In the complex world of global economics, the term “money” is often used as a catch-all phrase. However, to economists, central bankers, and sophisticated investors, money exists in several distinct layers. At the very bottom of this hierarchy—the foundation upon which the entire global financial structure is built—lies the “monetary base.”

Often referred to as “high-powered money” or “M0,” the monetary base represents the most liquid form of wealth within an economy. While it might not be the money you see in your Venmo balance or your brokerage account, its fluctuations dictate interest rates, influence inflation, and determine the lending capacity of commercial banks. Understanding the monetary base is essential for anyone looking to grasp how central banks control the pulse of the modern economy.

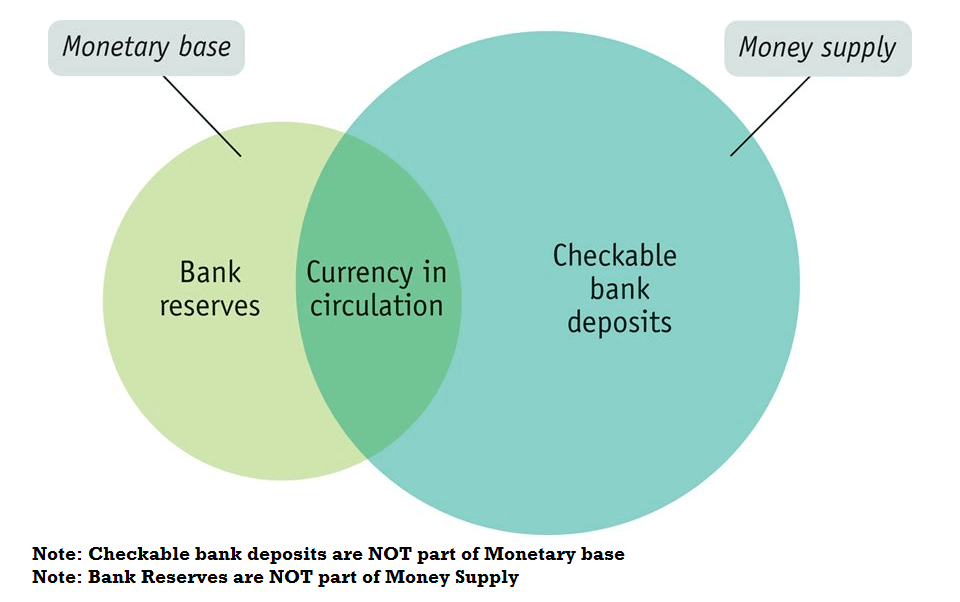

Defining the Monetary Base: The “High-Powered Money”

The monetary base is a specific measure of a country’s money supply that includes only the most liquid assets. Specifically, it consists of the total amount of a currency that is either in general circulation in the hands of the public or in the form of commercial bank deposits held in the central bank’s reserves.

The Components of the Monetary Base

To understand the monetary base, we must look at its two primary components:

- Currency in Circulation: This includes all the physical banknotes and coins held by individuals, businesses, and in bank vaults. It is the tangible “cash” that most people associate with the word money.

- Bank Reserves: This is the portion of the monetary base that the public never sees. Commercial banks are required to hold a certain amount of funds at the central bank (such as the Federal Reserve in the United States). These reserves ensure that banks have enough liquidity to settle transactions with one another and meet withdrawal demands from customers.

The Role of the Central Bank

The monetary base is unique because it is the only part of the money supply that a central bank can control directly. By engaging in “Open Market Operations”—buying or selling government bonds—the central bank can instantly increase or decrease the amount of reserves in the system. Because this “base” money can be leveraged by banks to create even more money through lending, it is frequently called “high-powered money.”

The Monetary Base vs. The Money Supply

A common point of confusion for those new to business finance is the difference between the monetary base and the broader money supply (often categorized as M1 and M2). While they are related, they represent very different functions within the financial ecosystem.

Understanding M1 and M2

The broader money supply includes the monetary base but adds several layers of “credit-based” money:

- M1: Includes the monetary base plus demand deposits (checking accounts) and other liquid instruments.

- M2: A broader category that includes M1 plus “near money,” such as savings accounts, money market funds, and certificates of deposit (CDs).

The key difference is that the monetary base consists of physical currency and central bank reserves, whereas M1 and M2 consist largely of digital accounting entries created by commercial banks when they issue loans.

The Money Multiplier Effect

The relationship between the monetary base and the broader money supply is governed by the “money multiplier.” In a fractional reserve banking system, banks are only required to keep a small fraction of their deposits as reserves. They lend out the rest.

For example, if the reserve requirement is 10%, a bank receiving a $1,000 deposit can lend out $900. That $900 is eventually deposited into another bank, which can then lend out $810. Through this cycle, a small increase in the monetary base can lead to a much larger increase in the total money supply (M2). This is why the monetary base is the “foundation”; if the foundation grows, the entire building of credit can expand.

How Central Banks Manipulate the Monetary Base

Central banks utilize the monetary base as their primary tool for conducting monetary policy. By shifting the size of the base, they can influence the cost of borrowing and the overall level of economic activity.

Open Market Operations (OMO)

The most traditional way to alter the monetary base is through the purchase and sale of securities. When the Federal Reserve wants to increase the monetary base to stimulate the economy, it buys government Treasuries from private banks. The Fed pays for these securities by electronically crediting the banks’ reserve accounts. Suddenly, the monetary base has expanded, and banks have more “high-powered money” to lend to consumers and businesses. Conversely, if the Fed sells securities, it “mops up” liquidity, shrinking the monetary base.

Quantitative Easing (QE)

In times of extreme economic crisis, such as the 2008 financial collapse or the 2020 COVID-19 pandemic, standard OMO may not be enough. Central banks then turn to Quantitative Easing. QE is essentially a massive, aggressive expansion of the monetary base. The central bank buys not just short-term government debt, but also long-term bonds and mortgage-backed securities. This floods the banking system with reserves, keeping long-term interest rates low and encouraging investment when confidence is at an all-time low.

Interest on Reserves (IOR)

Modern central banking also uses the interest rate paid on reserves to control the “velocity” of the monetary base. By raising the interest rate it pays to commercial banks for holding their money at the central bank, the Fed can encourage banks to keep their money parked rather than lending it out. This allows the central bank to maintain a large monetary base without necessarily causing immediate inflationary pressure in the broader economy.

The Impact on Inflation and the Economy

One of the most debated topics in macroeconomics is the link between the monetary base and inflation. Theoretically, if the monetary base grows too quickly, there will be “too much money chasing too few goods,” leading to a decrease in the purchasing power of the currency.

The Quantity Theory of Money

The classical view, often associated with economist Milton Friedman, suggests that inflation is “always and everywhere a monetary phenomenon.” Under this view, a direct correlation exists between the growth of the monetary base and the rate of inflation. If the monetary base doubles while the production of goods remains stagnant, prices should, in theory, double.

Why the Link Sometimes Breaks

In recent decades, however, we have seen instances where the monetary base expanded massively without immediate hyperinflation. This occurred after 2008. The reason lies in the “velocity of money”—the speed at which money changes hands. If the central bank increases the monetary base, but commercial banks are too scared to lend and consumers are too scared to spend, the money simply sits in reserve accounts. In this scenario, the broader money supply (M2) does not grow as fast as the monetary base, and inflationary pressure remains muted.

The 2020-2022 Inflationary Cycle

The post-pandemic era provided a different case study. In 2020, the monetary base was expanded at a record pace. Unlike 2008, this expansion was coupled with direct fiscal stimulus (government checks to citizens). This caused both the monetary base and the M2 money supply to skyrocket simultaneously. When supply chain disruptions met this massive surge in the money supply, global inflation reached 40-year highs, proving that while the monetary base is a tool for growth, it is also a potential catalyst for price instability.

Why Investors and Businesses Should Care

For the average person, the monetary base feels like an abstract concept. However, for those involved in personal finance, investing, and business strategy, it is a leading indicator of market conditions.

Predicting Interest Rate Trends

The monetary base is the “supply” side of the supply-and-demand equation for money. When the monetary base is expanding rapidly, it generally signals a period of low interest rates and high liquidity. This is usually a “risk-on” environment where stock markets and real estate prices rise because capital is cheap and abundant. Conversely, when a central bank begins “Quantitative Tightening” (reducing the monetary base), it is a signal that interest rates are headed higher and market volatility is likely to increase.

Managing Risk in an Inflationary Environment

Business owners must monitor the monetary base to anticipate changes in their input costs. Because the monetary base is the precursor to inflation, a sustained, aggressive expansion of the base often precedes a rise in the cost of raw materials and labor. Businesses that understand this can adjust their pricing models and supply chain contracts before the full force of inflation hits the retail market.

Asset Allocation and Wealth Preservation

For investors, the monetary base provides a roadmap for wealth preservation. In periods of extreme monetary expansion, “hard assets” like gold, real estate, and even Bitcoin often outperform fiat currency because their supply cannot be increased by a central bank’s keyboard. By tracking the growth of the monetary base relative to GDP, investors can determine whether they are in a period of currency debasement or sound monetary management.

Conclusion

The monetary base is far more than a technical banking term; it is the fundamental driver of the modern financial engine. By controlling the supply of physical currency and bank reserves, central banks exercise immense power over the global economy. While a stable and growing monetary base can facilitate trade and investment, an unmanaged or volatile base can lead to economic overheating or stagnation.

For anyone navigating the world of money—whether as an entrepreneur, an investor, or a consumer—keeping an eye on the “foundation” is the best way to understand the stability of the entire economic house. As the world shifts toward more digital forms of currency and decentralized finance, the way we define and manage the monetary base may evolve, but its role as the ultimate source of liquidity will remain unchanged.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.