In the dynamic world of real estate and mortgage financing, the term “jumbo loan” frequently surfaces, often associated with luxury properties and substantial borrowing needs. For many prospective homebuyers, particularly those eyeing properties in high-cost areas, understanding what constitutes a jumbo loan and, crucially, what its limits are, is a fundamental step in navigating their financial journey. Far from being a niche product, jumbo loans represent a significant segment of the mortgage market, catering to a specific borrower demographic and a unique set of financial parameters. This article will delve deep into the intricacies of jumbo loans, exploring their definition, how limits are established, the pros and cons of opting for one, and the essential steps to secure this distinct type of financing.

Understanding the Landscape of Mortgage Lending

To truly grasp the concept of a jumbo loan, it’s vital to first understand the broader framework of mortgage lending in the United States. The market is primarily bifurcated into conforming and non-conforming loans, a distinction that forms the bedrock of how mortgage products are designed, priced, and underwritten.

Conforming vs. Non-Conforming Loans

At the heart of mortgage finance lies the conforming loan. These are mortgages that meet specific criteria set by government-sponsored enterprises (GSEs), namely Fannie Mae and Freddie Mac. These criteria include loan amount limits, borrower credit standards, and property types. By adhering to these standards, conforming loans can be purchased by Fannie Mae and Freddie Mac from lenders, injecting liquidity into the market and making mortgages more accessible and affordable. This ability to sell mortgages allows lenders to free up capital to issue new loans, creating a robust and continuous lending cycle.

Conversely, non-conforming loans are those that do not meet the guidelines of Fannie Mae and Freddie Mac. Jumbo loans are the most prominent type of non-conforming loan. They are non-conforming specifically because their loan amounts exceed the limits set for conforming loans. While conforming loans are standardized and relatively straightforward, non-conforming loans, like jumbo mortgages, require a different approach to underwriting and risk assessment by lenders.

The Role of Fannie Mae and Freddie Mac

Fannie Mae (Federal National Mortgage Association) and Freddie Mac (Federal Home Loan Mortgage Corporation) are pivotal institutions in the U.S. housing market. They do not directly lend money to consumers but rather buy mortgages from primary lenders, package them into mortgage-backed securities, and sell them to investors. This secondary market activity ensures a steady flow of capital for mortgage lending. The loan limits they establish for conforming mortgages are not arbitrary; they are typically based on the average home price in the U.S., with provisions for higher limits in areas with higher median home values. These limits are reviewed and adjusted annually by the Federal Housing Finance Agency (FHFA), which oversees both Fannie Mae and Freddie Mac.

Why Loan Limits Matter

Loan limits are more than just numerical thresholds; they have profound implications for borrowers and the housing market. For borrowers, they dictate which type of mortgage they might qualify for and, consequently, the associated interest rates, down payment requirements, and underwriting standards. If a borrower needs to finance a home purchase that exceeds the conforming loan limit for their area, they automatically enter the realm of jumbo loans. For lenders, these limits influence their risk exposure, portfolio management strategies, and the availability of capital. The distinction ensures that lenders appropriately price the risk associated with larger loans that cannot be easily sold to the GSEs.

Defining the Jumbo Loan and Its Limits

With the foundational understanding established, we can now zero in on the core subject: what exactly is a jumbo loan and how are its limits determined?

How Jumbo Loan Limits are Determined

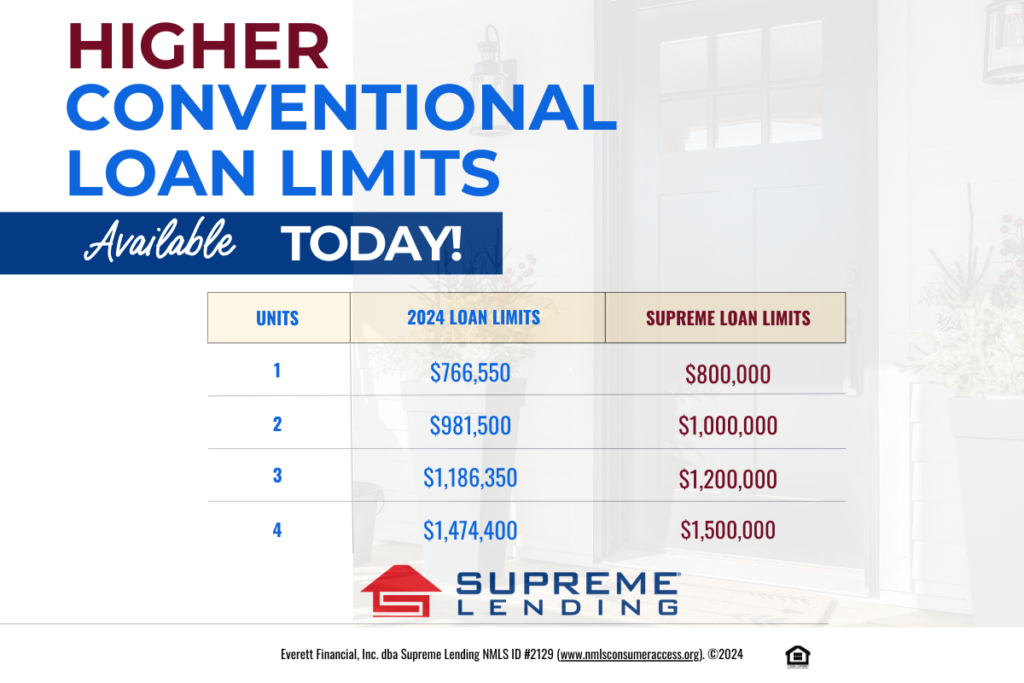

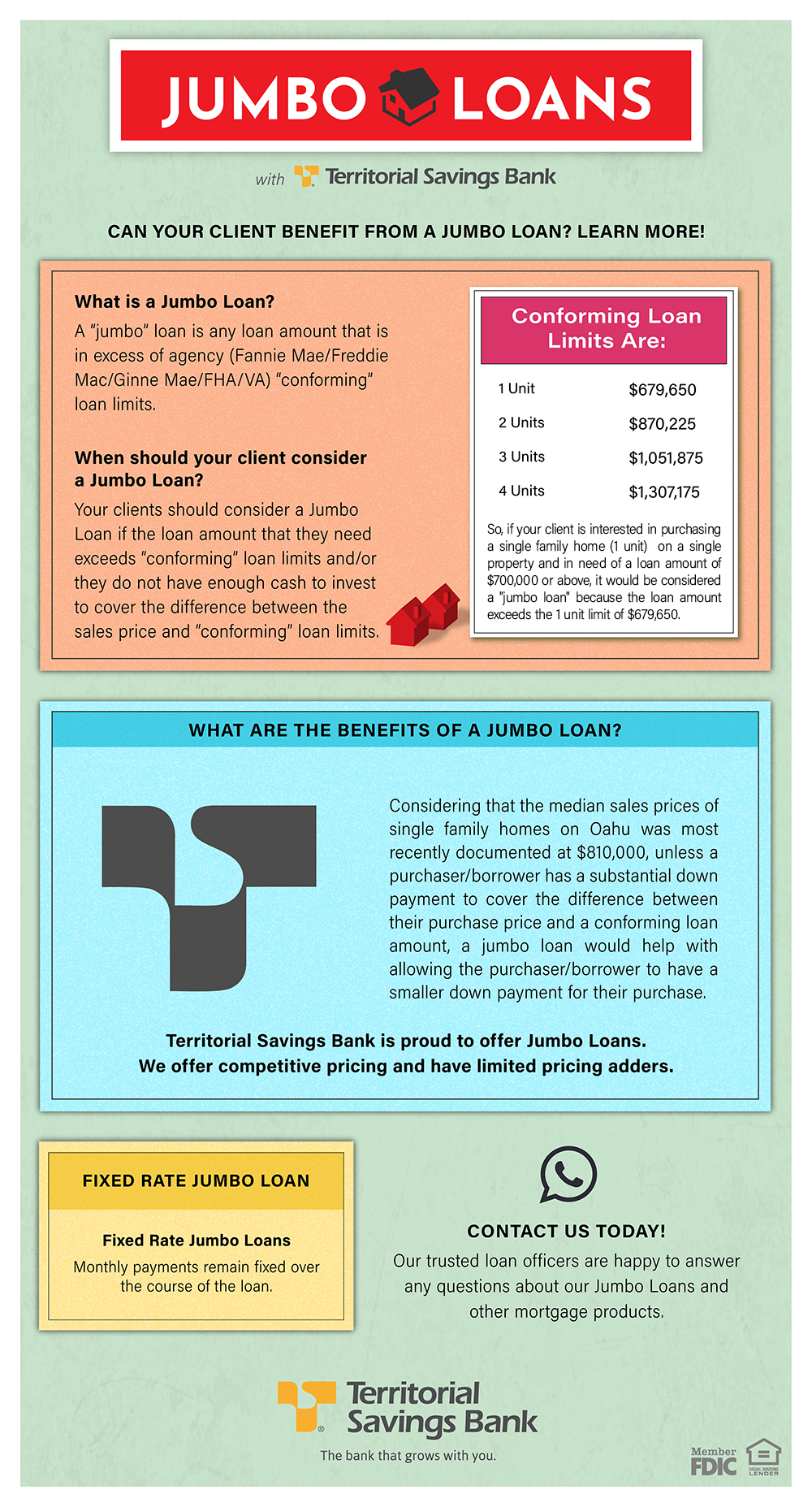

A jumbo loan is, by definition, any mortgage loan that exceeds the conforming loan limits set by the Federal Housing Finance Agency (FHFA) for Fannie Mae and Freddie Mac. For most of the United States, the baseline conforming loan limit is adjusted annually to reflect changes in the average U.S. home price. For 2024, the baseline conforming loan limit for a single-unit property in most of the U.S. is $766,550. Any loan amount above this figure in a standard area would be considered a jumbo loan.

However, it’s crucial to understand that this limit is not universally applied. The FHFA also establishes higher conforming loan limits for certain high-cost areas where 115% of the local median home value exceeds the baseline limit. These areas often include major metropolitan centers and popular coastal regions where housing costs are significantly above the national average. In the most expensive areas, the maximum conforming loan limit for a single-unit property can be up to $1,149,825 for 2024 (150% of the baseline limit). Only loans exceeding these higher local limits would be considered jumbo loans in those specific geographies.

Geographic Variations in Limits

The geographic variation is a critical aspect of jumbo loan limits. What might be a conforming loan in an expensive coastal city like San Francisco or New York could easily be a jumbo loan in a more affordable Midwestern city. For instance, if the conforming loan limit in a particular high-cost county is $1,000,000, a $900,000 mortgage would still be a conforming loan. However, in a county with the standard $766,550 limit, that same $900,000 mortgage would be a jumbo loan.

These limits are also influenced by the number of units in a property. Duplexes, triplexes, and four-plexes have higher conforming loan limits than single-unit homes, reflecting the increased value and potential rental income. For example, the conforming loan limit for a two-unit property is higher than for a single-unit property, and so on, up to four units.

The Impact of the FHFA

The Federal Housing Finance Agency (FHFA) plays the central role in establishing these limits. Each year, typically in November or December, the FHFA announces the new conforming loan limits for the upcoming year. This annual adjustment is based on a formula mandated by the Housing and Economic Recovery Act of 2008 (HERA), which ties the baseline limit to the percentage change in the average U.S. home price. This ensures that the limits remain relevant and responsive to market conditions, although sometimes with a slight lag. The FHFA’s decisions directly impact the accessibility of mortgages, the pricing of various loan products, and the overall liquidity of the housing market.

Advantages and Disadvantages of Jumbo Loans

Like any financial product, jumbo loans come with their own set of benefits and drawbacks. Understanding these can help potential borrowers make informed decisions.

Benefits: Higher Loan Amounts, Potentially Competitive Rates

The most obvious advantage of a jumbo loan is its ability to finance high-value properties that exceed conforming loan limits. Without jumbo loans, individuals looking to purchase expensive homes would be severely limited in their financing options. For well-qualified borrowers, jumbo loans can sometimes offer surprisingly competitive interest rates, especially in a low-rate environment. Lenders often vie for these high-net-worth clients, leading to attractive pricing for those with impeccable credit and substantial assets. Furthermore, a single jumbo loan can simplify the financing process for an expensive home, as opposed to potentially requiring multiple smaller loans or a significant cash outlay.

Challenges: Stricter Qualification, Larger Down Payments, Higher Closing Costs

The primary challenges of jumbo loans stem from their higher risk profile for lenders, given that they cannot be sold to Fannie Mae or Freddie Mac. Consequently, lenders hold these loans on their books, requiring them to implement stricter underwriting standards.

- Stricter Qualification: Borrowers typically need an excellent credit score (often 700 or higher, with 740+ being preferred), a low debt-to-income (DTI) ratio (usually below 38-43%), and significant liquid financial reserves (often 6-12 months of mortgage payments, or even more for very large loans).

- Larger Down Payments: While some conforming loans might allow for down payments as low as 3-5%, jumbo loans generally require a larger down payment, often 10-20% or even 25% for the highest loan amounts. This is to reduce the lender’s loan-to-value (LTV) risk.

- Higher Closing Costs: Given the larger loan amounts, closing costs—which are often a percentage of the loan—will naturally be higher in absolute terms. Appraisal fees can also be higher, and some lenders might require two appraisals for very large properties.

- Increased Documentation: Lenders often demand more extensive documentation to verify income, assets, and overall financial stability, including multiple years of tax returns, detailed bank statements, and investment account summaries.

Risk Assessment for Lenders and Borrowers

For lenders, jumbo loans carry increased risk because they lack the liquidity and government backing associated with conforming loans. If a jumbo loan defaults, the lender bears the full brunt of the loss. This is why their underwriting is so rigorous. For borrowers, while a jumbo loan enables the purchase of a high-value property, it also entails a substantial financial commitment. The larger monthly payments, coupled with potentially higher property taxes and insurance on expensive homes, mean borrowers must be absolutely confident in their long-term financial stability. A thorough personal risk assessment is as crucial for the borrower as the lender’s assessment.

Navigating the Jumbo Loan Application Process

Applying for a jumbo loan is a comprehensive process that demands meticulous preparation and attention to detail. Success hinges on demonstrating a robust financial profile and clear repayment capacity.

Key Eligibility Requirements (Credit Score, Debt-to-Income, Reserves)

Lenders scrutinize several key metrics when evaluating jumbo loan applications:

- Exceptional Credit Score: A FICO score typically in the mid-700s or higher is paramount. This indicates a strong history of responsible borrowing and repayment.

- Low Debt-to-Income (DTI) Ratio: Your DTI ratio, which compares your total monthly debt payments to your gross monthly income, needs to be low, often below 38% to 43%. Lenders want to see that you have ample disposable income to comfortably manage the large mortgage payment.

- Significant Liquid Financial Reserves: This is a crucial differentiator for jumbo loans. Lenders typically require borrowers to have several months (often 6 to 12 months, or even more) of mortgage payments (principal, interest, taxes, and insurance – PITI) in readily accessible accounts after the down payment and closing costs have been paid. These reserves act as a financial cushion, assuring the lender of your ability to make payments even if your income stream experiences a temporary disruption.

- Stable Income and Employment History: Lenders will look for a consistent and verifiable income stream, often requiring at least two years of stable employment or self-employment history in the same field.

Documentation Needed for Jumbo Loan Approval

The documentation required for a jumbo loan is extensive and designed to provide a comprehensive picture of your financial health. Expect to provide:

- Income Verification: W-2 forms for the past two years, recent pay stubs (typically 30-60 days), and if self-employed, two years of personal and business tax returns, along with profit and loss statements.

- Asset Verification: Statements for all checking, savings, investment, and retirement accounts (typically 2-3 months). Lenders want to see not only the quantity of assets but also the source of funds for your down payment and reserves.

- Credit History: Lenders will pull a comprehensive credit report, but it’s wise for you to review your own report beforehand to address any inaccuracies.

- Property Information: Details about the property you intend to purchase, including the purchase agreement, and potentially two appraisals will be required.

- Other Debt Obligations: Statements for all existing loans, credit cards, and other financial commitments.

Strategies for a Successful Application

To maximize your chances of approval, consider these strategies:

- Improve Your Credit Score: Pay down debts, avoid opening new lines of credit, and address any credit report errors.

- Boost Your Reserves: Save aggressively to accumulate more liquid assets than the minimum required. The more reserves you have, the more confident lenders will be.

- Reduce Debt: Pay off high-interest debts to lower your DTI ratio.

- Maintain Stable Employment: Avoid job changes during the application process, if possible.

- Get Pre-Approved: Obtain a pre-approval letter specifically for a jumbo loan. This demonstrates to sellers that you are a serious and qualified buyer.

- Work with an Experienced Lender: Seek out lenders and mortgage brokers who specialize in jumbo loans and have a strong track record. Their expertise can be invaluable in navigating the complexities.

Is a Jumbo Loan Right for You?

The decision to pursue a jumbo loan is a significant financial one. It requires careful consideration of your personal financial situation, risk tolerance, and long-term goals.

Assessing Your Financial Readiness

Before committing to a jumbo loan, conduct a thorough self-assessment. Can you comfortably afford the larger monthly payments, property taxes, insurance, and potential maintenance costs associated with a high-value home? Do you have a stable and secure income that can withstand potential economic fluctuations? Are your financial reserves robust enough to cover unexpected expenses or periods of reduced income? Remember that tying up a significant portion of your net worth in a single asset, even a valuable one, requires careful planning. Consider your overall financial portfolio and whether a large mortgage aligns with your investment strategies.

Exploring Alternatives to Jumbo Loans

While jumbo loans are often the go-to for high-value properties, alternatives might exist, depending on your specific needs:

- Piggyback Mortgages (80/10/10 or 80/15/5): This involves taking out a conforming first mortgage for 80% of the home’s value, a second mortgage (often a home equity line of credit or HELOC) for 10-15%, and making a 5-10% down payment. This strategy allows you to avoid a jumbo loan altogether by keeping the first mortgage conforming. However, it means managing two loan payments and potentially higher interest rates on the second mortgage.

- Cash-Out Refinance on Existing Property: If you already own a substantial amount of equity in another home, a cash-out refinance could provide the funds needed for a larger down payment on your new home, potentially bringing the new mortgage amount down to conforming limits.

- Saving a Larger Down Payment: If time permits, saving an even larger down payment can reduce your loan amount, possibly pushing it below jumbo thresholds or at least making the jumbo loan more manageable.

Seeking Professional Financial Advice

Given the complexities and significant financial implications of a jumbo loan, consulting with a qualified financial advisor is highly recommended. A financial advisor can help you:

- Evaluate your overall financial health and long-term goals.

- Analyze the impact of a large mortgage on your net worth and cash flow.

- Compare various financing options, including jumbo loans and their alternatives.

- Develop a comprehensive financial plan that incorporates your housing goals.

Their objective perspective can provide invaluable insights and help you make a decision that is both financially sound and aligned with your personal circumstances.

In conclusion, understanding “what is the jumbo loan limit” is more than knowing a numerical threshold; it’s about comprehending a critical segment of the mortgage market. Jumbo loans open doors to high-value properties but demand a strong financial foundation and meticulous preparation. By carefully assessing your readiness, exploring all options, and leveraging expert advice, you can confidently navigate the path to financing your dream home, regardless of its price tag.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.