Navigating the landscape of higher education finance can often feel like deciphering a complex code, filled with acronyms and nuanced terms. Among the most common financial aid offerings is the unsubsidized loan – a vital resource for countless students pursuing their academic and career aspirations. Unlike its subsidized counterpart, which often garners more attention due to its favorable terms, the unsubsidized loan operates under a distinct set of rules, particularly concerning interest accrual. Understanding “what is an unsubsidized loan” isn’t just about defining a financial product; it’s about grasping a critical component of personal finance that can profoundly impact a student’s long-term financial health, future investment opportunities, and even their emerging professional brand.

In an increasingly digital world, where personal finance intersects with cutting-edge technology and individual reputation is meticulously curated, mastering the intricacies of student debt management becomes paramount. This article will delve deep into the mechanics of unsubsidized loans, demystifying their operations, and critically, exploring how modern technology can empower borrowers. Furthermore, we’ll examine the broader implications of these loans on one’s personal financial brand, offering strategic insights to not only manage debt effectively but also to leverage that management as a testament to financial acumen and responsibility. Whether you’re a prospective student, a current borrower, or simply seeking to broaden your financial literacy, understanding unsubsidized loans is a foundational step towards building a robust financial future.

Understanding the Mechanics of Unsubsidized Loans

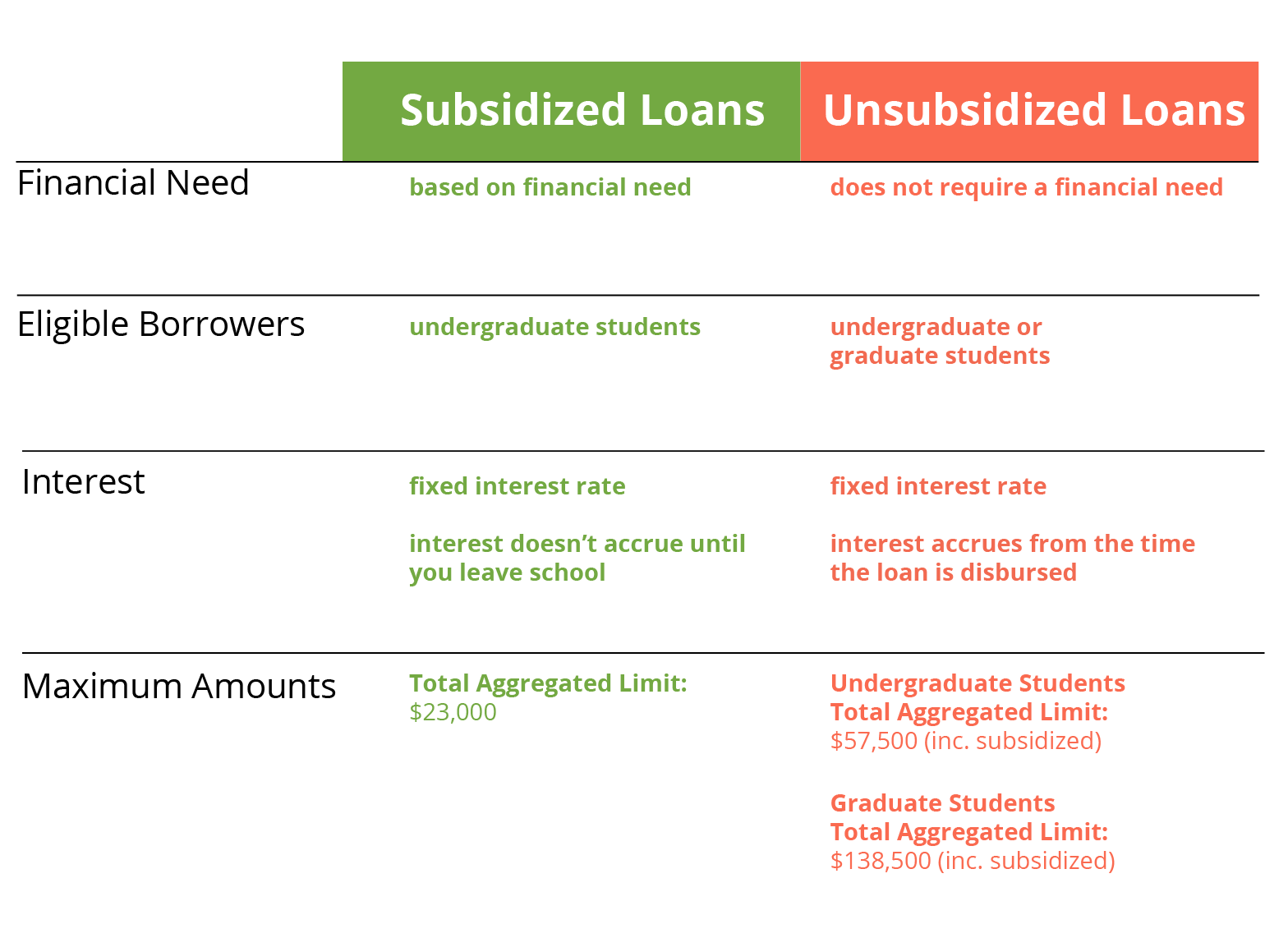

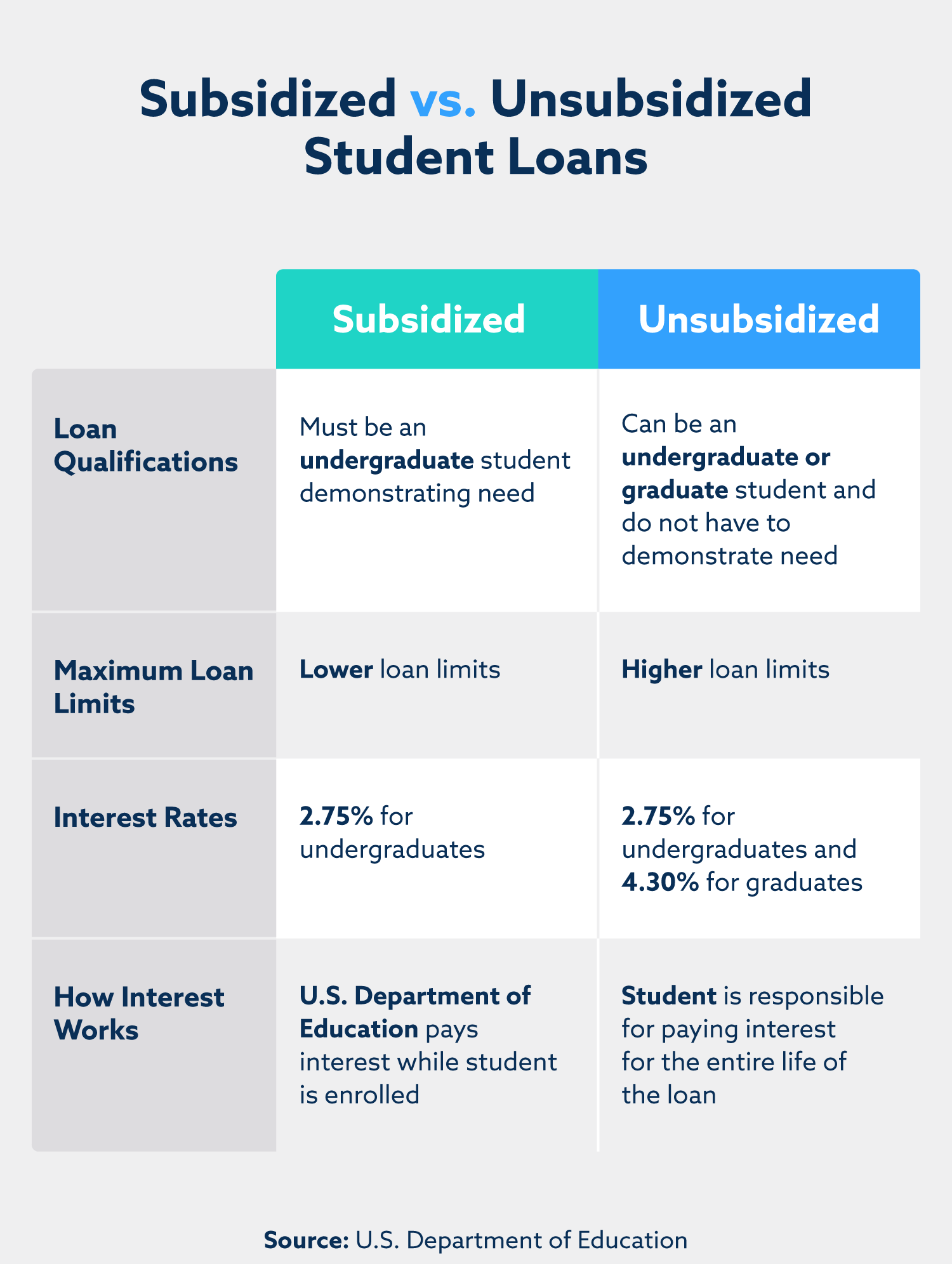

At its core, a Federal Direct Unsubsidized Loan is a type of federal student loan available to both undergraduate and graduate students, regardless of their financial need. This “non-need-based” characteristic is one of its most defining features, setting it apart from subsidized loans which are reserved for students demonstrating financial hardship. While this inclusivity makes unsubsidized loans accessible to a wider pool of students, it also comes with a significant distinction that every borrower must understand: interest accrual.

The Core Difference: Interest Accrual

The most crucial difference between an unsubsidized loan and a subsidized loan lies in when interest begins to accrue. For a subsidized loan, the U.S. Department of Education pays the interest while the student is in school at least half-time, during the grace period (typically six months after leaving school), and during periods of deferment. This means the loan balance doesn’t grow during these times.

In stark contrast, interest on an unsubsidized loan begins to accrue immediately after the loan is disbursed, even while the student is still enrolled in school. This interest continues to accumulate during the grace period and any periods of deferment or forbearance. If the borrower doesn’t pay this accumulating interest, it will be added to the principal balance of the loan, a process known as capitalization. Capitalization significantly increases the total amount owed because future interest will then be calculated on a larger principal. For example, if you borrow $10,000 at a 5% interest rate, and $500 in interest capitalizes, your new principal becomes $10,500, and subsequent interest will be calculated on that higher amount. This seemingly small detail can lead to a substantially larger repayment burden over the life of the loan, making it imperative for borrowers to grasp this concept fully.

Eligibility and Loan Limits

To be eligible for a Federal Direct Unsubsidized Loan, students must complete the Free Application for Federal Student Aid (FAFSA). While the FAFSA is used to determine eligibility for all federal student aid, unsubsidized loans do not require demonstrating financial need. Key eligibility criteria include being enrolled at least half-time in an eligible program at an accredited institution and meeting general federal student aid requirements (e.g., U.S. citizen or eligible non-citizen, valid Social Security number, maintaining satisfactory academic progress).

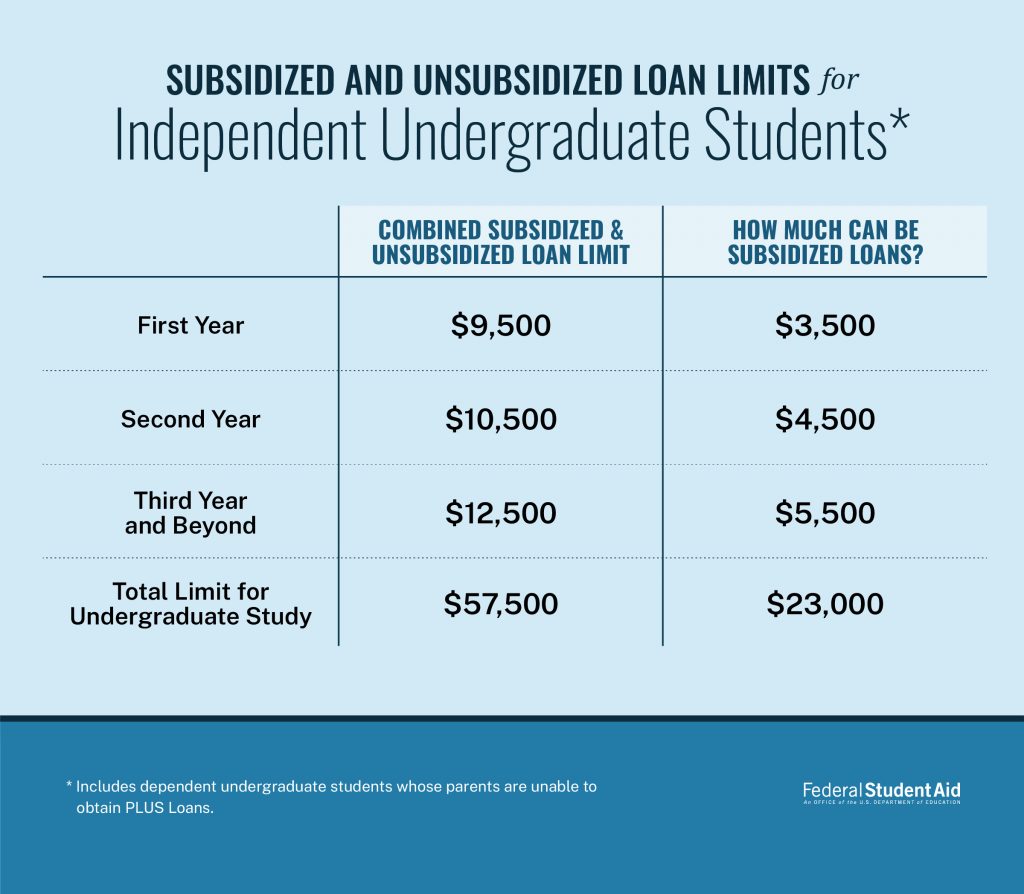

There are specific annual and aggregate loan limits for unsubsidized loans, which vary based on a student’s dependency status and academic level. For instance, independent undergraduate students can borrow more annually than dependent undergraduates, and graduate students have higher limits still. These limits include any subsidized loans a student may have received. It’s crucial for students to be aware of these limits to plan their borrowing strategy effectively and avoid exceeding the maximum amounts allowed over their academic careers. Understanding these limits is a foundational step in responsible borrowing, ensuring that students only take on what is absolutely necessary for their education.

Repayment and Deferment Options

Repayment for unsubsidized loans typically begins six months after a student graduates, leaves school, or drops below half-time enrollment. However, borrowers have several repayment plan options designed to accommodate different financial situations:

- Standard Repayment Plan: Fixed monthly payments for up to 10 years (or 30 years for consolidated loans). This typically results in the lowest total interest paid.

- Graduated Repayment Plan: Payments start low and gradually increase every two years, lasting up to 10 years.

- Extended Repayment Plan: For borrowers with more than $30,000 in direct loans, this plan allows for fixed or graduated payments over up to 25 years, resulting in lower monthly payments but more interest paid over time.

- Income-Driven Repayment (IDR) Plans: These plans (e.g., REPAYE, PAYE, IBR, ICR) adjust monthly payments based on income and family size, typically capping payments at 10-20% of discretionary income. Any remaining balance after 20 or 25 years of payments may be forgiven, though this forgiven amount is often considered taxable income.

Borrowers can also explore deferment or forbearance options if they face temporary financial hardship. While both allow for a temporary pause or reduction in payments, it’s vital to remember that interest continues to accrue on unsubsidized loans during these periods. This means deferment or forbearance can lead to significant capitalization of interest and a larger overall debt burden. For this reason, borrowers with unsubsidized loans should exercise these options judiciously and consider making interest-only payments if possible during these periods to prevent their loan balance from growing unnecessarily. Understanding these repayment and deferment mechanisms is not merely administrative; it’s a strategic financial decision that directly impacts the total cost of borrowing and one’s capacity to manage debt effectively.

Navigating Unsubsidized Loans with Technology and Financial Tools

In today’s interconnected world, managing personal finances, especially something as long-term as student debt, doesn’t have to be a manual, spreadsheet-heavy ordeal. The “Tech” pillar of our website comes alive when we consider the myriad of digital tools and technologies available to help borrowers track, manage, and even optimize their unsubsidized loans. From intuitive budgeting apps to advanced AI-powered financial planning, leveraging technology can transform the daunting task of debt management into a streamlined, efficient process, bolstering both productivity and financial security.

Leveraging Apps for Debt Management

The market is saturated with financial applications designed to simplify money management, and many are perfectly suited for overseeing student loans.

- Budgeting Apps (e.g., Mint, YNAB, Personal Capital): These apps allow users to link all their financial accounts, including student loan accounts, providing a holistic view of their financial health. They can track spending, categorize expenses, and help create budgets that factor in loan payments. Seeing where money goes helps identify areas to save, freeing up funds for extra loan payments to reduce capitalized interest.

- Loan Tracking Apps (e.g., ChangEd, Savvy): Some apps specifically focus on student loans, allowing borrowers to monitor their principal balance, interest accrual, and payment history across multiple servicers. Features often include round-up programs that automatically apply spare change to loan principal, accelerating repayment.

- Payment Reminder Apps: Simple but effective, these apps ensure you never miss a payment, protecting your credit score and avoiding late fees. Many banking apps and loan servicer portals also offer push notifications and email reminders.

By integrating these tools into daily routines, borrowers gain clearer insights into their financial flow, making it easier to make informed decisions about their unsubsidized loans and proactively mitigate the impact of accruing interest.

AI and Predictive Finance for Loan Optimization

The advent of Artificial Intelligence (AI) and machine learning is revolutionizing personal finance, offering sophisticated ways to manage debt.

- AI-Powered Financial Planners: Tools like those offered by some robo-advisors or specialized AI financial platforms can analyze your income, expenses, interest rates across various debts (including unsubsidized loans), and future financial goals. They can then recommend optimized repayment strategies, such as the “debt snowball” or “debt avalanche” methods, tailored to your specific situation. For unsubsidized loans, an AI might suggest making interest-only payments during in-school or grace periods to prevent capitalization, or it could forecast the impact of an extra payment on your total interest paid.

- Predictive Analytics for Interest Forecasting: Advanced software can project how your unsubsidized loan balance will grow over time under different scenarios (e.g., making minimum payments, making extra payments, utilizing deferment). This foresight is invaluable for understanding the true cost of borrowing and empowering borrowers to adjust their strategies to minimize interest capitalization.

- Personalized Advice Engines: Beyond just numbers, some AI tools can provide personalized advice on refinancing options, eligibility for different repayment plans, or even suggest side hustles to generate extra income for debt repayment, truly connecting the “Tech” and “Money” aspects.

While these tools are still evolving, they offer a glimpse into a future where managing complex financial products like unsubsidized loans becomes increasingly intelligent and personalized, empowering borrowers with data-driven insights to make optimal choices.

Digital Security in Loan Management

As more of our financial lives move online, the importance of digital security cannot be overstated. Managing unsubsidized loans involves sensitive personal and financial information, making it a prime target for cyber threats.

- Protecting Personal Data: Always use strong, unique passwords for loan servicer portals and financial apps, ideally with two-factor authentication (2FA). Be wary of public Wi-Fi when accessing financial accounts.

- Secure Online Portals: Legitimate loan servicers use encrypted, secure websites. Always verify the URL and look for “https://” in the address bar. Avoid clicking on suspicious links in emails or texts that claim to be from your loan servicer.

- Phishing and Scams: Be vigilant against phishing attempts that try to trick you into revealing your login credentials or personal information. Student loan scams are unfortunately common, often promising too-good-to-be-true loan forgiveness or consolidation offers. Always verify information directly with your servicer or the Department of Education.

- Regular Monitoring: Regularly review your loan statements and credit reports for any suspicious activity. Early detection of fraud can prevent significant financial harm.

Prioritizing digital security ensures that while you’re leveraging technology to manage your loans more efficiently, you’re also safeguarding your financial identity and peace of mind.

Productivity Hacks for Financial Planning

Integrating digital tools with smart habits can boost your productivity in managing unsubsidized loans.

- Automating Payments: Set up automatic monthly payments for your loans directly from your bank account. This ensures on-time payments, often comes with a small interest rate reduction from servicers, and frees up mental space.

- Digital Document Management: Use cloud storage (like Google Drive, Dropbox, OneDrive) to keep all loan-related documents (award letters, promissory notes, payment confirmations) organized and easily accessible. This eliminates paper clutter and ensures you have a record of everything.

- Time Management for Financial Reviews: Schedule regular “financial check-up” appointments with yourself – perhaps once a month or quarter. Use this time to review loan balances, track progress, adjust budgets, and explore new repayment strategies. Treat it like any other important appointment.

By embracing these technological and productivity strategies, managing unsubsidized loans transitions from a passive burden to an active, empowering aspect of your financial journey, allowing you to minimize costs and maximize your future financial freedom.

The Brand Impact: How Unsubsidized Loans Shape Your Financial Identity

Beyond the pure numbers and technological tools, managing an unsubsidized loan, and debt in general, has a profound impact on one’s personal and professional brand. In an era where personal branding is critical for career advancement and social standing, responsible financial management becomes a cornerstone of a credible and trustworthy identity. How you handle your debt isn’t just about your bank account; it reflects on your discipline, responsibility, and foresight – qualities highly valued in any context, from securing future loans to building a successful career.

Building Your Personal Financial Brand

Your approach to managing an unsubsidized loan directly contributes to your personal financial brand, primarily through your credit score and reputation with lenders.

- Credit Score Implications: Making timely payments on your unsubsidized loans is a significant factor in building a strong credit history. A high credit score (a key indicator of your financial brand) demonstrates reliability to future lenders for mortgages, car loans, or even business financing. Conversely, missed payments or defaults can severely damage your credit, making it harder and more expensive to borrow in the future, thus tarnishing your financial brand.

- Reputation with Lenders: Your payment history creates a long-term record. Lenders evaluate this record to assess your risk profile. Consistently managing your student debt responsibly shows you are a reliable borrower, enhancing your reputation and potentially opening doors to better terms on future financial products.

- Discipline and Responsibility: Effectively managing a long-term debt like an unsubsidized loan showcases discipline and responsibility – traits that extend beyond finance. These qualities are attractive to employers, business partners, and even landlords, subtly bolstering your overall personal brand. It demonstrates a capacity for long-term planning and commitment.

By diligently managing your unsubsidized loans, you are actively cultivating a robust financial brand that underpins your credibility and opens up future opportunities.

Strategic Financial Planning for Long-Term Brand Growth

The decisions you make regarding your unsubsidized loans today resonate throughout your life, impacting your capacity for future financial growth and the strength of your brand.

- Influence on Future Opportunities: A heavy student loan burden, especially one that has grown due to capitalized interest, can delay major life milestones such as buying a home, starting a family, or launching a business. These delays can indirectly affect your professional brand by limiting your ability to invest in assets or ventures that typically signify professional success and stability.

- Importance of Financial Literacy for a Strong “Brand”: Proactively understanding the terms of your unsubsidized loan, exploring repayment options, and making educated choices about interest payments reflects a high degree of financial literacy. This literacy isn’t just a personal skill; it’s a valuable trait that contributes to a sophisticated personal brand, signaling intelligence and an ability to navigate complex systems. It shows you’re not just reacting to debt but strategically managing it.

- Conscious Consumerism in Finance: Choosing how much to borrow, considering the interest rates, and understanding the long-term cost is an act of conscious financial consumerism. This mindful approach to financial products also enhances your brand, demonstrating thoughtful decision-making rather than impulsive borrowing.

Strategic financial planning for unsubsidized loans, therefore, is not merely about debt reduction; it’s about building a solid foundation for long-term personal and professional brand growth.

Integrating Side Hustles and Online Income for Accelerated Repayment

In today’s dynamic economy, leveraging “Money” through online income and side hustles provides a powerful mechanism to accelerate unsubsidized loan repayment, which in turn significantly strengthens your financial brand.

- Proactive Debt Management: Actively seeking out additional income streams – be it through freelancing, gig work, or monetizing a hobby – to put towards your loan principal demonstrates extreme proactivity and financial ambition. This commitment to debt reduction stands out as a strong positive aspect of your brand.

- Enhanced Financial Freedom: Paying down unsubsidized loans faster reduces the total interest paid and frees up future cash flow sooner. This financial freedom allows for greater flexibility to invest in personal development, pursue entrepreneurial ventures, or save for significant assets – all of which contribute to a more powerful and dynamic personal brand.

- Showcasing Entrepreneurial Spirit: For many, a side hustle or online income venture is a form of entrepreneurship. Using these earnings to tackle debt showcases not only financial responsibility but also an entrepreneurial spirit and resourcefulness. These are highly desirable traits that can significantly boost your professional brand, signaling innovation and drive.

- Mitigating Capitalization: Directing extra income specifically towards paying down the accumulating interest on unsubsidized loans is a smart strategic move. It prevents capitalization, keeps the principal lower, and thus reduces the overall cost of the loan. This smart financial maneuvering is a testament to financial savviness, an invaluable component of a strong personal brand.

By strategically integrating online income and side hustles into your debt repayment strategy, you transform a financial obligation into an opportunity to build a powerful financial identity that resonates with responsibility, foresight, and ambition.

Making Informed Decisions: A Strategic Approach

Understanding what an unsubsidized loan is goes beyond its definition; it’s about making astute decisions that align with your financial goals and personal circumstances. The objective isn’t merely to borrow, but to borrow wisely, manage effectively, and ultimately minimize the long-term cost of your education. A strategic approach involves carefully weighing the pros and cons, adhering to best practices, and always keeping your long-term financial health in sight.

Weighing the Pros and Cons

Like any financial product, unsubsidized loans come with advantages and disadvantages that borrowers must consider:

Pros:

- Accessibility: Available to all eligible students regardless of financial need, making higher education attainable for many.

- Fixed Interest Rates: Federal unsubsidized loans typically have fixed interest rates, providing predictability in future payments.

- Federal Benefits: Offers various federal benefits, including income-driven repayment plans, deferment, and forbearance options, which are generally more flexible than private loans.

- Grace Period: Payments are not required while enrolled at least half-time and for six months after leaving school.

Cons:

- Interest Accrues Immediately: This is the primary drawback. Interest starts accumulating from disbursement, leading to a larger total repayment if not managed proactively.

- Capitalization: Unpaid interest can capitalize, increasing the principal balance and the total cost of the loan significantly.

- No Interest Subsidy: Unlike subsidized loans, the government does not pay interest on your behalf during in-school periods or deferment.

Understanding this balance is crucial for making an informed decision about whether an unsubsidized loan is the right choice for your specific educational and financial situation.

Best Practices for Borrowing

To mitigate the cons and maximize the pros of unsubsidized loans, consider these best practices:

- Borrow Only What You Need: Resist the urge to borrow the maximum amount offered. Calculate your true educational expenses and borrow only the difference between your costs and other aid. Every dollar borrowed is a dollar (plus interest) you’ll have to repay.

- Understand the Terms: Before signing, thoroughly read and understand the interest rate, repayment options, and the implications of interest capitalization. Don’t hesitate to ask your financial aid office or loan servicer for clarification.

- Make Interest Payments During Deferment if Possible: If you are in school, during your grace period, or in a period of deferment, try to make interest-only payments. Even small, consistent payments can prevent significant capitalization and save you money in the long run.

- Explore All Aid Options First: Prioritize grants, scholarships, and subsidized loans before turning to unsubsidized loans. These forms of aid do not accrue interest or do not need to be repaid.

- Maintain a Budget: A clear budget helps you understand your income and expenses, making it easier to identify funds that can be allocated towards your loan payments, potentially allowing you to pay more than the minimum.

Long-Term Financial Health

Managing unsubsidized loans is a critical component of your overall long-term financial health. Viewing your debt holistically, as part of your broader financial portfolio, is key. This means considering how your student loan burden impacts your ability to save for retirement, invest in a business, or achieve other financial milestones. Proactive and strategic management of these loans, leveraging both financial tools and personal discipline, not only minimizes the cost of your education but also sets a strong precedent for responsible financial behavior throughout your life. It ensures that your education remains an investment that truly pays off, rather than a financial burden that hinders future opportunities.

Conclusion

The unsubsidized loan, while a powerful tool for financing education, comes with distinct characteristics that demand careful consideration and proactive management. Its defining feature – the immediate accrual of interest – necessitates an informed and strategic approach to borrowing and repayment. Understanding “what is an unsubsidized loan” is the first step, but the journey truly begins with how you choose to manage it.

In an era defined by technological advancement and the increasing importance of personal branding, the strategies for managing unsubsidized loans are evolving. By leveraging innovative tech tools, from budgeting apps and AI-powered financial planners to robust digital security practices, borrowers can streamline their financial management, minimize interest capitalization, and gain unprecedented control over their debt. Furthermore, the discipline and foresight demonstrated in managing these loans actively contribute to a strong personal financial brand – a crucial asset that enhances creditworthiness, opens future opportunities, and signals overall responsibility and ambition.

Ultimately, an unsubsidized loan is more than just a line of credit; it’s a financial commitment that, when managed wisely, can be a springboard to educational and professional success. By embracing best practices, making informed decisions, and utilizing the resources available in our interconnected world, students and graduates can transform a potential burden into a testament to their financial acumen, paving the way for a more secure and prosperous future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.