In the complex ecosystem of modern finance, few numbers carry as much weight as the “Prime Rate.” For the average consumer, business owner, or investor, understanding today’s prime rate is not merely an academic exercise—it is a fundamental necessity for managing debt and planning for the future. Whether you are looking to purchase a home, apply for a small business loan, or manage your credit card balances, the fluctuations of this benchmark rate dictate the cost of borrowing and, by extension, your purchasing power.

The prime rate represents the base interest rate that commercial banks charge their most creditworthy corporate customers. While it is technically a rate for “prime” clients, it serves as the foundation for almost all consumer lending products. When the prime rate moves, the ripples are felt across the entire economy. In this guide, we will explore the mechanics of the prime rate, why it changes, and how you can navigate your financial life in response to its shifts.

The Mechanics of the Prime Rate: How It Is Determined

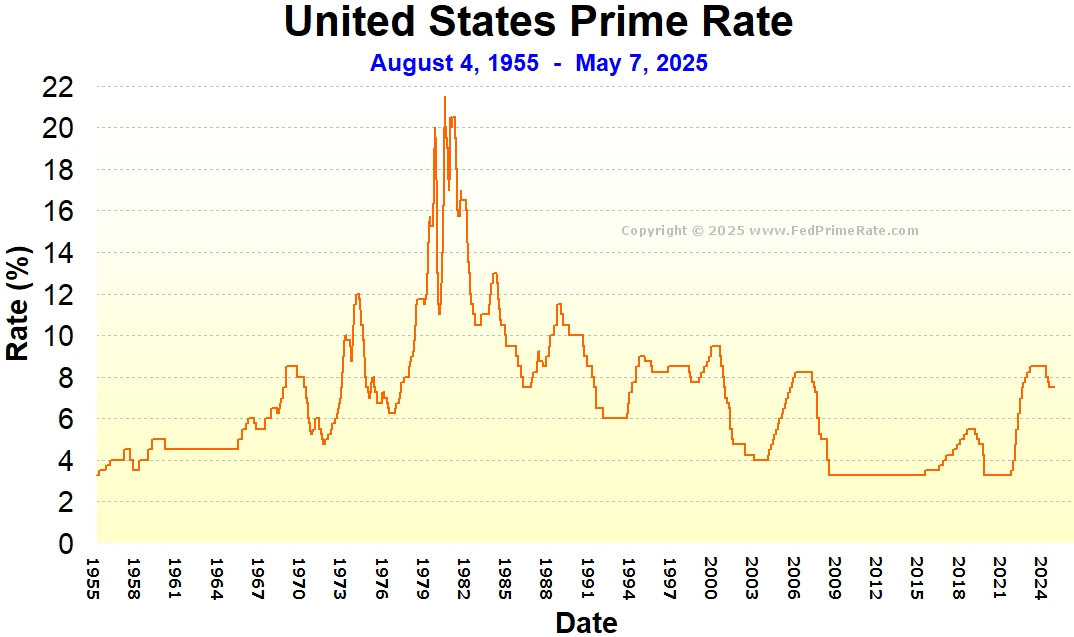

To understand today’s prime rate, one must first look at the Federal Reserve, the central bank of the United States. While the Federal Reserve does not “set” the prime rate directly, it controls the lever that makes it move.

The Federal Funds Rate Connection

The primary driver of the prime rate is the Federal Funds Rate. This is the interest rate at which commercial banks lend their excess reserves to one another overnight. The Federal Open Market Committee (FOMC) meets eight times a year to determine whether to raise, lower, or maintain this rate based on economic indicators like inflation and unemployment.

By industry standard, the prime rate is almost always set exactly 3 percentage points (300 basis points) above the Federal Funds Rate. Therefore, if the Federal Reserve sets the target range for the Fed Funds Rate at 5.25% to 5.50%, the prime rate will typically sit at 8.50%. This 3% spread allows banks to cover their operating costs and manage the risks associated with lending while maintaining a profit margin.

Who Actually Sets the Prime Rate?

While the Federal Reserve influences the environment, individual banks are responsible for setting their own prime rates. However, because the banking industry is highly competitive, most major financial institutions move in lockstep. The most widely cited benchmark is the “Wall Street Journal Prime Rate,” which is derived by surveying the 30 largest banks in the country. When at least 23 out of 30 of these banks change their prime rate, the WSJ updates its published benchmark. This consistency ensures that the lending market remains stable and predictable for both lenders and borrowers.

The Role of Inflation and Economic Health

The prime rate is a tool used to balance the economy. When inflation is high, the Federal Reserve raises rates to “cool” the economy, making borrowing more expensive and slowing down spending. Conversely, during a recession, the Fed lowers rates to encourage borrowing and stimulate economic activity. Today’s prime rate is a reflection of this ongoing tug-of-war between growth and price stability.

Why the Prime Rate Matters to Your Personal Wallet

For the individual consumer, the prime rate is rarely a static number on a screen; it is a dynamic force that affects monthly bills and long-term savings. Most consumer debt is “variable,” meaning the interest rate you pay is tied directly to a benchmark—most often, the prime rate.

The Immediate Impact on Credit Cards

Credit cards are perhaps the most sensitive financial products to changes in the prime rate. Most credit cards have a Variable Annual Percentage Rate (APR). Your card’s interest rate is calculated as the [Prime Rate + a Margin]. For example, if your margin is 15% and the prime rate is 8.5%, your APR is 23.5%.

When the prime rate increases by 0.25%, your credit card interest rate usually follows suit within one or two billing cycles. Over a year, these incremental increases can add hundreds or even thousands of dollars to the cost of carrying a balance. In a high-prime-rate environment, the “cost of carry” for consumer debt becomes a significant burden on household budgets.

HELOCs and Variable-Rate Mortgages

Homeowners with Home Equity Lines of Credit (HELOCs) are also directly affected. Unlike a traditional fixed-rate mortgage, a HELOC is a revolving line of credit that typically uses the prime rate as its index. As the prime rate climbs, the interest-only or principal-plus-interest payments on a HELOC can rise sharply, potentially straining a homeowner’s cash flow.

While most standard 30-year mortgages are fixed-rate and do not change with the prime rate once they are signed, new mortgage applications are influenced by the broader interest rate environment. When the prime rate is high, the overall cost of capital for banks is higher, which generally leads to higher rates for all types of home loans.

Personal Loans and Auto Financing

While many auto loans are fixed-rate at the time of purchase, the “starting” rates offered by dealerships and banks are influenced by the prime rate. If you are shopping for a new car when the prime rate is high, you will likely face higher monthly payments than you would have a year or two prior. Personal loans, often used for debt consolidation, also see their interest floors rise in tandem with the prime rate, making it more difficult to find “cheap” money for restructuring debt.

The Business Perspective: Commercial Lending and Expansion

The prime rate is not just a consumer concern; it is the lifeblood of business finance. Small and medium-sized enterprises (SMEs) are particularly sensitive to these shifts, as they often rely on credit lines to manage operations.

Small Business Administration (SBA) Loans

Many SBA loans, which are vital for entrepreneurs looking to start or grow a business, are pegged to the prime rate. Specifically, the popular SBA 7(a) loan program often uses a “Prime + Spread” formula. When the prime rate rises, the cost of doing business increases for thousands of local companies. This can lead to a slowdown in hiring or a delay in purchasing new equipment, as the cost of financing those investments becomes prohibitively expensive.

Working Capital and Inventory Financing

Businesses often use revolving lines of credit to bridge the gap between paying suppliers and receiving payments from customers. Because these lines of credit are almost always variable and tied to the prime rate, a rising rate environment increases the “cost of goods sold” indirectly. To maintain profit margins, businesses may be forced to pass these increased borrowing costs on to consumers in the form of higher prices, contributing to a cycle of inflation.

Commercial Real Estate and Development

In the world of commercial real estate, many construction loans are structured with variable rates tied to the prime rate. Developers must carefully calculate their “pro forma” projections based on expected interest costs. If the prime rate rises significantly during the construction phase, a project that was once profitable can quickly become a financial liability. This is why many developers use interest rate “swaps” or “caps” to protect themselves against the volatility of the prime rate.

Strategies to Manage Your Finances in a High-Rate Environment

When today’s prime rate is high, the goal for any savvy financial planner is to minimize interest expenses and maximize the efficiency of every dollar.

Debt Consolidation and Refinancing

If you are carrying high-interest debt tied to the prime rate, such as credit card balances, now is the time to look at fixed-rate consolidation options. Transferring variable-rate debt to a fixed-rate personal loan can “lock in” your interest costs, protecting you from future rate hikes. Even if the fixed rate is higher than historical lows, the predictability of a set monthly payment is a powerful tool for budgeting.

Boosting Your Credit Score to Mitigate Hikes

While you cannot control the prime rate, you can control the “margin” that lenders charge you. Lenders determine your specific interest rate by adding a risk premium to the prime rate. By improving your credit score—through timely payments, reducing credit utilization, and correcting errors on your credit report—you may qualify for a lower margin. In a world where the prime rate is 8.5%, a borrower with a 10% margin pays much less than a borrower with a 20% margin.

Focusing on Liquid Savings

There is one silver lining to a high prime rate: interest rates on savings accounts and Certificates of Deposit (CDs) tend to rise. As banks charge more for loans, they also offer more to attract deposits. High-yield savings accounts (HYSAs) often track the movements of the prime rate and the Fed Funds Rate. This is an opportune time to move “lazy” cash from a standard checking account into a high-yield vehicle to ensure your money is working as hard as possible.

Conclusion: Staying Informed for Long-Term Success

“What is today’s prime rate?” is a question that serves as a pulse check for the broader economy. It is a reflection of the Federal Reserve’s strategy, the banking sector’s health, and the general cost of living. While the number itself may change from month to month, its influence remains constant.

By understanding that the prime rate is the foundation upon which your credit cards, HELOCs, and business loans are built, you can make more informed decisions about when to borrow and when to pay down debt. In a high-rate environment, the premium is on liquidity and debt reduction. In a low-rate environment, the focus shifts to strategic borrowing and investment. Regardless of where the rate sits today, staying educated on these financial benchmarks is the most effective way to ensure your personal and professional financial health remains robust in any economic climate.