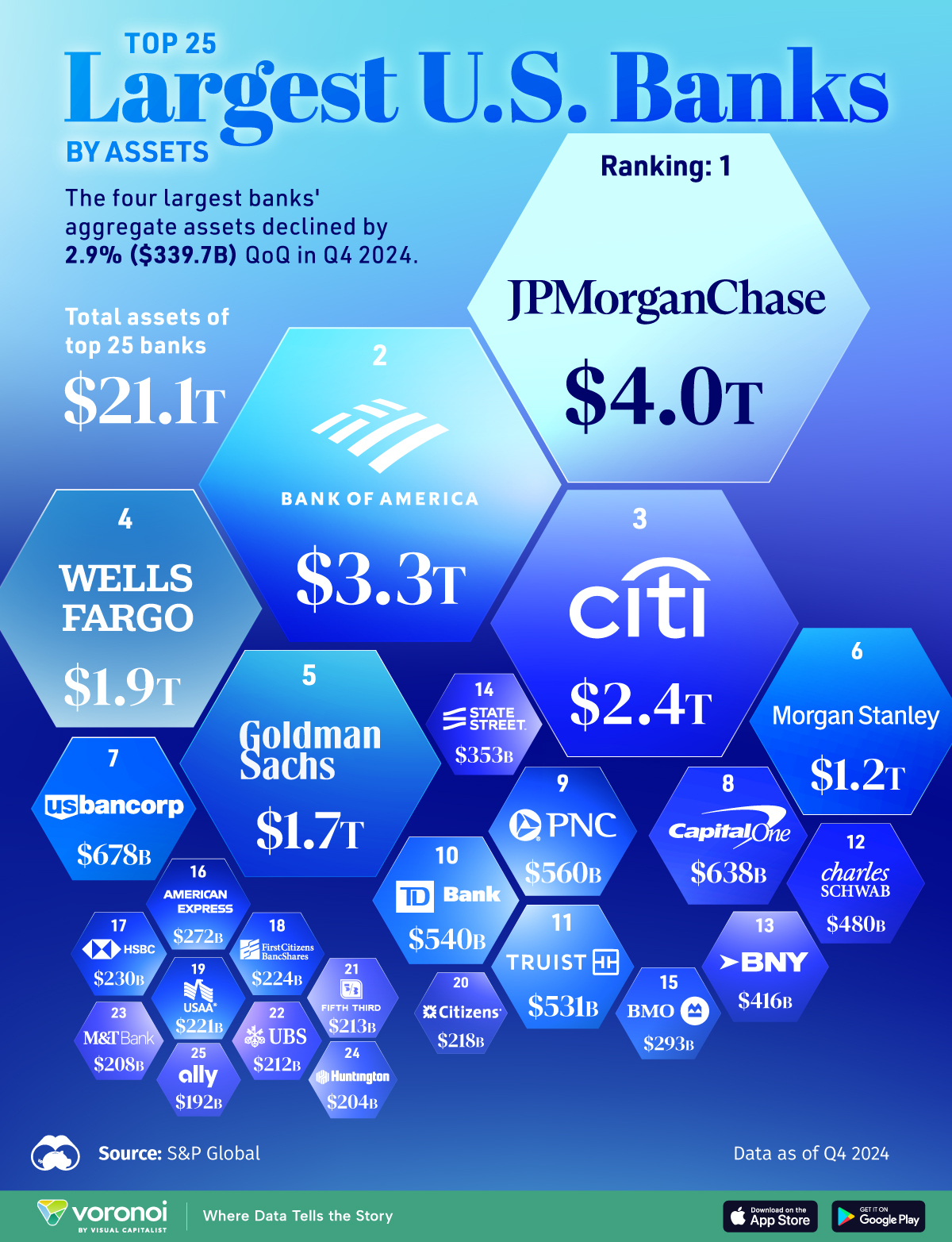

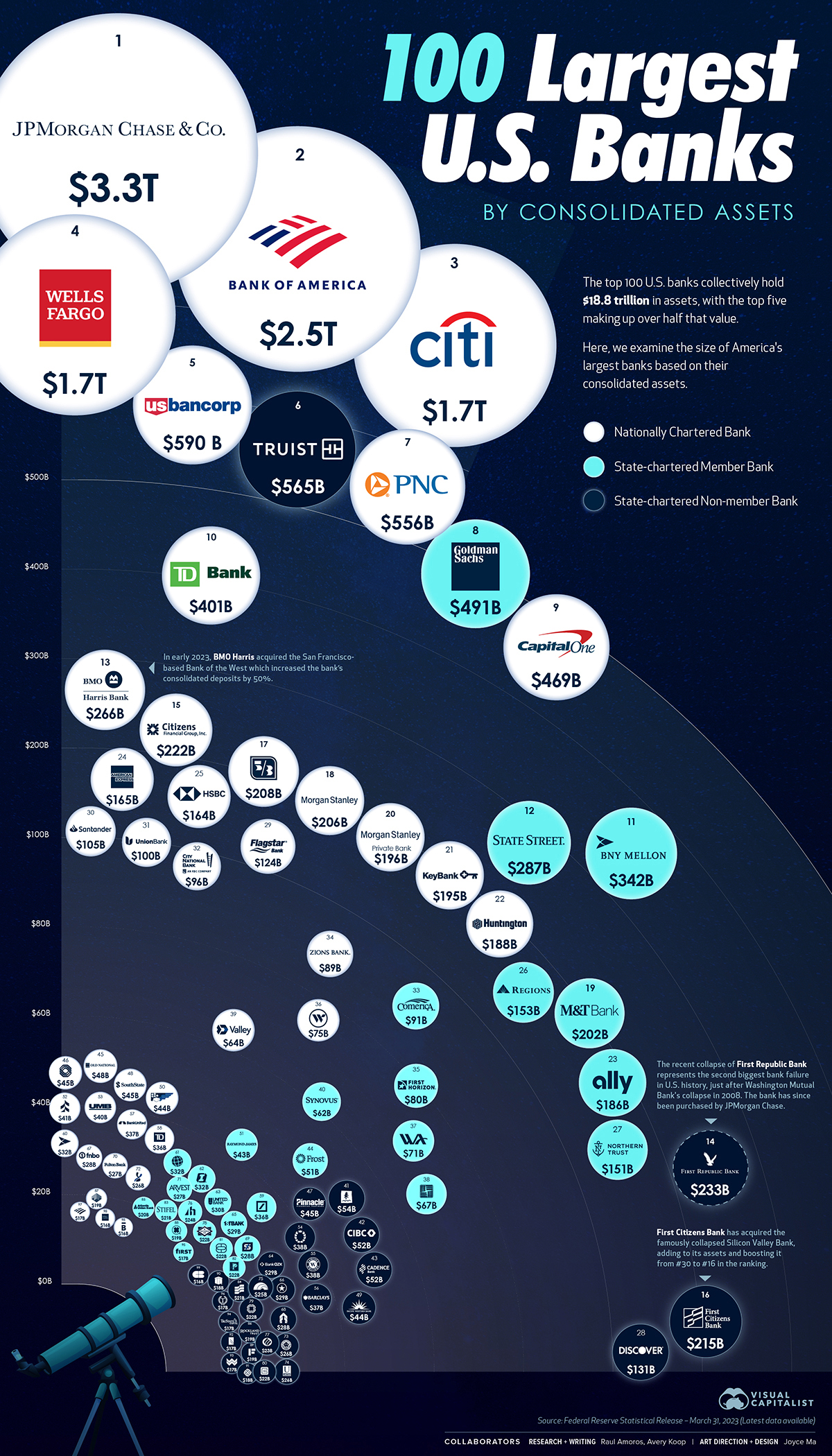

The question “what is the largest bank in the US?” is a fundamental one for anyone seeking to understand the immense scale and influence of financial institutions in the American economy. While various metrics can define “largest”—such as market capitalization, revenue, or number of customers—the most commonly accepted and significant measure is total assets. By this standard, JPMorgan Chase & Co. consistently holds the top position, a testament to its sprawling operations, strategic acquisitions, and diverse financial services.

Understanding the size and scope of institutions like JPMorgan Chase is not merely an exercise in trivia; it offers crucial insights into the stability of the financial system, the allocation of capital, and the landscape of services available to businesses and consumers alike. These behemoths play a pivotal role in everything from individual mortgage lending to complex international trade finance, profoundly impacting economic growth and stability.

JPMorgan Chase: A Colossus in the American Financial Landscape

JPMorgan Chase stands as the undisputed leader among US banks, a financial superpower whose influence permeates nearly every facet of the American and global economy. Its sheer scale is a result of centuries of strategic evolution, critical mergers, and an unwavering focus on diversification across key financial sectors.

By the Numbers: Defining “Largest”

When we declare JPMorgan Chase the largest, we primarily refer to its colossal total assets. As of various reporting periods in recent years, JPMorgan Chase’s total assets have typically hovered around or exceeded $3.5 trillion. This figure represents the sum of all its economic resources, including loans, investments, cash, and other holdings, providing a clear indicator of its financial might and capacity.

Beyond assets, other metrics reinforce its dominant position:

- Market Capitalization: Often fluctuating with market sentiment, JPMorgan Chase consistently ranks among the top banks globally by market cap, reflecting investor confidence in its future earnings potential and stability.

- Revenue and Profitability: The bank routinely reports multi-billion-dollar quarterly revenues and profits, underscoring its operational efficiency and vast income streams from its diverse business segments.

- Global Reach and Customer Base: While we focus on its US standing, JPMorgan Chase has a significant international presence, serving millions of consumers and businesses worldwide. Within the US, its customer base spans millions of households and corporations, making its footprint ubiquitous.

A Legacy of Mergers and Growth

JPMorgan Chase’s current form is the culmination of a rich and complex history of mergers, acquisitions, and organic growth that traces back to the 19th century. Its lineage includes iconic names that have shaped American finance:

- J.P. Morgan & Co.: Founded by the legendary financier J. Pierpont Morgan, this institution was instrumental in the industrialization of America and played a key role in stabilizing markets during crises.

- Chase Manhattan Corporation: A major retail and commercial bank, formed from the merger of Chase National Bank and The Bank of the Manhattan Company.

The modern JPMorgan Chase truly began to take shape with the 2000 merger of J.P. Morgan & Co. and Chase Manhattan Corporation. This fusion created a financial services giant combining investment banking prowess with a robust retail banking network. Subsequent, highly significant acquisitions further cemented its leading position:

- Bear Stearns (2008): Acquired during the height of the 2008 financial crisis, this move bolstered JPMorgan Chase’s investment banking capabilities and market share.

- Washington Mutual (2008): Another crisis-era acquisition, Washington Mutual’s collapse provided JPMorgan Chase with an immense network of retail branches and a massive deposit base, significantly expanding its consumer banking footprint.

These strategic moves, often orchestrated during periods of market turmoil, allowed JPMorgan Chase to not only survive but thrive and expand, absorbing competitors and consolidating its market power.

Diverse Business Segments Fueling Its Scale

The strength of JPMorgan Chase lies in its multi-faceted business model, which spans the entire spectrum of financial services. This diversification minimizes reliance on any single revenue stream and provides robust cross-selling opportunities. Its primary segments include:

- Consumer & Community Banking (CCB): This is the retail face of the bank, offering checking and savings accounts, mortgages, auto loans, and credit cards to millions of households and small businesses through its extensive branch network and digital platforms.

- Corporate & Investment Bank (CIB): Serving large corporations, institutions, and governments, the CIB provides investment banking services (M&A advisory, underwriting), market-making activities (trading equities, fixed income, currencies), and treasury services.

- Commercial Banking: This segment focuses on providing financial solutions to mid-sized businesses, local governments, and non-profit organizations, offering lending, treasury, and investment banking products.

- Asset & Wealth Management: Catering to high-net-worth individuals, institutional investors, and sovereign wealth funds, this division provides private banking, investment management, and retirement planning services.

This comprehensive array of services ensures that JPMorgan Chase is a central player in almost every financial transaction, from an individual depositing their paycheck to a multinational corporation raising billions in the capital markets.

The Economic and Financial Impact of Megabanks

The existence and operations of megabanks like JPMorgan Chase have profound implications for the economy, regulators, and the general public. Their sheer size bestows upon them both immense power and significant responsibilities.

Systemic Importance and “Too Big to Fail”

Megabanks are often classified as Systemically Important Financial Institutions (SIFIs), a designation that acknowledges their critical role in the global financial system. Their failure could trigger a cascading crisis, threatening the stability of the broader economy. This concept led to the controversial “Too Big to Fail” label, implying that governments might be compelled to bail out such institutions during severe distress to prevent a wider economic meltdown.

In response to the 2008 financial crisis, regulators implemented stricter oversight and capital requirements for SIFIs. These measures, such as increased capital buffers and robust stress testing, are designed to make these banks more resilient and reduce the likelihood and impact of their failure. However, the debate continues regarding whether these measures are sufficient and if the concentration of financial power in a few hands poses an inherent risk.

Influence on Monetary Policy and Markets

Megabanks are integral to the transmission of monetary policy from central banks like the Federal Reserve to the broader economy. They are primary dealers in government securities, play a massive role in interbank lending, and are key conduits for the flow of credit. Their lending decisions, investment strategies, and trading activities can significantly influence:

- Interest Rates: Their vast lending operations impact the effective interest rates offered to consumers and businesses.

- Credit Availability: As major lenders, their willingness to extend credit is crucial for economic expansion.

- Market Liquidity: Their trading desks provide essential liquidity to equity, bond, and foreign exchange markets, ensuring smooth functioning.

Their deep understanding of market dynamics and extensive data allow them to play a leading role in shaping financial trends, often influencing smaller players and the broader economic narrative.

Advantages of Scale for Consumers and Businesses

While megabanks face scrutiny, their enormous scale also brings tangible benefits:

- Extensive Network and Accessibility: JPMorgan Chase boasts a vast network of branches, ATMs, and a sophisticated digital banking presence, offering unparalleled convenience and access to financial services across the country and online.

- Broad Product Range: They can offer an incredibly diverse suite of products and services, from basic checking accounts to complex derivatives, catering to virtually any financial need for individuals or multi-national corporations.

- Technological Innovation: Their substantial resources allow them to invest heavily in technology, leading to advanced mobile banking apps, cybersecurity measures, and innovative financial tools that can improve customer experience and efficiency.

- Access to Capital: For large corporations and governments, megabanks are often the only institutions capable of underwriting massive debt or equity offerings, facilitating large-scale projects and investments critical for economic development.

- Economies of Scale: While not always translated into lower consumer prices due to other factors, their size theoretically allows for greater efficiency in operations, which can sometimes result in competitive pricing for certain products or services.

The Competitive Landscape: Other Financial Giants

While JPMorgan Chase sits atop the hierarchy, it operates within a highly competitive landscape populated by other formidable financial institutions, all vying for market share, talent, and technological supremacy.

The “Big Four” and Beyond

JPMorgan Chase is typically grouped with three other banks to form the “Big Four” in the US, based on total assets:

- Bank of America: Often a close second to JPMorgan Chase, Bank of America also boasts a massive retail presence, significant investment banking operations, and a strong wealth management division. Its assets typically range between $3 to $3.5 trillion.

- Wells Fargo: Known for its extensive retail banking network and strong presence in mortgage lending, Wells Fargo has faced significant challenges in recent years due to various scandals but remains a major player with assets around $1.7 to $2 trillion.

- Citigroup: A globally diversified financial services company, Citigroup has a strong international footprint, particularly in emerging markets, alongside significant investment banking and consumer banking operations. Its assets are generally in the $1.7 to $2 trillion range.

Beyond these giants, other important players include investment banks like Goldman Sachs and Morgan Stanley (which have expanded into wealth management and consumer lending), large regional banks (e.g., U.S. Bank, PNC Financial Services), and a multitude of smaller community banks and credit unions.

Shifting Tides: Challenges and Opportunities

The banking sector is dynamic, constantly evolving in response to economic forces, technological advancements, and changing customer expectations:

- Fintech Disruption: The rise of financial technology (fintech) companies, offering specialized services from digital payments to online lending, presents both a challenge and an opportunity. Megabanks are responding by investing in their own digital capabilities, acquiring fintech startups, and forming partnerships.

- Regulatory Environment: The post-2008 regulatory landscape, including the Dodd-Frank Act, imposed significant compliance costs and capital requirements. Future regulatory shifts, particularly concerning consumer protection and systemic risk, will continue to shape bank operations.

- Interest Rate Environment: Fluctuations in interest rates directly impact banks’ net interest income (the difference between what they earn on loans and pay on deposits), influencing profitability and lending strategies.

- Customer Expectations: Modern customers demand seamless digital experiences, personalized services, and ethical practices. Banks must adapt to these evolving demands to retain and attract clients.

- ESG Considerations: Environmental, Social, and Governance (ESG) factors are increasingly important to investors, customers, and regulators. Banks are under pressure to demonstrate their commitment to sustainability, diversity, and responsible lending practices.

Navigating the Financial World: Choosing a Bank

While understanding which institution is the “largest” provides a macroeconomic perspective, for individuals and businesses, the ideal bank might not always be the biggest. Choosing a financial partner requires assessing specific needs and priorities.

What Matters Most to You?

For consumers, key factors might include:

- Branch and ATM Access: Do you prefer in-person service, or are you comfortable with primarily digital interactions?

- Fees and Rates: What are the monthly fees, overdraft charges, and interest rates offered on savings accounts or loans?

- Digital Tools: How robust and user-friendly is their mobile app and online banking platform?

- Customer Service: Is their support responsive and helpful?

- Product Range: Do they offer all the services you anticipate needing, from checking to mortgages to investment options?

For businesses, considerations often revolve around:

- Lending Capabilities: Can the bank meet your financing needs, whether for working capital, equipment, or expansion?

- Treasury Services: Do they offer efficient cash management, payment processing, and international banking solutions?

- Industry Expertise: Does the bank have a dedicated team or specific expertise in your industry?

- Relationship Management: Is there a dedicated point of contact who understands your business needs?

Beyond Size: Regional Banks and Credit Unions

While megabanks offer unparalleled scale and breadth, smaller institutions often excel in different areas:

- Regional and Community Banks: These banks typically focus on specific geographic areas, fostering stronger ties with local businesses and communities. They may offer more personalized service and a deeper understanding of local economic conditions.

- Credit Unions: Member-owned financial cooperatives, credit unions often offer lower fees, better interest rates on deposits, and more favorable loan terms because they operate on a not-for-profit basis. They are known for excellent customer service and community focus.

Choosing a smaller bank or credit union might be advantageous if personalized service, local decision-making, or specific community values are high on your priority list, even if their product range or digital offerings are less extensive than a megabank.

In conclusion, JPMorgan Chase & Co. unequivocally stands as the largest bank in the US by total assets, a testament to its strategic growth, diverse operations, and critical role in the global financial system. Its dominance highlights the multifaceted impact of megabanks on the economy, from systemic stability to daily consumer finance. However, the dynamic financial landscape continues to evolve, presenting both challenges and opportunities for all financial institutions, ensuring that the question of “largest” remains a key point of discussion in the ever-important world of money.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.