Inflation is often described as the “silent thief” of the financial world. While it may seem like a distant economic concept reserved for academic textbooks and central bank press releases, its impact is felt every time you swipe your credit card, pay your rent, or look at your retirement account balance. At its core, inflation is the rate at which the general level of prices for goods and services is rising, and, consequently, the rate at which the purchasing power of your currency is falling.

For anyone focused on personal finance, investing, or business management, understanding the mechanics of inflation is not just a matter of intellectual curiosity—it is a fundamental requirement for financial survival. If your money is sitting in a traditional savings account earning 0.1% interest while inflation is running at 4%, you are effectively losing 3.9% of your wealth every single year. This guide explores the depths of inflation, how it is measured, its impact on your financial life, and the strategies you can employ to ensure your wealth grows even when prices rise.

The Mechanics of Inflation: Why Prices Rise

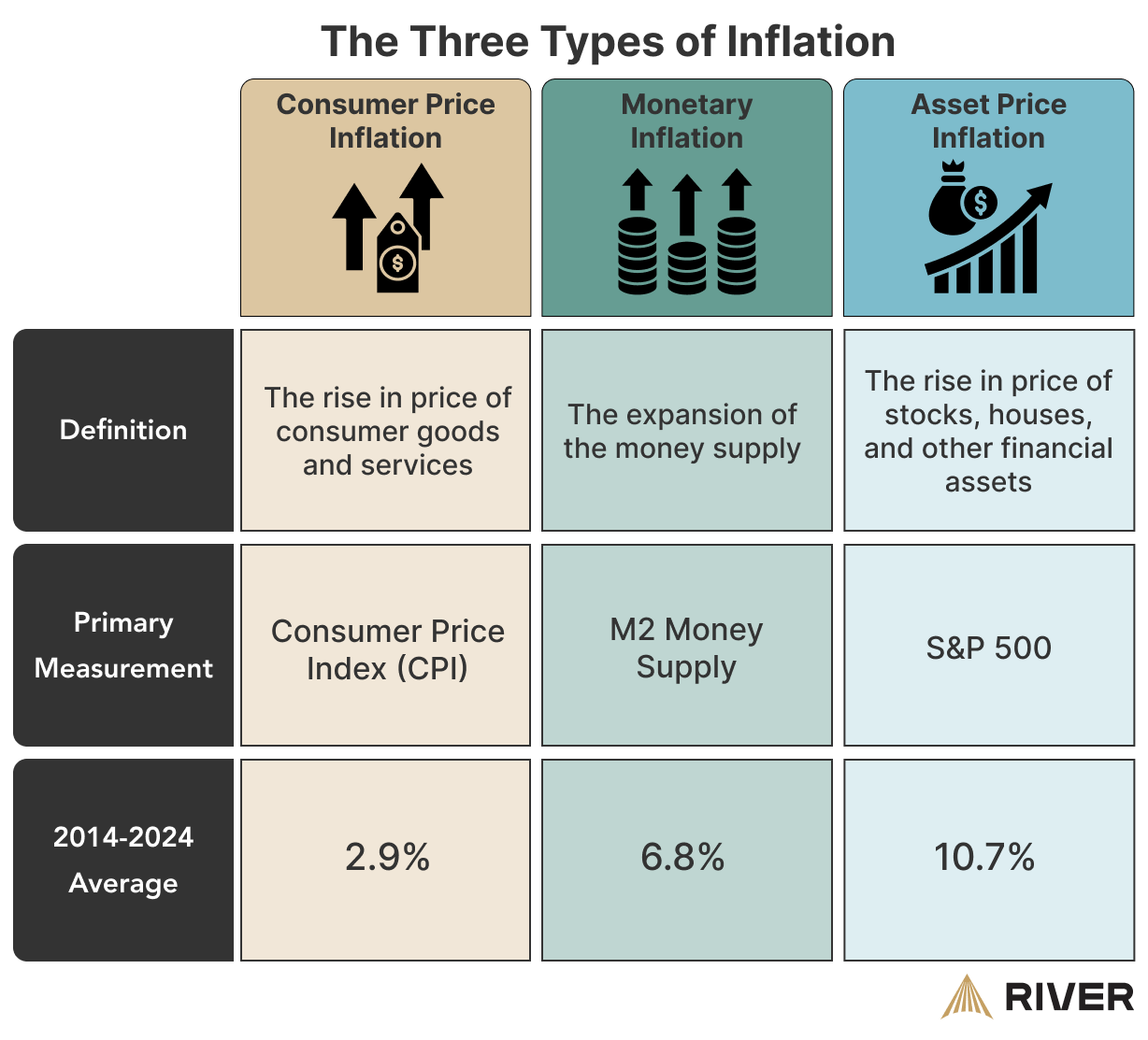

To navigate a world of shifting prices, one must first understand what drives the phenomenon. Inflation is rarely the result of a single factor; rather, it is a complex interplay between supply, demand, and monetary policy. Economists generally categorize inflation into three distinct types, each driven by different market forces.

Demand-Pull Inflation

Demand-pull inflation occurs when the demand for goods and services exceeds the economy’s capacity to produce them. Think of it as “too much money chasing too few goods.” This often happens during periods of strong economic growth. When unemployment is low and consumers feel confident, they spend more. If factories and service providers cannot keep up with this surge in orders, they raise prices to manage demand and maximize profit.

Cost-Push Inflation

Cost-push inflation is driven by the supply side of the economy. This occurs when the costs of production increase, forcing companies to pass those costs on to consumers to maintain their profit margins. A classic example is a spike in oil prices. Because energy is a fundamental input for almost every product—from the plastic in a toy to the fuel required to ship a loaf of bread—an increase in energy costs creates a ripple effect throughout the entire economy, driving up prices across the board.

Built-in Inflation

Built-in inflation, also known as the “wage-price spiral,” is linked to adaptive expectations. As prices for goods and services rise, workers begin to expect that inflation will continue in the future. Consequently, they demand higher wages to maintain their standard of living. Employers, in turn, raise the prices of their products to cover the increased labor costs. This creates a self-reinforcing loop that can be difficult to break once it becomes embedded in the public psyche.

How Inflation is Measured: Understanding the Metrics

In the world of money and finance, data is king. To make informed decisions, investors and policymakers rely on specific indices that track how prices change over time. Understanding these metrics allows you to interpret economic news and adjust your financial strategy accordingly.

The Consumer Price Index (CPI)

The Consumer Price Index (CPI) is the most widely recognized measure of inflation. It tracks the change in prices paid by urban consumers for a representative “basket” of goods and services. This basket includes everything from food and beverages to housing, apparel, transportation, and medical care. When you hear in the news that “inflation is at 5%,” the reporter is usually referring to the year-over-year change in the CPI. For the individual, the CPI is the most accurate reflection of how your daily cost of living is changing.

The Producer Price Index (PPI)

While the CPI measures the prices paid by consumers, the Producer Price Index (PPI) measures the average change over time in the selling prices received by domestic producers. It looks at the costs from the perspective of the business. The PPI is often considered a “leading indicator” of inflation. If the costs of raw materials and wholesale goods rise for businesses (PPI), those increases are likely to be passed on to the consumer (CPI) in the coming months.

The Personal Consumption Expenditures (PCE) Index

The PCE index is the Federal Reserve’s preferred measure of inflation. While similar to the CPI, it uses a different formula that accounts for “substitution.” For example, if the price of beef rises significantly, the PCE assumes consumers might buy more chicken instead. This makes the PCE a slightly more flexible and comprehensive view of how people are actually spending their money in a dynamic economy.

The Impact on Personal Finance and Purchasing Power

The primary danger of inflation is the erosion of purchasing power. If you have $100 today and inflation is at 10%, that same $100 will only buy $90 worth of goods next year. For those focused on building long-term wealth, inflation represents a significant hurdle that must be overcome through strategic financial planning.

The Erosion of Cash Savings

Cash is the asset most vulnerable to inflation. While having an emergency fund in a liquid savings account is essential for financial security, keeping excessive amounts of wealth in cash can be a recipe for financial stagnation. In an inflationary environment, the “real” return on your savings—the interest rate minus the inflation rate—is often negative. To protect your wealth, you must look beyond the mattress and the basic savings account toward assets that have the potential to appreciate.

Debt Management in High-Inflation Environments

Interestingly, inflation is not bad for everyone. It can actually benefit those who hold fixed-rate debt. If you have a 30-year fixed-rate mortgage at 3% and inflation rises to 6%, you are essentially paying back your loan with “cheaper” dollars. The value of the debt stays the same in nominal terms, but as your wages (ideally) rise with inflation, the debt becomes a smaller percentage of your income. This is why some investors use “good debt” strategically as a hedge against currency devaluation.

The Real Value of Wages

For the average worker, the most critical aspect of inflation is whether wage growth is keeping pace with the cost of living. If your salary increases by 3% but inflation is 5%, you have effectively taken a 2% pay cut. Professional career management in an inflationary era requires proactive negotiation and a focus on high-demand skills that allow you to command higher compensation as the market shifts.

Strategic Investing to Outpace Inflation

To grow wealth, your investment returns must exceed the rate of inflation. This requires a shift from a “saving” mindset to an “investing” mindset. Certain asset classes have historically performed well during periods of rising prices, acting as a “hedge” that protects your capital.

Equities and Growth Stocks

Historically, the stock market has been one of the most effective tools for beating inflation over the long term. Companies have the ability to raise their prices to offset rising costs, which can lead to higher earnings. However, not all stocks are created equal. Companies with strong “pricing power”—those that can raise prices without losing customers—are the best performers. These are typically businesses with strong brands or essential services that consumers cannot easily forgo.

Real Estate and Tangible Assets

Real estate is a classic inflation hedge. As the cost of building materials and labor increases, the value of existing properties tends to rise. Furthermore, landlords can often increase rents during inflationary periods, providing an income stream that adjusts with the market. Other tangible assets, such as commodities (gold, silver, oil) and even collectibles, often see price appreciation when the value of paper currency declines.

Treasury Inflation-Protected Securities (TIPS)

For the more conservative investor, the government offers specialized financial tools designed specifically to combat inflation. TIPS are a type of Treasury bond where the principal value increases with inflation and decreases with deflation, as measured by the CPI. When the bond matures, you are paid the adjusted principal or the original principal, whichever is greater. This ensures that your investment keeps up with the cost of living, providing a “floor” for your purchasing power.

The Role of Central Banks and Monetary Policy

Understanding the macro-finance environment is essential for any serious investor or business owner. Central banks, such as the Federal Reserve in the United States, have a “dual mandate”: to promote maximum employment and maintain stable prices. Their primary tool for controlling inflation is the adjustment of interest rates.

Interest Rate Adjustments

When inflation is too high, central banks typically raise interest rates. This makes borrowing more expensive for consumers and businesses, which cools off spending and slows down the economy. Conversely, when inflation is too low or the economy is in a recession, central banks lower rates to encourage borrowing and investment. As an investor, tracking these interest rate cycles is vital, as they dictate the “cost of money” and influence the valuation of everything from stocks to real estate.

Quantitative Easing vs. Tightening

In extreme cases, central banks use more direct methods to influence the money supply. Quantitative Easing (QE) involves the central bank buying government bonds to inject liquidity into the financial system, which can stimulate growth but also carries the risk of fueling future inflation. Quantitative Tightening (QT) is the reverse process, where the bank reduces its holdings to pull money out of the system. Monitoring these shifts in the “monetary base” provides a high-level view of where the economy is headed.

Conclusion: Building Financial Resilience

Inflation is an inevitable part of the modern economic landscape. While it can be a threat to the unprepared, it also presents opportunities for those who understand how money works. By shifting your focus from nominal gains (the number on the screen) to real gains (what that money can actually buy), you can build a robust financial strategy.

Building wealth in an inflationary world requires a diversified approach: maintaining a strategic level of debt, investing in productive assets like equities and real estate, and staying informed about the metrics that define the value of your currency. Ultimately, the goal is not just to survive inflation, but to position your finances so that you can thrive, regardless of the direction of the Consumer Price Index. Knowledge, in this case, is the ultimate hedge.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.