In an increasingly digital world, the way we manage and transfer money has undergone a profound transformation. At the forefront of this revolution stands Venmo, a ubiquitous name in peer-to-peer (P2P) payment solutions. More than just an application, Venmo represents a significant shift in how individuals interact with their finances, blending convenience with social connectivity. For many, especially younger demographics, “Venmo me” has become synonymous with settling debts, splitting bills, or sending money to friends and family. But beyond its widespread adoption and catchy colloquialisms, what exactly is Venmo? This article will dissect Venmo from a technological perspective, exploring its core functionality, design principles, impact on the digital payment landscape, and the underlying innovations that power its operations.

The Technological Core: How Venmo Works

At its heart, Venmo is a mobile payment service owned by PayPal, designed to simplify the process of sending and receiving money between individuals. It operates primarily through a smartphone application, leveraging a sophisticated backend infrastructure to facilitate instant, secure transactions. Understanding Venmo means understanding the technology that makes these seamless exchanges possible.

The Underlying Architecture: Facilitating Instant Transfers

When a user initiates a payment on Venmo, the process kicks off a series of complex interactions behind the scenes. Initially, the app communicates with Venmo’s servers, which verify the sender’s identity and account balance (or linked funding source). The system then processes the request, debiting the sender’s account and crediting the recipient’s Venmo balance. While the transaction appears instantaneous to the end-user, it involves robust real-time data processing and synchronization across distributed systems.

The ‘instant’ nature of Venmo payments often refers to the immediate update of the recipient’s Venmo balance. Actual funds transfer to an external bank account, known as “cashing out,” can take standard banking days (typically 1-3 business days) for free transfers, or minutes for a small fee using the “Instant Transfer” feature. This distinction is crucial and highlights the sophisticated balance Venmo strikes between user experience and the realities of traditional banking rails. The technology behind Instant Transfer involves direct partnerships with banking networks and advanced fraud detection algorithms that allow for near real-time settlement, albeit at a premium.

Security Protocols: Protecting User Data and Transactions

Given the sensitive nature of financial transactions, security is paramount for Venmo. The platform employs a multi-layered security architecture to protect user data and prevent unauthorized access or fraudulent activity. This includes:

- Encryption: All data transmitted between the user’s device and Venmo’s servers is encrypted using industry-standard protocols (e.g., TLS/SSL). This ensures that personal and financial information remains confidential and impervious to eavesdropping.

- Authentication: Users are required to authenticate their identity using strong passwords, PINs, or biometric methods (fingerprint, facial recognition). Two-factor authentication (2FA) is also available, adding an extra layer of security by requiring a verification code sent to a trusted device.

- Fraud Detection Systems: Venmo utilizes advanced machine learning algorithms to continuously monitor transactions for suspicious patterns indicative of fraud. These systems analyze a vast array of data points in real-time to identify and flag potentially fraudulent activities, triggering alerts or automatic transaction blocks.

- PCI DSS Compliance: As a payment processor, Venmo adheres to the Payment Card Industry Data Security Standard (PCI DSS), a set of security standards designed to ensure that all companies that process, store, or transmit credit card information maintain a secure environment.

While Venmo implements robust security measures, it also educates users on best practices, such as being cautious of phishing scams and only sending money to trusted individuals, underscoring the shared responsibility in maintaining digital financial security.

Integration with Banking Systems and Payment Networks

Venmo’s functionality is deeply intertwined with the broader financial ecosystem. It integrates seamlessly with users’ existing bank accounts, debit cards, and credit cards. This integration is achieved through secure API (Application Programming Interface) connections with financial institutions and major payment networks (Visa, Mastercard, American Express, Discover). When a user links a bank account or card, Venmo uses these APIs to verify account ownership and facilitate the movement of funds, both for adding money to their Venmo balance and for cashing out. The ability to abstract away the complexities of these underlying financial rails into a simple, user-friendly interface is a testament to Venmo’s engineering prowess.

User Experience and Interface Design: The App’s Appeal

Beyond the robust backend technology, a significant part of Venmo’s success lies in its front-end design and user experience. The app is crafted to be intuitive, engaging, and remarkably easy to use, making financial interactions feel less like a chore and more like a natural part of digital communication.

Intuitive Design: Navigating the Venmo Ecosystem

Venmo’s user interface (UI) is characterized by its clean, minimalist design and straightforward navigation. Key functionalities—sending/requesting money, viewing transaction history, and managing settings—are prominently accessible, minimizing the learning curve for new users. The design prioritizes clarity and efficiency, ensuring that users can complete tasks quickly and without confusion. This focus on user-centric design is critical for any technology dealing with personal finance, as trust and ease of use directly impact adoption and retention. The use of clear icons, readable fonts, and logical information hierarchy contributes to an overall positive and stress-free user experience.

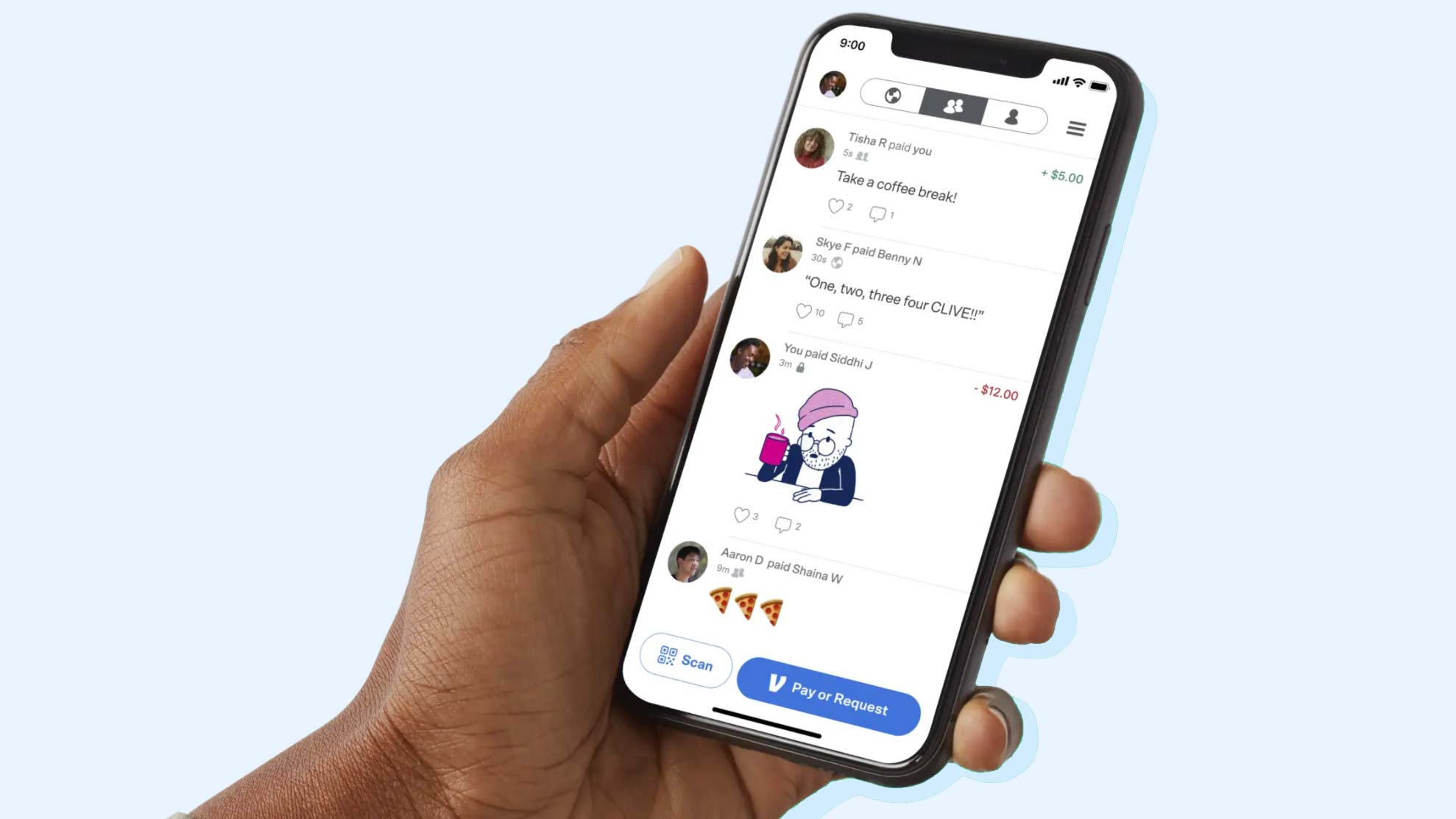

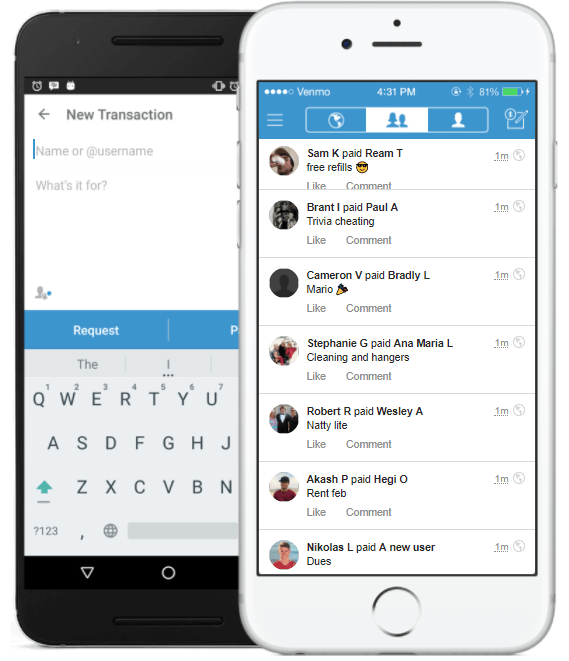

Social Features: Payments as a Shared Experience

One of Venmo’s most distinctive features, and a significant contributor to its viral growth, is its integrated social feed. Each transaction, by default, is shared on a public, friends-only, or private feed, often accompanied by emojis, brief descriptions, and likes/comments. While optional, this social layer transforms what would otherwise be a mundane financial transaction into an interactive, almost game-like experience. From a technological standpoint, integrating this social graph into a payment application required careful consideration of privacy settings, data management, and real-time feed updates without compromising transaction security or performance. This novel approach positioned Venmo not just as a financial tool but also as a social platform, leveraging network effects to drive user engagement.

Beyond P2P: Expanding Services and Features

While its core remains P2P payments, Venmo has continually evolved its feature set, leveraging its established user base and technological infrastructure to expand into broader financial services. These expansions are all rooted in building new technological capabilities into the existing platform:

- Business Profiles: Venmo introduced business profiles, allowing small businesses and freelancers to accept payments from customers directly through the app, complete with QR codes for in-person transactions. This required developing new merchant tools, transaction reporting, and compliance features.

- Venmo Debit and Credit Cards: Partnering with financial institutions, Venmo offers physical and virtual debit and credit cards, which draw directly from or link to a user’s Venmo balance. This involved deep integration with payment network infrastructure and sophisticated card management systems within the app.

- Direct Deposit: Users can set up direct deposit for their paychecks directly into their Venmo account, effectively positioning Venmo as a primary banking alternative for some. This required integrating with ACH (Automated Clearing House) networks and developing compliant banking features.

- Cryptocurrency Trading: More recently, Venmo has ventured into cryptocurrency, allowing users to buy, hold, and sell selected cryptocurrencies directly within the app. This necessitated building a secure crypto wallet infrastructure, integrating with crypto exchanges, and navigating the complexities of blockchain technology. Each of these expansions demonstrates Venmo’s commitment to evolving its technological offerings beyond simple money transfers, aiming to become a more comprehensive digital wallet solution.

Venmo’s Evolution and Impact on Digital Payments

Venmo didn’t just appear; it evolved, adapting to technological advancements and user demands. Its journey from a niche startup to a mainstream payment giant has left an indelible mark on how we perceive and conduct digital transactions.

From Niche Tool to Mainstream Staple: Growth Trajectory

Initially launched in 2009, Venmo began as a text message-based payment system, quickly pivoting to a smartphone app to capitalize on the burgeoning mobile revolution. Its acquisition by Braintree in 2012, and subsequently by PayPal in 2013, provided the necessary resources and infrastructure to scale rapidly. PayPal’s backing significantly bolstered Venmo’s technological capabilities, security, and market reach. This strategic integration allowed Venmo to leverage PayPal’s extensive financial network and regulatory expertise while retaining its distinct, youth-oriented brand and social features. The growth trajectory underscores the importance of robust technological infrastructure and strategic partnerships in scaling a digital product.

Disrupting Traditional Banking: A New Paradigm for Transfers

Venmo, along with other P2P apps, fundamentally disrupted the traditional model of transferring money. Prior to these apps, splitting a dinner bill often meant fumbling with cash, waiting for checks to clear, or dealing with cumbersome bank transfers. Venmo simplified this, offering a frictionless, instant, and often free alternative. This ease of use has shifted consumer expectations, putting pressure on traditional banks to innovate their own digital offerings. Venmo demonstrated that financial transactions could be quick, mobile-first, and even enjoyable, setting a new benchmark for digital payment solutions. The technology enabled a direct, human-centric approach to finance, bypassing traditional intermediaries with their slower processes.

Challenges and Competitors in the Digital Wallet Landscape

Despite its success, Venmo operates in a highly competitive and evolving landscape. Competitors include:

- Zelle: A bank-backed P2P network offering direct transfers between bank accounts, often integrated into banking apps. Zelle focuses purely on the financial transaction, lacking Venmo’s social features.

- Cash App: From Square (now Block), Cash App offers P2P payments, investing in stocks and Bitcoin, and debit card services, often with a younger, edgier brand identity.

- Apple Pay Cash and Google Pay: These tech giants integrate P2P functionality directly into their mobile operating systems, leveraging their vast user bases and ecosystem lock-in.

- PayPal: Venmo’s parent company, PayPal, also offers P2P services, often catering to a slightly older or more business-oriented demographic.

The constant innovation from these competitors necessitates Venmo to continuously enhance its technology, adding new features, bolstering security, and optimizing performance to maintain its market position. The challenge is not just to attract new users but to retain existing ones by offering a superior and evolving technological experience.

Understanding Venmo’s Technology Stack and Future Innovations

Delving deeper into Venmo’s technical foundation reveals a sophisticated blend of modern technologies and architectural patterns designed for scalability, reliability, and continuous innovation.

Leveraging Cloud Infrastructure for Scalability

Venmo, like many modern digital services, heavily relies on cloud computing infrastructure. This allows the platform to dynamically scale its resources up or down based on user demand, ensuring optimal performance even during peak usage times (e.g., Friday evenings when people often split dinner bills). Utilizing cloud services provides high availability, disaster recovery capabilities, and the flexibility to deploy new features rapidly. This move away from proprietary on-premise servers is a cornerstone of modern digital service delivery, enabling Venmo to handle millions of transactions daily without significant downtime.

API Integrations and Developer Ecosystem

The ability for Venmo to integrate with various external services – from linking bank accounts to supporting merchant payments – speaks to its robust API (Application Programming Interface) strategy. A well-designed set of APIs allows different software systems to communicate and exchange data securely and efficiently. While Venmo doesn’t have a broad public developer ecosystem like some larger platforms, its internal use of APIs for feature development and external integrations (e.g., with specific merchant partners or financial institutions) is fundamental. These APIs are the connective tissue that allows Venmo to extend its functionality beyond the core app, enabling features like in-app purchases or payments through other applications.

Emerging Technologies: AI, Blockchain, and the Road Ahead for P2P

The future of P2P payments will undoubtedly be shaped by emerging technologies, and Venmo is well-positioned to integrate these innovations.

- Artificial Intelligence (AI) and Machine Learning (ML): Beyond fraud detection, AI/ML can enhance user experience through personalized insights, smart expense categorization, and predictive analytics for spending habits. Chatbot integration for customer support, powered by natural language processing (NLP), could also streamline user interactions.

- Blockchain and Decentralized Finance (DeFi): Venmo’s foray into cryptocurrency is an early step into the blockchain space. While not fully decentralized, exploring blockchain technology for cross-border payments could reduce costs and increase transfer speeds. Secure identity management using blockchain could also enhance privacy and security features.

- Voice Commerce and IoT Payments: As smart home devices and the Internet of Things (IoT) become more prevalent, voice-activated payments (e.g., “Alexa, Venmo Sarah for dinner”) and embedded payment capabilities in devices could become the next frontier. This requires seamless integration with diverse hardware and robust security protocols for non-traditional payment interfaces.

Venmo’s continuous investment in technology ensures it remains at the forefront of these innovations, ready to adapt and integrate new paradigms into its service offering.

Best Practices for Secure and Efficient Venmo Usage

While Venmo’s technology is designed to be secure and efficient, user behavior plays a crucial role in maximizing its benefits and minimizing risks.

Safeguarding Your Account: Tips for Digital Security

Users are the first line of defense in digital security. To protect your Venmo account:

- Use Strong, Unique Passwords: Avoid easily guessable passwords and never reuse passwords across multiple services.

- Enable Two-Factor Authentication (2FA): This critical security feature adds an extra layer of protection by requiring a code from your phone in addition to your password.

- Monitor Your Activity: Regularly review your transaction history for any unauthorized payments.

- Be Wary of Phishing Scams: Do not click on suspicious links in emails or texts purporting to be from Venmo. Always go directly to the official app or website. Venmo will never ask for your password or PIN via email or text.

- Only Send Money to Trusted Individuals: Once money is sent on Venmo, it can be difficult to recover, especially if sent to a scammer. Verify the recipient’s identity and username carefully.

- Secure Your Device: Use passcodes, biometrics, and up-to-date operating systems on your smartphone to protect against unauthorized access to your device and, by extension, your Venmo app.

Troubleshooting Common Technical Issues

Even with sophisticated technology, users might occasionally encounter technical glitches. Venmo provides robust support channels for these situations:

- App Updates: Ensure your Venmo app is always updated to the latest version, as updates often include bug fixes and security enhancements.

- Internet Connection: A stable internet connection (Wi-Fi or mobile data) is essential for the app to function correctly.

- Linked Accounts: Verify that your bank accounts or cards are correctly linked and have not expired.

- Contact Support: For persistent issues, Venmo’s in-app help center and customer support team are available to diagnose and resolve technical problems.

Privacy Settings and Managing Your Digital Footprint

Venmo’s social features, while engaging, require users to be mindful of their privacy settings. The app offers granular controls over who can see your transactions (public, friends-only, or private). Users should periodically review these settings to ensure they align with their comfort level regarding their financial privacy. Understanding how your data is used and shared, and actively managing your digital footprint, is an important aspect of responsible technology usage in the age of interconnected apps.

In conclusion, Venmo is far more than just a simple money-sending app; it’s a testament to the power of well-engineered technology to transform everyday financial interactions. By combining robust security protocols, an intuitive user interface, and innovative social features with continuous technological evolution, Venmo has cemented its place as a cornerstone of the modern digital payment landscape, defining what it means to send and receive money in the 21st century.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.