The allure of the open water is undeniable, offering escape, adventure, and a unique connection with nature. However, beneath the serene surface lies a spectrum of risks, and understanding which boating activities carry the highest statistical likelihood of fatalities is not just a matter of safety awareness; it’s a critical element of financial prudence. For individuals, insurers, and the marine industry at large, a deep dive into the fatality data reveals patterns that directly translate into financial considerations, from personal investment in safety gear to the actuarial calculations that underpin insurance premiums and the economic viability of maritime enterprises. This analysis explores the types of boating that statistically lead to the most fatalities, framing it through the lens of financial risk and the economic impact of safety.

The Cost of Negligence: Unpacking the Financial Ramifications of Boating Fatalities

Fatalities at sea or on inland waterways are not merely tragic events; they represent a significant financial burden. Beyond the immeasurable grief, these incidents incur substantial costs that ripple through various sectors. From emergency response and investigation expenses to legal liabilities and the loss of productive individuals within the workforce, the economic fallout is considerable. Understanding the root causes of these fatalities allows for targeted investment in preventative measures, which, in the long run, offers a significant return on investment by mitigating financial losses.

Drowning: The Overwhelming Economic Driver of Boating Fatalities

Statistics consistently point to drowning as the leading cause of death in boating accidents. This stark reality has profound financial implications. The immediate costs associated with a drowning victim include search and rescue operations, which are often publicly funded and can run into hundreds of thousands or even millions of dollars, depending on the complexity and duration. Furthermore, the legal ramifications for negligence, if applicable, can result in substantial settlements or judgments, impacting individuals and businesses alike.

The Insurance Landscape: How Fatality Data Influences Premiums

For the insurance industry, fatality data is the bedrock of risk assessment. Insurers meticulously analyze accident statistics to determine the likelihood of claims. Boating activities that have a higher propensity for fatal accidents will invariably attract higher insurance premiums. This directly impacts the cost of ownership for recreational boaters and the operational expenses for commercial entities. A boater engaging in activities statistically proven to be riskier, such as watersports or operating in challenging conditions, will find their insurance costs reflecting that elevated risk. For businesses, such as charter companies or tour operators, comprehensive insurance is a non-negotiable expense, and the type of operations they conduct will directly influence their actuarial models and, consequently, their bottom line. The financial decision to participate in a particular type of boating must therefore be weighed against the insurance costs associated with its inherent risks.

The Economic Impact of Lost Lives: Beyond the Immediate Costs

The economic impact of lost lives extends far beyond immediate expenses. Each fatality represents the loss of a potential contributor to the economy, be it through wages earned, taxes paid, or consumption. For families, the loss of a breadwinner can lead to devastating financial hardship, often necessitating significant lifestyle adjustments and reliance on insurance payouts or social support systems. For businesses, particularly those reliant on skilled maritime labor, a fatality can disrupt operations, leading to delays, loss of contracts, and reputational damage, all of which have tangible financial consequences.

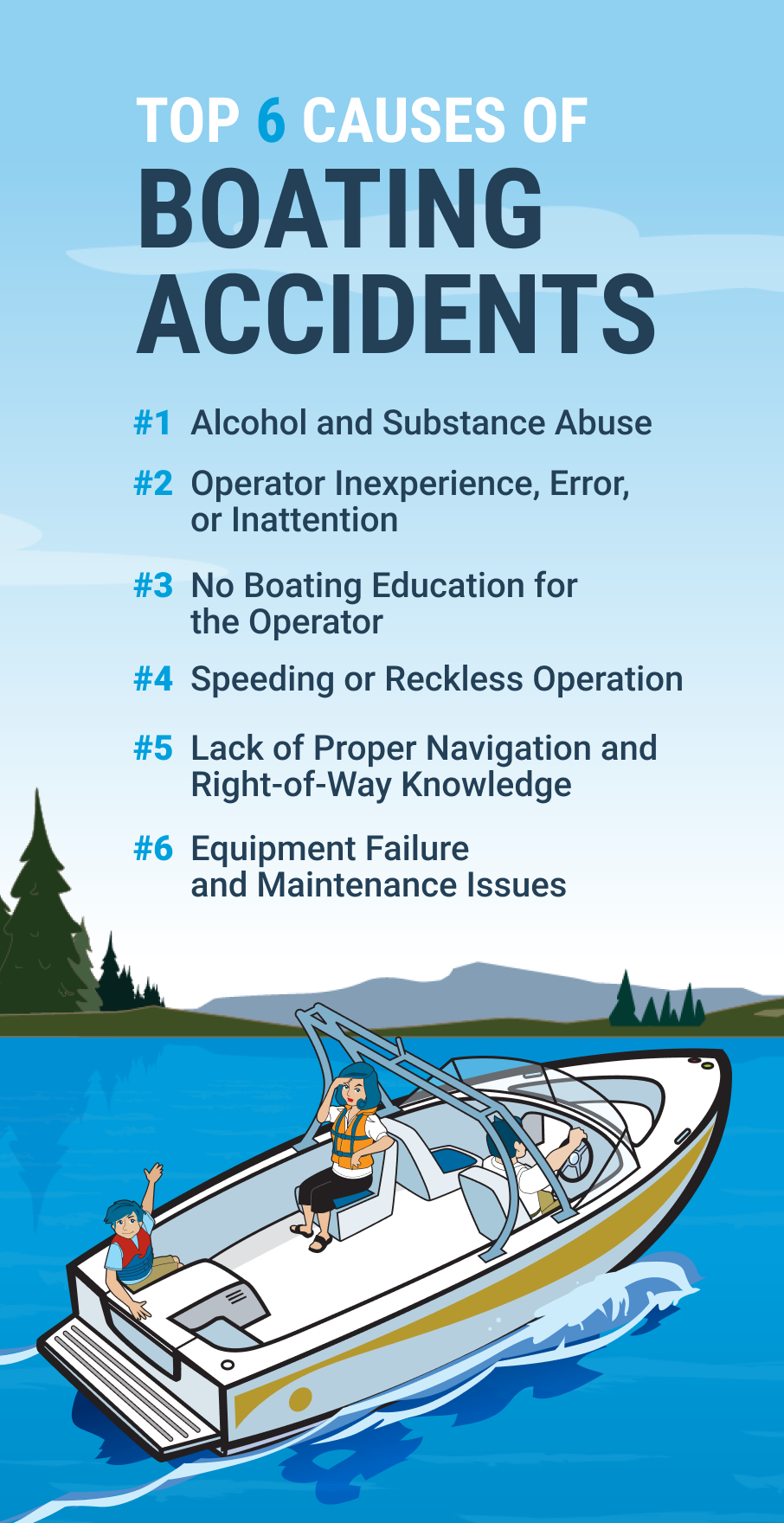

High-Risk Activities: Identifying the Financial Vulnerabilities in Boating

Certain types of boating activities, by their very nature, expose participants to a statistically higher risk of fatalities. Recognizing these activities is crucial for making informed financial decisions regarding safety investments and operational planning. The financial burden associated with these higher-risk pursuits can manifest in various ways, from the upfront cost of specialized safety equipment to the potential for increased insurance premiums and the broader economic impact of preventable accidents.

Personal Watercraft (PWCs): A Statistical High-Roller in Fatalities and Associated Costs

Personal watercraft (PWCs), such as jet skis, are frequently cited in accident statistics, and while the total number of fatalities might be lower than for larger vessels due to their prevalence, their fatality rate per user can be concerning. The inherent design of PWCs, often operated at high speeds and with less stability than traditional boats, contributes to this. The financial implications here are multifaceted. The cost of operating a PWC, while seemingly lower than a large yacht, is amplified by the potential for severe accidents. Injuries sustained on PWCs can be catastrophic, leading to lengthy rehabilitation periods and significant medical expenses.

PWC Operator Behavior and Financial Repercussions

A significant factor contributing to PWC fatalities is operator error, often involving reckless behavior, excessive speed, and operating under the influence of alcohol or drugs. These behaviors not only increase the risk of a fatal accident but also have direct financial repercussions. If an accident results in injury or death to another party, the PWC operator can face substantial legal liabilities, including personal injury lawsuits and potential criminal charges. The cost of legal defense and any resulting settlements or judgments can be financially ruinous. Furthermore, a history of accidents or citations can lead to significantly higher insurance premiums for PWC owners, or even a complete inability to obtain coverage.

The Role of Training and Safety Equipment in Mitigating Financial Risk

Investing in proper PWC training and adhering to safety guidelines are not just about personal safety; they are sound financial decisions. Certified training programs often equip operators with the knowledge and skills to navigate hazardous situations, thereby reducing the likelihood of an accident. Similarly, ensuring that all safety equipment, such as life jackets and kill switches, is functional and used correctly can prevent a minor incident from escalating into a fatality. The cost of this training and equipment is a fraction of the potential financial loss associated with a serious accident. For commercial operators who rent out PWCs, providing mandatory safety briefings and ensuring renters are trained can significantly reduce their liability and insurance costs.

Watersports and Towing Activities: The Financial Equation of Adrenaline

Activities like waterskiing, wakeboarding, and tubing, while exhilarating, introduce another layer of risk to boating. These activities inherently involve towing individuals behind a moving vessel, creating dynamic and often unpredictable scenarios. The financial considerations associated with these sports revolve around the combined risks of the vessel operation and the towed participant’s actions.

Common Accident Scenarios and Their Economic Fallout

Collisions with other boats, fixed objects, or even the towed individual falling incorrectly can lead to severe injuries or fatalities. The cost of medical treatment for broken bones, head injuries, and other trauma can be substantial, particularly if long-term rehabilitation is required. For boat owners, the liability in such incidents can be significant, especially if the operator was negligent or failed to adequately supervise the towed individual. Insurance claims arising from these accidents can impact future premiums, and in severe cases, legal action can lead to significant financial settlements.

The Financial Benefit of Proactive Safety Measures in Watersports

The key to mitigating the financial risks associated with watersports lies in proactive safety measures. This includes ensuring the towed individual is wearing a properly fitted life jacket, establishing clear communication signals between the boat operator and the skier/rider, and maintaining a safe distance from other vessels and obstacles. For commercial operators offering watersports as part of their services, comprehensive waivers, mandatory safety briefings, and experienced instructors are crucial for managing financial exposure. The upfront investment in proper safety gear and training is a far more economical approach than facing the devastating financial and emotional consequences of a serious accident.

Small Boat Operations and Falls Overboard: The Stealthy Financial Drain

While large-scale recreational vessels and high-octane watersports often grab headlines, small boat operations, particularly those involving fishing or leisure cruising, account for a significant number of fatalities, with falls overboard being a common precursor. The perceived simplicity of operating small boats can sometimes lead to complacency, which can have severe financial repercussions.

The Underestimated Dangers of Small Vessels and Unexpected Capsizes

Many small boats, especially those under 16 feet, may not be equipped with the same stability or safety features as larger vessels. In choppy conditions or when subjected to sudden shifts in weight, these boats can capsize unexpectedly, leading to falls overboard and potential drowning. The financial cost here can be immediate and severe. If the capsizing is due to negligence or a poorly maintained vessel, the owner can face significant liability. The cost of rescue operations, even for a small boat, can be substantial, and if the boat is lost or damaged, replacement costs add to the financial burden.

Falls Overboard: The Preventable Tragedy and its Financial Impact

Falls overboard are often preventable and are frequently linked to factors such as intoxication, unsecured footing, or leaning too far over the side. When a fatality occurs from a fall overboard, the financial implications are similar to other drowning incidents: search and rescue costs, potential legal liabilities, and the immeasurable loss of a life. However, the preventative measures are often relatively inexpensive. Ensuring good lighting on deck, installing grab rails, maintaining dry and clear walking surfaces, and implementing a strict “buddy system” or ensuring everyone aboard is accounted for are all low-cost strategies that can significantly reduce the financial risk associated with falls overboard. For individuals and businesses alike, understanding that seemingly minor oversights on small boats can lead to catastrophic financial losses underscores the importance of vigilance and investment in basic safety protocols.

In conclusion, while the primary concern surrounding boating fatalities is, of course, the preservation of human life, the financial implications are undeniable and far-reaching. From the direct costs of rescue and medical care to the long-term economic impacts on families and industries, understanding which boating activities statistically lead to the most fatalities is a critical component of sound financial risk management. By investing in education, proper equipment, and a culture of safety, individuals and businesses can not only protect lives but also safeguard their financial well-being, making the pursuit of enjoyment on the water a responsible and economically sound endeavor.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.