Navigating the landscape of retirement savings can often feel like deciphering a complex code. While the 401(k) is a household name, many individuals, particularly those in public service or certain non-profit sectors, may encounter another, equally significant, yet less widely discussed, retirement savings vehicle: the 401(a). Understanding the nuances of a 401(a) plan is crucial for maximizing your long-term financial security and making informed decisions about your future. This article delves into the core aspects of the 401(a) plan, exploring its purpose, key features, how it compares to other retirement options, and what you need to know to make it work for you.

The Foundation of the 401(a): Purpose and Eligibility

The 401(a) retirement plan, much like its more famous counterpart, is designed to help employees save for retirement on a tax-advantaged basis. Its primary objective is to provide a reliable stream of income after an individual ceases to be employed, thereby ensuring financial stability during their post-working years.

Origins and Target Audience

The 401(a) plan is established under Section 401(a) of the Internal Revenue Code, which is the same section that governs 401(k) plans. However, the application and eligibility for 401(a) plans differ significantly. Historically, 401(a) plans were predominantly offered to employees of state and local governments, public school systems, and certain tax-exempt organizations. This includes a wide array of professionals such as teachers, police officers, firefighters, and university staff. The rationale behind offering these plans to public sector employees is often to provide a competitive benefits package that attracts and retains valuable talent in roles that may not always offer the same salary potential as the private sector.

Distinguishing Features of Eligibility

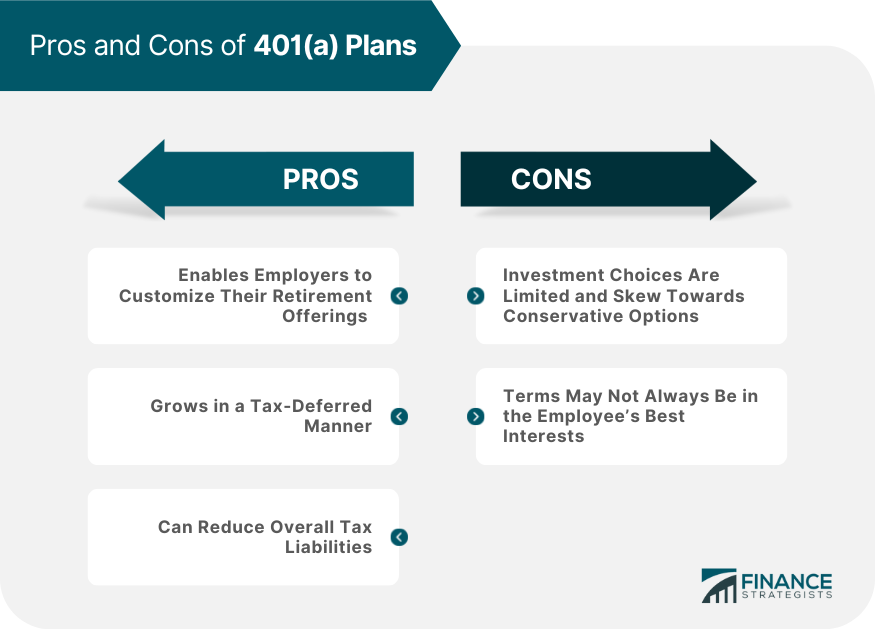

Unlike 401(k) plans, which are commonly available in the private sector, 401(a) plans are not typically offered by for-profit companies. The eligibility for a 401(a) is determined by the employer, and it is intrinsically linked to the nature of the organization. For instance, a state university will likely offer a 401(a) to its faculty and administrative staff, while a private corporation will likely offer a 401(k) or a defined benefit pension plan. It’s important to note that within eligible organizations, there may be specific criteria for participation, such as a waiting period after employment commencement or a minimum number of hours worked per year. Understanding these specific eligibility requirements is the first step to leveraging the benefits of a 401(a) plan.

Key Characteristics of the 401(a) Plan

While sharing the fundamental goal of retirement savings with other employer-sponsored plans, the 401(a) possesses several distinct characteristics that shape its structure and operation. These features can impact contribution methods, investment choices, and distribution rules, making it essential to grasp them thoroughly.

Contribution Structures: Employer and Employee Roles

A defining aspect of many 401(a) plans is the contribution structure. While employee contributions are common, employer contributions are also a significant feature and, in some cases, are mandatory.

Mandatory Employer Contributions

Many 401(a) plans feature mandatory employer contributions. This means the employer is legally obligated to contribute a certain percentage of the employee’s salary into the retirement account, regardless of whether the employee chooses to contribute. This can be a powerful benefit, as it guarantees a baseline level of retirement savings growth, effectively acting as a form of deferred compensation. The specific percentage is determined by the plan rules, which are often set by state law or the governing body of the organization.

Employee Contributions: Voluntary and Mandatory Options

Employees often have the option to make their own contributions to a 401(a) plan. These contributions are typically made on a pre-tax basis, meaning they reduce your current taxable income, leading to immediate tax savings. In some 401(a) plans, employee contributions might also be mandatory, either as a percentage of salary or a fixed amount, particularly if the employer contributions are designed to be supplementary. The ability to contribute not only accelerates your savings but also allows you to take advantage of potential employer matches, where the employer contributes a certain amount for every dollar the employee contributes, up to a specified limit. This matching feature is a significant incentive for employees to actively participate and maximize their savings.

Investment Options and Growth Potential

Once contributions are made, they are typically invested to grow over time. The investment landscape within a 401(a) plan, while varying by plan provider, generally offers a range of options designed to meet different risk tolerances and financial goals.

Diversified Investment Portfolios

Participants in a 401(a) plan usually have access to a curated selection of investment vehicles. These commonly include a variety of mutual funds, such as stock funds (covering domestic and international equities), bond funds (ranging from government bonds to corporate bonds), and balanced funds (which combine stocks and bonds). Some plans may also offer target-date funds, which automatically adjust their asset allocation to become more conservative as the participant approaches retirement. The goal of these diversified options is to allow participants to construct a portfolio that aligns with their time horizon to retirement and their comfort level with market fluctuations.

Tax-Deferred Growth and Compounding

The primary advantage of investing within a 401(a) plan is the tax-deferred growth. This means that any earnings, dividends, or capital gains generated by your investments are not taxed until you withdraw them in retirement. This deferral allows your investments to compound more effectively, as your earnings are reinvested and subsequently generate their own earnings, creating a snowball effect over time. The longer your money remains invested, the greater the impact of compounding, making consistent contributions and strategic investment choices paramount to maximizing long-term wealth accumulation.

Comparing the 401(a) to Other Retirement Plans

To fully appreciate the 401(a) plan, it’s beneficial to compare it to other common retirement savings vehicles, particularly the ubiquitous 401(k) and traditional pension plans. Understanding these distinctions helps individuals make informed decisions and maximize their retirement readiness.

The 401(a) vs. the 401(k): Similarities and Differences

Both the 401(a) and the 401(k) are defined contribution plans operating under Section 401(a) of the Internal Revenue Code. This shared foundation means they share many fundamental characteristics, including:

- Tax Advantages: Contributions are typically made pre-tax, reducing current taxable income, and earnings grow tax-deferred until withdrawal.

- Contribution Limits: Both plans have annual contribution limits set by the IRS, which are subject to change.

- Portability: While not always fully portable, many 401(a) and 401(k) plans allow for rollovers to other retirement accounts upon separation from service.

- Investment Options: Both offer a range of investment choices, typically mutual funds.

However, crucial differences exist:

- Eligibility and Employer Type: As discussed, 401(a) plans are primarily for public sector and certain non-profit employees, while 401(k)s are prevalent in the private sector.

- Mandatory Employer Contributions: 401(a) plans are more likely to feature mandatory employer contributions, sometimes even without employee contributions. While some 401(k)s offer employer matches, mandatory employer contributions are less common.

- Plan Design Flexibility: 401(a) plans can sometimes have more unique or employer-specific designs, whereas 401(k) plans tend to follow more standardized structures due to their widespread adoption across industries.

401(a) and Defined Benefit Pension Plans: A Divergent Path

Defined benefit (DB) pension plans, often referred to as traditional pensions, represent a different model of retirement income. In a DB plan, retirement income is calculated based on a formula that typically considers factors like salary history, years of service, and age at retirement.

- Guaranteed Income: The key distinction is that DB plans promise a specific, predictable monthly income in retirement, often for life. This provides a high degree of certainty about retirement income.

- Employer Responsibility: The investment risk and responsibility for ensuring sufficient funds for promised benefits lie primarily with the employer.

- Defined Contribution vs. Defined Benefit: In contrast, a 401(a) is a defined contribution plan. The amount of retirement income is not guaranteed; it depends entirely on the total contributions made by the employer and employee, and the investment performance of those contributions.

- Shift in Responsibility: The shift from DB plans to defined contribution plans (like 401(a)s and 401(k)s) over the past few decades has transferred more of the retirement savings responsibility and investment risk from employers to employees.

Understanding these comparisons is vital for individuals to accurately assess their retirement planning strategy and to recognize the specific advantages and responsibilities associated with their 401(a) plan.

Maximizing Your 401(a) for a Secure Retirement

Enrolling in a 401(a) plan is a significant step towards financial well-being in retirement. However, simply participating is not enough; active engagement and strategic planning are key to truly maximizing its potential.

Understanding Your Plan’s Specifics

The first and most critical step is to thoroughly understand the details of your specific 401(a) plan. This involves:

- Reviewing Plan Documents: Obtain and carefully read the Summary Plan Description (SPD). This document outlines your plan’s rules, eligibility requirements, contribution details, vesting schedules, and investment options.

- Identifying Contribution Rules: Understand if your contributions are voluntary or mandatory, and if there are any employer matching contributions. If a match is offered, aim to contribute enough to receive the full benefit, as it’s essentially “free money” that significantly boosts your savings.

- Knowing Vesting Schedules: Vesting refers to the employee’s ownership of employer contributions. Understand how long you need to be employed to become fully vested in any employer contributions. Once vested, those funds are yours to keep, even if you leave the employer.

Strategic Investment and Contribution Choices

Once you have a grasp of your plan’s framework, you can make more informed decisions about your contributions and investments.

Contribution Levels and Employer Match

- Contribute at Least to the Match: If your plan offers an employer match, contribute at least enough to capture the full match. This is one of the most effective ways to increase your retirement savings.

- Increase Contributions Over Time: As your income grows, try to increase your contribution percentage. Even small incremental increases can make a substantial difference over decades. Consider increasing contributions when you receive pay raises.

- Consider Catch-Up Contributions: If you are aged 50 or older, you may be eligible to make additional “catch-up” contributions beyond the standard annual limit, allowing you to boost your savings in your later working years.

Investment Allocation and Risk Management

- Assess Your Risk Tolerance: Evaluate how comfortable you are with investment risk. Younger individuals with a longer time horizon can typically afford to take on more risk for potentially higher returns, while those closer to retirement may opt for more conservative investments.

- Diversify Your Portfolio: Don’t put all your eggs in one basket. Spread your investments across different asset classes (stocks, bonds, etc.) to mitigate risk.

- Consider Target-Date Funds: For a hands-off approach, target-date funds automatically adjust their asset allocation to become more conservative as you near your target retirement date, simplifying the investment process.

- Regularly Review and Rebalance: Periodically review your investment performance (at least annually) and rebalance your portfolio if necessary to ensure it still aligns with your goals and risk tolerance.

Planning for Distributions and Beyond

Retirement planning doesn’t end with contributions; it extends to how you will access those funds.

Understanding Withdrawal Rules and Taxes

- Early Withdrawal Penalties: Be aware of the penalties associated with withdrawing funds before retirement age (typically 59½). These usually involve a 10% IRS penalty in addition to ordinary income taxes.

- Required Minimum Distributions (RMDs): Once you reach a certain age (currently 73, rising to 75), you will be required to take minimum distributions from your 401(a) account annually, and these distributions will be taxed as ordinary income.

- Tax Implications: Understand the tax implications of withdrawals in retirement. Since contributions are typically pre-tax, withdrawals will be taxed as ordinary income.

Considering Rollover Options

- Rolling Over to an IRA: When you leave an employer, you have the option to roll over your 401(a) funds into an Individual Retirement Account (IRA). This can offer more investment flexibility and control.

- Rolling Over to a New Employer’s Plan: If your new employer offers a retirement plan, you may be able to roll your 401(a) funds into that plan, consolidating your retirement assets.

By actively engaging with your 401(a) plan, understanding its unique features, and making strategic choices regarding contributions and investments, you can significantly enhance your prospects for a financially secure and comfortable retirement. The 401(a) is a powerful tool, and with informed participation, it can be a cornerstone of your long-term financial success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.