial vulnerabilities. These factors, amplified by investor psychology and market mechanics, can converge to create periods of intense market stress.

However, understanding these triggers is not about predicting the impossible, but about fostering resilience. Stock market crashes, while devastating in the short term, are an inevitable, albeit infrequent, part of the broader economic cycle. For the disciplined investor, they represent not just risks but also opportunities—chances to acquire quality assets at depressed prices. By embracing diversification, maintaining a long-term perspective, ensuring adequate liquidity, and understanding personal risk tolerance, investors can navigate these turbulent waters, emerge stronger, and ultimately continue their journey toward long-term financial prosperity. The market has always recovered, and it is the prepared, patient investor who ultimately benefits from that enduring truth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.