The concept of poverty, while seemingly straightforward on the surface, is a multifaceted economic and social construct that extends far beyond a simple numerical threshold. When we ask “what yearly income is considered poverty?”, we are delving into a complex interplay of official definitions, cost of living realities, and the lived experiences of millions. Understanding the official poverty lines, their evolution, and their limitations is crucial for comprehending the financial struggles faced by individuals and families, as well as for informing effective policy interventions. This article will explore the various dimensions of poverty measurement, dissecting the metrics, examining their shortcomings, and highlighting the broader implications for personal finance and societal well-being.

Defining Poverty: More Than Just a Number

Poverty is often discussed in terms of an income level, but its true definition encompasses a lack of resources necessary to maintain a minimum standard of living, including adequate food, shelter, healthcare, and other basic necessities. While an official poverty line provides a quantitative benchmark, it doesn’t fully capture the qualitative aspects of deprivation, insecurity, and exclusion that define the experience of poverty. The global context further complicates this, with different nations employing distinct methodologies tailored to their specific economic realities and social safety nets.

The Evolution of Poverty Measurement

The modern approach to defining poverty, particularly in developed nations like the United States, largely originated in the mid-20th century. In the U.S., the official poverty threshold was developed in the 1960s by Mollie Orshansky, an economist at the Social Security Administration. Her methodology was based on the cost of a minimum food diet multiplied by three, reflecting the understanding that food constituted approximately one-third of a family’s budget at the time. This initial calculation established a benchmark that has since been updated annually for inflation, forming the basis of the Federal Poverty Level (FPL). While groundbreaking for its time, this method has faced significant criticism for its static nature and its failure to adapt to changing consumption patterns and economic realities over the decades. The original assumption that food consumes one-third of a household budget is no longer accurate, with housing, healthcare, and transportation often consuming far greater proportions today.

Absolute vs. Relative Poverty

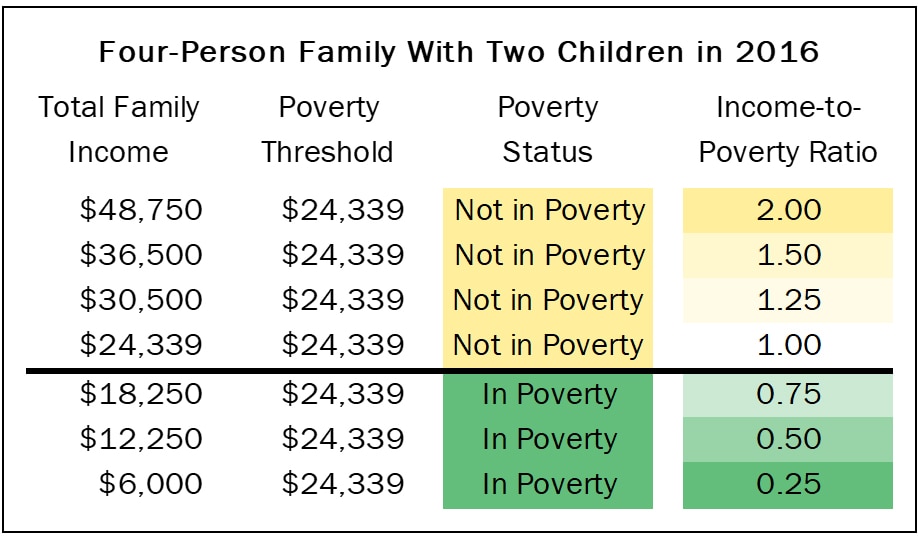

It’s important to distinguish between absolute and relative poverty. Absolute poverty refers to a condition where people lack the basic necessities for survival, such as food, water, shelter, and sanitation. It’s typically measured against a fixed international standard, like the World Bank’s international poverty line (currently $2.15 a day for extreme poverty). This form of poverty is most prevalent in developing countries. Relative poverty, on the other hand, describes a condition where people lack the minimum amount of income needed to maintain the average standard of living in the society in which they live. This means a person could be above the absolute poverty line but still experience relative poverty if their income is significantly lower than the median income of their country. Most developed nations, including the U.S., primarily focus on measuring absolute poverty for official statistics, though the concept of relative poverty is gaining traction in discussions about income inequality and social exclusion. Both forms present distinct challenges and require different policy approaches.

The Official Poverty Line: Understanding the Metrics

In the United States, the yearly income considered poverty is determined by the Federal Poverty Levels (FPL), also known as the poverty thresholds. These thresholds are a set of income cutoffs that vary by family size and composition, established by the U.S. Census Bureau and updated annually by the Department of Health and Human Services (HHS). While these figures provide a national benchmark, their practical application and underlying assumptions warrant closer examination.

Federal Poverty Levels (FPL) and Their Calculation

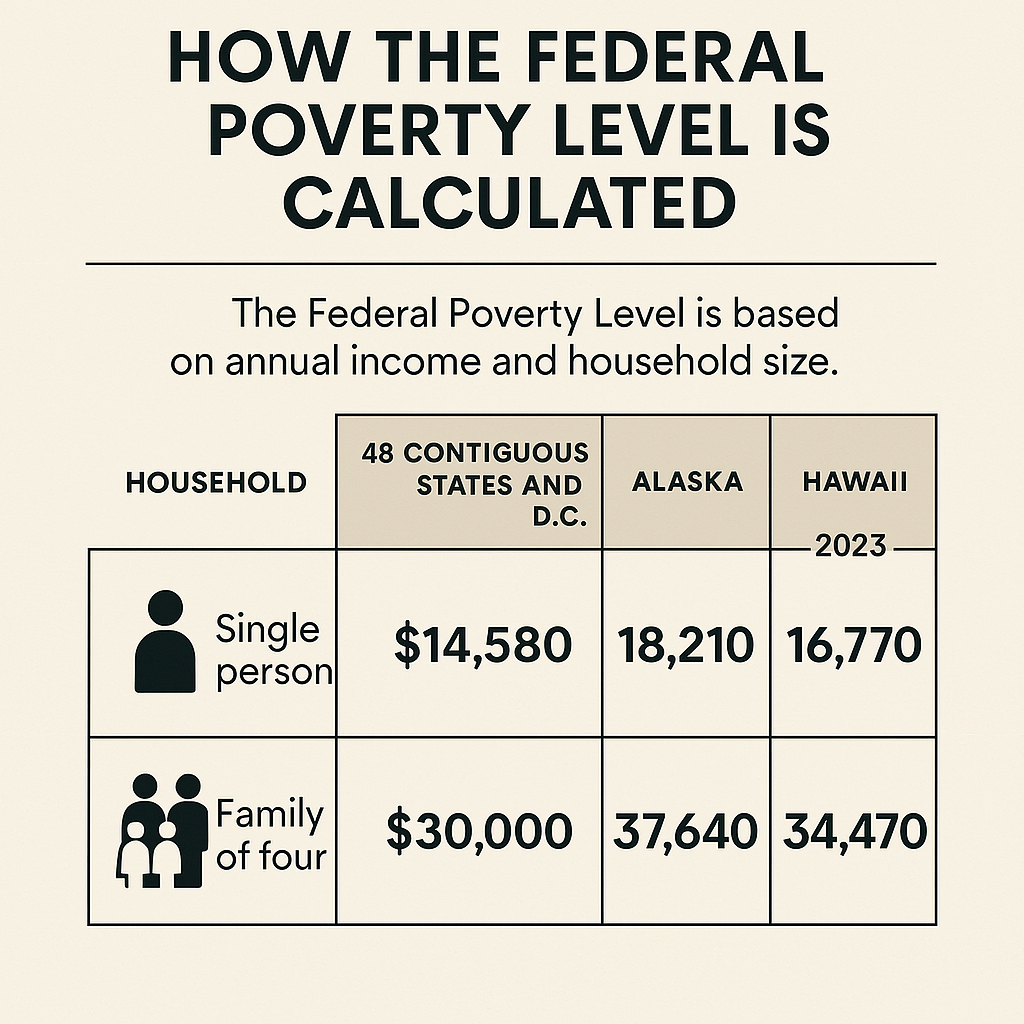

The FPLs are derived from the official poverty thresholds developed in the 1960s. For example, for 2024, the poverty guideline for a single person in the 48 contiguous states and D.C. might be approximately $15,060, while for a family of four, it could be around $31,200. These figures are higher for Alaska and Hawaii due to their elevated cost of living. The calculation begins with a base threshold for a single person and then increases incrementally for each additional family member. This scaling is meant to reflect the economies of scale that larger households may experience (e.g., sharing rent or utilities). However, a key limitation is that it doesn’t adequately account for the specific needs of different age groups within a household, nor does it differentiate between urban and rural living costs, except for the Alaska and Hawaii adjustments. This standardized approach, while providing a consistent measure, often fails to reflect the nuanced financial realities across diverse regions of the country.

Limitations of the FPL: The Poverty “Trap”

Despite its widespread use, the FPL faces significant criticism for its outdated methodology and its failure to reflect contemporary economic realities.

- Outdated Formula: As mentioned, the FPL is still based on the 1960s assumption that food costs constitute one-third of a household’s budget. Today, housing, childcare, transportation, and healthcare often consume a much larger portion of a low-income family’s budget, sometimes exceeding 70-80% of their income. This means that a family technically above the FPL might still struggle to afford basic necessities.

- Exclusion of Non-Cash Benefits: The FPL only considers pre-tax cash income. It does not account for non-cash benefits such as SNAP (food stamps), housing subsidies, Medicaid, or the Earned Income Tax Credit (EITC). While these programs significantly alleviate poverty, their impact is not reflected in the official poverty statistics, leading to an overestimation of the number of people living in poverty if only cash income is considered.

- Geographic Variation in Cost of Living: A major flaw is the FPL’s failure to adequately adjust for vast differences in the cost of living across different regions of the country. Living on $30,000 for a family of four in a rural town in Mississippi is vastly different from living on the same income in San Francisco or New York City, where housing costs alone can consume a disproportionate share of that income. This disparity means that families just above the FPL in high-cost areas are often experiencing financial hardship comparable to or even greater than those below the FPL in lower-cost regions. This creates a “poverty trap” where individuals might earn just enough to be above the official line, losing access to crucial support programs, but still not enough to live comfortably or even adequately.

Beyond the Basics: The Lived Experience of Poverty

While the official poverty line provides a statistical marker, the true experience of living in poverty is far more complex and goes beyond a mere income deficit. It impacts every facet of an individual’s life, creating chronic stress, limiting opportunities, and perpetuating cycles of disadvantage. Understanding these lived realities is essential for appreciating the true weight of financial hardship.

The “Working Poor” Phenomenon

A significant and often overlooked segment of the impoverished population comprises the “working poor.” These are individuals and families who are employed, often full-time, but whose wages are insufficient to lift them above the poverty line or provide for a decent standard of living. Despite their consistent efforts, they struggle with food insecurity, inadequate housing, lack of access to healthcare, and the inability to save for emergencies or their future. The rise of low-wage service jobs, the decline in real wages, and the increasing cost of living have all contributed to the growth of the working poor. This phenomenon challenges the conventional narrative that employment automatically guarantees an escape from poverty, highlighting the need for policies that ensure livable wages and accessible benefits for all workers. For these families, a single unexpected expense—a car repair, a medical bill, or a childcare emergency—can be catastrophic, pushing them deeper into debt and instability.

The Poverty Trap and Intergenerational Impact

The “poverty trap” refers to a self-perpetuating cycle where individuals or communities face significant barriers to economic advancement, making it exceedingly difficult to escape poverty. This trap is often reinforced by a lack of access to quality education, healthcare, stable employment, and financial resources. Children born into poverty are disproportionately affected, facing limited opportunities, poorer health outcomes, and reduced access to essential services, perpetuating the cycle across generations. The lack of resources often means families cannot invest in their children’s education or health, which limits their future earning potential. Additionally, the constant stress of financial insecurity can take a significant toll on mental and physical health, further hindering individuals’ ability to improve their circumstances. Breaking this intergenerational cycle requires comprehensive interventions that address not just income deficits but also systemic barriers to opportunity and well-being. This includes investments in early childhood education, affordable housing, job training, and robust social safety nets.

Hidden Costs of Being Poor

Living in poverty comes with a host of hidden costs that often go unrecognized by those outside the experience.

- Higher Costs for Essentials: The poor often pay more for basic necessities. For example, without bank accounts, they rely on check-cashing services that charge hefty fees. Without access to reliable transportation, they may be forced to shop at more expensive local convenience stores rather than cost-effective supermarkets. Payday loans, with their exorbitant interest rates, become the only option for emergencies.

- Health Disparities: Poverty is strongly linked to poorer health outcomes. Lack of access to nutritious food, safe housing, and consistent healthcare leads to higher rates of chronic diseases and mental health issues. Stress related to financial insecurity further exacerbates these problems.

- Time Poverty: The constant struggle to make ends meet consumes an immense amount of time. Navigating public services, commuting long distances on public transport, working multiple jobs, and searching for affordable options leaves little time for personal development, leisure, or even quality family time, which can further limit opportunities for advancement.

Pathways to Financial Stability and Policy Interventions

Addressing poverty requires a multi-pronged approach that goes beyond simply adjusting income thresholds. It involves strengthening social safety nets, promoting economic opportunity, and tackling systemic inequalities that perpetuate financial hardship. Individual actions, community initiatives, and robust policy interventions all play critical roles in helping individuals and families move towards greater financial stability.

Policy Solutions and Government Programs

Governments at all levels play a crucial role in mitigating poverty through various programs and policies.

- Minimum Wage Increases: Advocating for a living wage, rather than just a minimum wage, is a key strategy. A wage that truly reflects the cost of living in a given area can significantly lift families out of poverty and reduce reliance on public assistance.

- Social Safety Net Programs: Programs like SNAP (food stamps), Medicaid, housing assistance, and the Earned Income Tax Credit (EITC) provide vital support to low-income families, helping them cover basic needs and reducing their financial burden. Expanding access to these programs and ensuring their adequacy are critical.

- Affordable Childcare and Education: Investing in accessible, high-quality early childhood education and affordable higher education or vocational training can break the cycle of intergenerational poverty by equipping individuals with the skills needed for better-paying jobs.

- Healthcare Reform: Ensuring universal access to affordable healthcare is paramount, as medical debt is a leading cause of bankruptcy and financial instability for many families, even those with insurance.

Community Initiatives and Empowerment

Beyond government action, community-led initiatives and non-profit organizations are essential in providing targeted support and fostering local empowerment.

- Food Banks and Pantries: These organizations address immediate food insecurity, providing essential nutrition to families struggling to make ends meet.

- Financial Literacy and Coaching: Offering free or low-cost financial literacy workshops and one-on-one coaching can equip individuals with the knowledge and tools to manage their money, build savings, and make informed financial decisions.

- Job Training and Placement Services: Community programs that provide job skills training, resume building, interview preparation, and job placement assistance can help individuals secure better employment opportunities.

- Affordable Housing Programs: Local initiatives focused on creating and preserving affordable housing options are critical in high-cost areas, ensuring that families can secure stable and safe shelter without disproportionate financial strain.

Individual Financial Planning and Resilience

While systemic issues demand systemic solutions, individuals can also take steps to build financial resilience, even when facing challenging circumstances.

- Budgeting and Saving: Creating a realistic budget, tracking expenses, and striving to save even small amounts can help build an emergency fund, which is crucial for weathering unexpected financial shocks.

- Emergency Fund Development: Prioritizing the creation of an emergency fund, even if it starts with a modest amount, can prevent minor setbacks from escalating into major financial crises.

- Debt Management: Understanding and strategically managing debt, prioritizing high-interest debts, and seeking credit counseling services can alleviate financial pressure.

- Skill Development: Investing in personal skill development, whether through formal education, vocational training, or online courses, can lead to increased earning potential and better career opportunities.

- Accessing Benefits: Actively seeking out and applying for eligible government benefits and community resources can significantly improve financial stability.

The question of “what yearly income is considered poverty” opens a window into the broader landscape of economic inequality and human struggle. While official thresholds provide a necessary starting point for data collection and policy formulation, they fall short of capturing the full scope of hardship faced by those living on the margins. A truly effective approach to alleviating poverty requires a nuanced understanding of its definitions, its causes, its lived experience, and a commitment to comprehensive, multi-faceted solutions that address both immediate needs and systemic barriers to financial well-being. By fostering economic opportunity, strengthening social safety nets, and empowering individuals with financial literacy and resources, societies can move closer to a future where poverty is not merely a statistical benchmark, but a diminishing reality.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.