Navigating the complexities of tax season is a fundamental pillar of personal finance management. For many, the question “When can I file my taxes?” is the starting gun for a sprint toward a potential refund or the finalization of a yearly budget. However, filing taxes is not merely an administrative hurdle; it is a strategic financial event that requires an understanding of IRS timelines, documentation cycles, and the broader implications for your financial health. Whether you are an employee with a single W-2, a freelancer navigating the gig economy, or a small business owner, understanding the “when” and “how” of tax filing is essential for optimizing your cash flow and maintaining compliance.

Understanding the IRS Tax Calendar and Key Deadlines

The timing of your tax filing is primarily dictated by the Internal Revenue Service (IRS), which sets the official “opening” of the tax season each year. Typically, the IRS begins accepting and processing individual tax returns in late January. While you may be able to prepare your return earlier using various software platforms, the IRS will not officially pull those returns into their system until the designated start date.

The Official Tax Season Launch

The tax season usually kicks off between January 24th and January 31st. The exact date is announced by the IRS in early January, following their internal systems updates and adjustments for any last-minute legislative changes. For taxpayers, this date represents the earliest moment a refund can begin processing. If you are a practitioner of proactive personal finance, aiming for this window is often beneficial, as early filers typically receive their refunds significantly faster than those who wait until the April rush.

The April Deadline and Its Variations

The traditional deadline for filing federal income tax returns is April 15th. However, this date is subject to change based on weekends and legal holidays. For instance, if April 15th falls on a Saturday or Sunday, the deadline moves to the following Monday. Additionally, Emancipation Day—a holiday observed in Washington, D.C.—can push the deadline back. Understanding these nuances is critical for avoiding late-filing penalties, which can accrue at a rate of 5% of the unpaid taxes for each month or part of a month that a return is late.

Deadlines for Business Owners and Freelancers

If you operate as a business owner or a freelancer, your “when” might be different. For example, S-Corporations and Partnerships (Form 1065 and 1120-S) typically have a filing deadline of March 15th. Furthermore, those who pay estimated quarterly taxes must adhere to a different rhythm altogether, with payments due in April, June, September, and January. Aligning your personal filing with these business obligations is a core component of sophisticated business finance management.

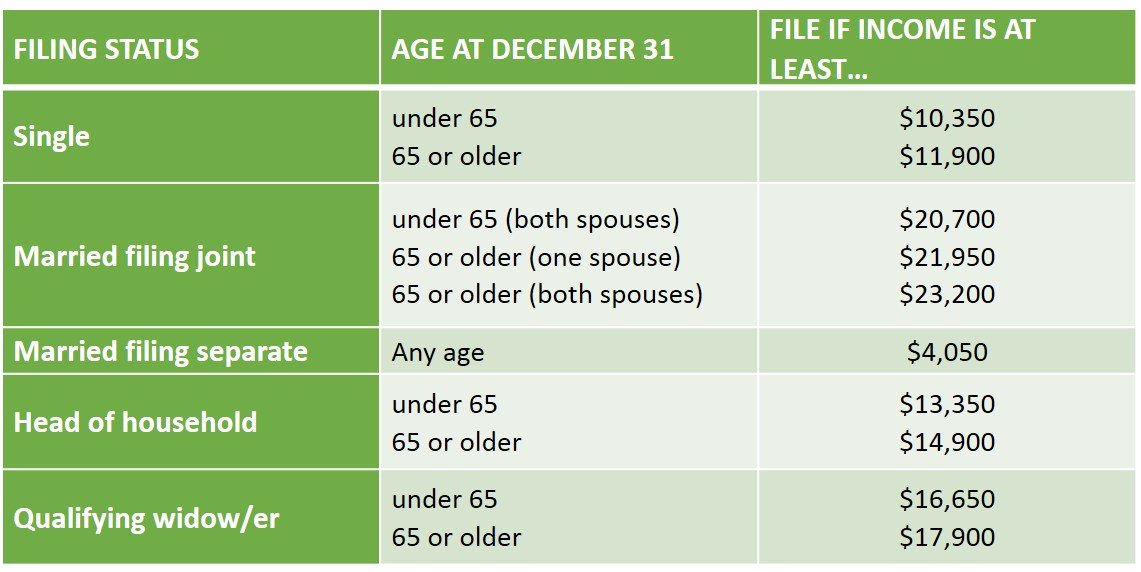

Essential Documentation: What You Need Before You File

You cannot file your taxes until you have a complete picture of your annual financial activity. The “when” of filing is often limited by when your employers, banks, and brokerage firms send out your necessary tax forms. Most institutions are required by law to mail or provide digital access to these forms by January 31st.

Income Statements: W-2s, 1099s, and Beyond

The backbone of your tax return is your income documentation. Full-time employees look for their W-2, while independent contractors and freelancers must wait for various 1099 forms (specifically the 1099-NEC). In the modern era of “online income,” you must also look for 1099-K forms if you have received significant payments through third-party processors. Filing before these forms arrive is a recipe for an amended return, which adds unnecessary complexity and potential interest charges to your financial life.

Investment and Interest Records

For those focused on investing and wealth building, 1099-B (for brokerage transactions), 1099-DIV (for dividends), and 1099-INT (for interest income) are vital. It is worth noting that some brokerage firms issue “consolidated” tax statements, which may not arrive until mid-to-late February. If you are an active investor, your filing window is naturally pushed back by this delay in reporting from financial institutions.

Deductions and Credit Substantiation

To minimize your tax liability and maximize your net worth, you must gather documentation for deductions. This includes 1098 forms for mortgage interest, records of charitable contributions, and receipts for business expenses if you are self-employed. If you are claiming the Earned Income Tax Credit (EITC) or the Additional Child Tax Credit (ACTC), the IRS is required by the PATH Act to hold your refund until mid-February, regardless of how early you file. This is an important financial planning detail for households relying on those funds for early-year expenses.

Strategic Financial Benefits of Timely Filing

Filing your taxes is not just about meeting a legal obligation; it is a tool for financial protection and optimization. There are several strategic reasons why filing as soon as you have your documentation is a superior financial move.

Mitigating the Risk of Identity Theft

Tax-related identity theft occurs when a fraudster uses your Social Security number to file a phony return and claim a fraudulent refund. By filing early, you effectively “lock” your Social Security number for the year. If a criminal attempts to file in your name after the IRS has already accepted your legitimate return, their fraudulent attempt will be automatically rejected. This is one of the simplest and most effective digital security measures you can take for your personal finances.

Accelerated Refund Management and Cash Flow

If you are owed a refund, the sooner you file, the sooner that capital returns to your control. From a personal finance perspective, a tax refund is essentially an interest-free loan you have given to the government. Once returned, these funds can be deployed into high-yield savings accounts, used to pay down high-interest debt, or invested in the market. Waiting until April to file means you are losing out on months of potential interest or the “time value of money.”

Financial Planning and Debt Strategy

Conversely, if you discover that you owe money, filing early gives you more time to arrange for payment. You can file your return in February to find out exactly what you owe, but you are not required to actually send the payment until the April deadline. This provides a two-month window to adjust your budget, liquidate assets if necessary, or set aside funds from your current income to cover the liability without incurring late-payment interest.

Leveraging Tools and Professional Advice

The methodology you choose for filing—whether it’s DIY software or a professional accountant—significantly impacts your filing experience and your financial outcomes.

Choosing Between Software and a CPA

For individuals with straightforward income (a single W-2 and standard deduction), modern tax software provides a cost-effective and efficient way to file as soon as the IRS opens. These tools are designed to guide users through the “Money” aspects of their lives with simple questions. However, as your financial portfolio grows—including rental properties, stock options, or business ownership—the value of a Certified Public Accountant (CPA) increases. A professional can provide tax planning advice that goes beyond mere filing, helping you structure your finances to minimize future tax bites.

Free File and VITA Programs

The IRS offers the “Free File” program for taxpayers whose adjusted gross income falls below a certain threshold. This provides access to high-quality tax preparation software at no cost. Additionally, the Volunteer Income Tax Assistance (VITA) program offers free tax help to people who generally make $64,000 or less, persons with disabilities, and limited English-speaking taxpayers. Utilizing these programs ensures that the cost of filing does not eat into your hard-earned savings.

Understanding Tax Extensions

If you cannot file by the April deadline, you can request an automatic six-month extension, moving your filing deadline to October 15th. It is a common financial misconception that an extension gives you more time to pay. In reality, an extension only gives you more time to file the paperwork. You must still estimate and pay your expected tax liability by the April deadline to avoid interest and failure-to-pay penalties. For those with complex international investments or K-1 forms from partnerships that often arrive late, the extension is a vital tool for ensuring accuracy.

Conclusion: The Lifecycle of a Tax Return

Knowing when you can file your taxes is the first step in a larger cycle of financial responsibility. By marking your calendar for the late-January IRS opening, ensuring your 1099s and W-2s are organized by early February, and understanding the specific deadlines for your business or investment types, you position yourself for financial success.

Filing taxes shouldn’t be a period of stress; instead, it should be viewed as an annual audit of your financial health. It is the moment when you reconcile your earnings, evaluate your investments, and reset your strategies for the year ahead. By being proactive rather than reactive, you protect your identity, optimize your cash flow, and ensure that you are making the most of every dollar you earn. Whether you file on day one or take advantage of an extension to ensure precision, the key is to approach the tax season with a clear, money-focused strategy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.