The moment you complete your education is often met with a mix of exhilaration and trepidation. While the achievement of a degree opens doors to new professional opportunities, it also signals the imminent arrival of a significant financial responsibility: student loan repayment. For many, understanding precisely when and how this process begins can feel like navigating a complex labyrinth. This article aims to demystify the start of student loan repayment, offering clear guidance and actionable insights to help you manage this crucial phase of your financial life.

Student loans represent a substantial investment in your future, but managing their repayment effectively is paramount to maintaining a healthy financial standing. Failing to grasp the timing and options available can lead to unnecessary stress, missed payments, and potentially adverse impacts on your credit score. By understanding the grace period, knowing your repayment plan options, and preparing proactively, you can transform a daunting obligation into a manageable step towards financial independence.

Understanding the Grace Period: Your Initial Repayment Pause

One of the most common misconceptions about student loan repayment is that payments begin immediately after graduation or leaving school. Fortunately, most student loans come with a built-in grace period, offering a temporary reprieve before your first payment is due. This period is designed to give you some breathing room to find employment, get settled, and prepare your finances.

What is a Grace Period?

A grace period is a set amount of time after you graduate, leave school, or drop below half-time enrollment during which you are not required to make payments on your student loans. For federal student loans, this period is typically six months. During this time, interest may or may not accrue depending on the type of loan you have. For instance, subsidized federal loans do not accrue interest during the grace period, while unsubsidized federal loans do. This distinction is important because any interest that accrues on unsubsidized loans during the grace period will be capitalized (added to your principal balance) when repayment officially begins, increasing the total amount you owe.

This initial pause serves as a critical window. It’s not merely a delay; it’s an opportunity to solidify your financial footing. Whether you’re searching for your first post-college job or adjusting to new living expenses, the grace period is designed to facilitate a smoother transition into full-time repayment.

Federal vs. Private Loans: Grace Period Nuances

While a six-month grace period is standard for most federal student loans (Direct Subsidized, Direct Unsubsidized, and Direct PLUS loans), the rules can differ significantly for private student loans. Private lenders set their own terms and conditions, and some may offer a grace period, while others might require payments immediately after disbursement or while you are still in school. It is crucial to check the specific terms of your private loan agreement or contact your lender directly to understand their grace period policy.

The absence or brevity of a grace period for private loans highlights the importance of thorough research and understanding of loan terms before signing. For those with a mix of federal and private loans, managing these varying timelines requires careful attention to avoid missing payments on those loans that start earlier.

Maximizing Your Grace Period

The grace period is not a time for inaction; it’s an ideal opportunity for proactive financial planning. Here’s how to make the most of it:

- Understand Your Loans: Consolidate information on all your loans – federal and private. Know your loan servicers, interest rates, principal balances, and grace period end dates.

- Create a Budget: Develop a realistic budget that accounts for your income and expenses. Identify how much you can comfortably allocate towards loan payments once they begin.

- Find a Job (If You Haven’t): Use this time to secure employment that will allow you to meet your future financial obligations.

- Make Interest-Only Payments: If you have unsubsidized loans, consider making interest-only payments during the grace period. This prevents interest from capitalizing and reduces the total cost of your loan over time.

- Explore Repayment Options: Familiarize yourself with the various repayment plans available, especially for federal loans. This preparation will help you choose the best plan when the time comes.

By using the grace period wisely, you can set yourself up for a less stressful and more financially sound repayment journey.

Official Commencement: The Day Repayment Begins

Once your grace period concludes, the official countdown to your first payment truly begins. This is the moment when your temporary reprieve ends, and your commitment to repaying your student loans becomes an active, monthly obligation. Understanding the mechanics of this commencement is vital for a smooth transition.

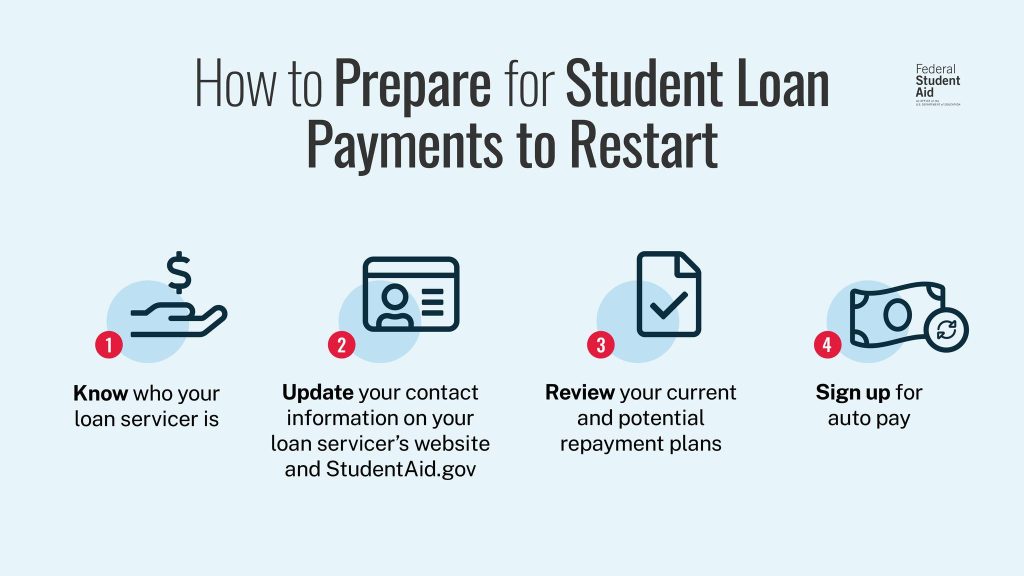

Notification and Preparation

Your loan servicer – the company that handles your loan payments – is legally required to notify you before your grace period ends and repayment begins. These notices typically include:

- Your total loan balance.

- Your interest rate.

- Your first payment due date.

- The amount of your monthly payment.

- Information about your chosen repayment plan (or the standard plan if you haven’t chosen one).

- Contact information for your servicer.

It’s imperative to keep your contact information updated with your loan servicer throughout your grace period. If you move or change your email address, inform them immediately to ensure you receive these critical notifications. Ignoring these communications can lead to missed payments and potential financial difficulties. Many servicers also offer online portals where you can track your loan details, set up payment reminders, and manage your account.

The First Payment Due Date

The first payment due date is typically set shortly after your grace period expires. For federal loans, this is usually around 30-45 days after the grace period ends. This date is not arbitrary; it’s part of a structured schedule designed to ensure consistent repayment. Mark this date on your calendar, set reminders, and make sure you have the funds available.

It’s also a good idea to confirm your payment amount and due date directly with your servicer, even if you’ve received notifications. Cross-referencing this information ensures accuracy and allows you to address any discrepancies before the due date. Proactive engagement with your servicer is a hallmark of responsible financial management.

Consequences of Missing the First Payment

Missing your very first student loan payment can have immediate and long-term repercussions:

- Late Fees: Loan servicers typically charge late fees, which can add to your total debt.

- Credit Score Impact: Payments reported 30 days or more past due can negatively affect your credit score. A lower credit score can impact your ability to secure future loans (e.g., mortgages, car loans) or even rent an apartment.

- Default Risk: Consistently missing payments can lead to default, which has severe consequences, including wage garnishment, tax refund offset, and loss of eligibility for federal student aid programs.

- Increased Stress: Financial stress can impact various aspects of your life. Avoiding the cycle of missed payments can significantly reduce this burden.

Understanding these consequences underscores the importance of being prepared and making your payments on time, starting with that very first one.

Exploring Repayment Plan Options: Tailoring Your Approach

One of the most empowering aspects of managing federal student loans is the flexibility offered through various repayment plans. These plans are designed to accommodate different financial situations, ensuring that borrowers can find a structure that works for them. For private loans, options are typically more limited, but it’s always worth contacting your lender.

Standard Repayment Plans

The Standard Repayment Plan is the default option for federal student loans if you don’t choose another plan. Under this plan, you make fixed monthly payments for up to 10 years (or up to 30 years for consolidated loans). This plan typically results in the lowest overall interest paid because you pay off your loan balance relatively quickly. It’s an excellent choice if you have a stable income and can comfortably afford the monthly payments.

Income-Driven Repayment (IDR) Plans

Income-Driven Repayment (IDR) plans are designed to make federal student loan payments more affordable by capping them at a percentage of your discretionary income. If your income is low compared to your debt, IDR plans can significantly reduce your monthly payment. After a certain period (typically 20 or 25 years, depending on the plan and whether you have graduate loans), any remaining balance may be forgiven, though the forgiven amount is usually considered taxable income.

There are several types of IDR plans:

- Revised Pay As You Earn (REPAYE): Generally 10% of discretionary income, for all Direct Loan borrowers.

- Pay As You Earn (PAYE): Generally 10% of discretionary income, but capped at the Standard Repayment Plan amount, for newer borrowers.

- Income-Based Repayment (IBR): Generally 10% or 15% of discretionary income, capped at the Standard Repayment Plan amount.

- Income-Contingent Repayment (ICR): The older IDR plan, payments are 20% of discretionary income or what you’d pay on a 12-year fixed plan, whichever is less.

IDR plans require annual recertification of your income and family size to adjust your payments. These plans are particularly beneficial for graduates entering lower-paying fields or facing temporary financial hardship.

Graduated and Extended Repayment Plans

Beyond Standard and IDR plans, federal loans offer other options:

- Graduated Repayment Plan: Payments start lower and gradually increase every two years. This plan is for borrowers whose income is expected to rise over time, but you’ll pay more interest overall than with the Standard Plan.

- Extended Repayment Plan: Allows you to extend your repayment period for up to 25 years. This results in lower monthly payments than the Standard Plan but higher overall interest costs. You must have more than $30,000 in direct loans to qualify.

Private Loan Repayment Options

For private student loans, repayment options are generally less flexible. Most private loans offer standard fixed payments or interest-only payments during school. If you face difficulty making payments, you must contact your private lender directly. They may offer forbearance or deferment options, but these are typically granted on a case-by-case basis and are not guaranteed like federal loan benefits. Some private lenders may also have options for modifying your loan terms, but these vary widely.

Strategies for a Successful Repayment Journey

Navigating student loan repayment effectively requires a proactive and strategic approach. It’s not just about making payments; it’s about optimizing your financial decisions to minimize stress and maximize your long-term financial health.

Building a Budget and Tracking Expenses

The foundation of successful student loan repayment, and indeed all personal finance, is a well-structured budget. By understanding exactly how much income you have and where every dollar goes, you can identify funds available for loan payments and make informed spending choices.

- Track Income and Outgoings: Use budgeting apps, spreadsheets, or even pen and paper to meticulously record your monthly income and all expenses.

- Identify Areas for Savings: Look for non-essential expenditures that can be cut back to free up more money for loan payments. Even small savings can add up.

- Allocate Loan Payments: Make your student loan payment a non-negotiable line item in your budget, just like rent or utilities.

A realistic budget empowers you to make timely payments without feeling deprived or constantly stressed.

Considering Refinancing or Consolidation

For some borrowers, refinancing or consolidating loans can be a powerful strategy to streamline payments or reduce interest rates.

- Consolidation (Federal): A Direct Consolidation Loan allows you to combine multiple federal student loans into a single loan with one monthly payment. This can simplify repayment and potentially open up eligibility for certain IDR plans or Public Service Loan Forgiveness (PSLF). The interest rate is a weighted average of your existing loans, rounded up to the nearest one-eighth of a percent, so it doesn’t necessarily lower your interest rate.

- Refinancing (Private): Refinancing involves taking out a new private loan to pay off one or more existing student loans (federal or private). This can be a smart move if you have excellent credit, a stable income, and can qualify for a lower interest rate, which can save you a significant amount over the life of the loan. However, be aware that refinancing federal loans into a private loan means forfeiting valuable federal benefits, such as access to IDR plans, deferment options, and potential forgiveness programs. This decision should be made carefully, weighing the potential interest savings against the loss of federal protections.

Automating Payments and Avoiding Penalties

Automation is your ally in student loan repayment. Setting up automatic payments directly from your bank account ensures that you never miss a due date. Most loan servicers offer a small interest rate reduction (typically 0.25%) for enrolling in auto-pay, which can further save you money.

- Set It and Forget It: Once set up, auto-pay provides peace of mind that your payments are always made on time.

- Avoid Late Fees and Credit Dings: Automated payments eliminate the risk of late fees and negative marks on your credit report due to forgetfulness.

- Potential Interest Rate Discount: Take advantage of any auto-pay discounts offered by your servicer.

Even with automation, it’s wise to periodically check your account to ensure payments are processing correctly and that you have sufficient funds available.

What to Do If You Face Financial Hardship

Life is unpredictable, and sometimes even the best-laid financial plans go awry. If you find yourself struggling to make your student loan payments, it’s crucial to act quickly and communicate with your servicer.

For federal loans, you have several options:

- Income-Driven Repayment (IDR) Plans: If you’re not already on one, switching to an IDR plan can significantly lower your monthly payments based on your current income.

- Deferment: Allows you to temporarily postpone your payments for specific situations like unemployment, economic hardship, or military service. Interest may or may not accrue during deferment, depending on the loan type.

- Forbearance: Also allows you to temporarily stop or reduce payments. Interest typically accrues on all loan types during forbearance. It’s often granted for a maximum of 12 months at a time.

For private loans, immediately contact your lender to discuss your options. They may offer limited forbearance, modified payment plans, or other assistance, but it’s not guaranteed. The key is never to ignore the problem; proactive communication is your best defense against default.

The Long-Term Impact of Student Loan Repayment

While the immediate concern is making monthly payments, understanding the long-term implications of student loan repayment on your overall financial landscape is equally important. Your repayment journey isn’t just about debt; it’s about building financial habits and achieving future goals.

Credit Score Implications

Your student loan repayment history plays a significant role in shaping your credit score.

- Positive Impact: Consistent, on-time payments demonstrate financial responsibility and build a strong credit history, which is essential for qualifying for mortgages, car loans, and credit cards at favorable interest rates.

- Negative Impact: Missed or late payments, particularly those reported to credit bureaus (typically 30 days or more past due), can severely damage your credit score, making it harder and more expensive to borrow money in the future. Defaulting on student loans has even more severe and long-lasting negative effects.

Financial Freedom and Future Goals

Successfully managing your student loans frees up financial capacity for other life goals. Paying down your debt allows you to:

- Save for a Down Payment: Whether for a home or another significant purchase, reducing student loan payments gives you more disposable income to put towards savings.

- Invest for Retirement: The sooner you start investing, the more time your money has to grow through compounding. Less student loan debt means more capacity for retirement contributions.

- Build an Emergency Fund: A robust emergency fund provides a safety net against unexpected expenses, reducing reliance on credit cards or further loans.

- Pursue Entrepreneurship: Having less debt can give you the financial flexibility and courage to take calculated risks, such as starting your own business.

The Psychological Aspect

Beyond the numbers, the psychological weight of student loan debt can be substantial. The journey from initial anxiety to eventual liberation can be a rollercoaster.

- Stress and Anxiety: The burden of debt can lead to significant stress, impacting mental well-being and overall quality of life.

- Motivation and Discipline: Successfully repaying loans can foster strong financial discipline and a sense of accomplishment.

- Relief and Empowerment: The ultimate payoff—becoming debt-free—brings immense relief and a powerful sense of financial empowerment, opening up new possibilities for your future.

Understanding when student loan repayment starts, exploring your options, and developing a strategic approach are crucial steps on the path to financial wellness. By being informed and proactive, you can navigate this challenge successfully and lay a strong foundation for a secure and prosperous future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.