For millions of aspiring homeowners and those looking to refinance, the question of “what is the home mortgage rate today?” is more than just a passing curiosity – it’s a critical determinant of financial feasibility and long-term security. Mortgage rates, though seemingly abstract numbers, directly translate into the affordability of monthly payments and the total cost of homeownership over decades. Understanding these rates is paramount, not just for locking in a good deal, but for making informed decisions in one of life’s largest financial commitments.

Today’s mortgage market is a dynamic ecosystem, constantly influenced by a complex interplay of global economics, domestic policy, and market sentiment. Unlike a static price tag, mortgage rates fluctuate daily, sometimes hourly, responding to shifts in the bond market, inflation data, employment figures, and the pronouncements of central banks. This article delves into the intricate mechanisms that drive mortgage rates, provides insights into the current landscape, and offers practical strategies for navigating this vital aspect of personal finance, all while staying firmly within the realm of money and financial decision-making.

Understanding the Dynamics of Mortgage Rates

To truly grasp “what is the home mortgage rate today,” one must look beyond the quoted number and understand the powerful forces that shape it. Mortgage rates are not set by a single entity but are a reflection of broader economic conditions and the supply and demand for money.

The Federal Reserve’s Influence

While the Federal Reserve (the Fed) does not directly set mortgage rates, its monetary policy decisions exert a significant indirect influence. The Fed’s primary tool is the federal funds rate, an overnight lending rate between banks. When the Fed raises this rate, it signals a tighter monetary policy, making it more expensive for banks to borrow money, which can trickle down to higher lending rates for consumers, including mortgages. Conversely, a cut in the federal funds rate aims to stimulate economic activity by making borrowing cheaper. However, mortgage rates are more closely tied to longer-term interest rates, particularly the yield on the 10-year Treasury bond, rather than the short-term federal funds rate. Yet, the Fed’s stance on inflation and economic growth heavily influences investor sentiment towards these bonds.

Inflation and Economic Indicators

Inflation is a primary antagonist to low mortgage rates. Lenders need to ensure that the money they lend today will retain its purchasing power when repaid in the future. If inflation is high, the real value of future repayments diminishes, prompting lenders to demand a higher interest rate to compensate for this loss. Consequently, strong inflation reports often lead to an increase in mortgage rates.

Beyond inflation, a host of economic indicators play a crucial role. Robust job growth, for instance, signals a healthy economy, which can sometimes lead to higher rates as the market anticipates potential inflation or a Fed response. Conversely, signs of economic slowdown or recession can sometimes push rates down, as investors flock to the safety of government bonds, driving down their yields and, by extension, mortgage rates. Consumer confidence, manufacturing data, and even global geopolitical events can all contribute to the daily fluctuations seen in the mortgage market.

Bond Market Fluctuations

The most direct daily influence on mortgage rates comes from the bond market, specifically the market for Mortgage-Backed Securities (MBS) and the 10-year Treasury yield. Most fixed-rate mortgages are priced off the secondary market where these securities are bought and sold. When demand for MBS and Treasury bonds is high, their prices go up, and their yields (which move inversely to price) go down. Lower yields generally translate to lower mortgage rates for consumers. Conversely, when investors sell off bonds, their prices fall, yields rise, and mortgage rates tend to follow suit. This is why financial news outlets often reference the 10-year Treasury yield as a bellwether for where mortgage rates are headed. Investor confidence, perceptions of risk, and the broader economic outlook all contribute to the bond market’s daily ebb and flow.

Current Landscape: What Borrowers Need to Know

Knowing the underlying forces is one thing; understanding the practical implications for today’s borrowers is another. The current market is a kaleidoscope of options, each with its own advantages and disadvantages, and individual circumstances play a huge role in determining the actual rate offered.

Average Rates for Popular Mortgage Types

While providing a real-time, exact rate here is impossible due to daily fluctuations, it’s crucial to understand the general trends and differences between common mortgage products.

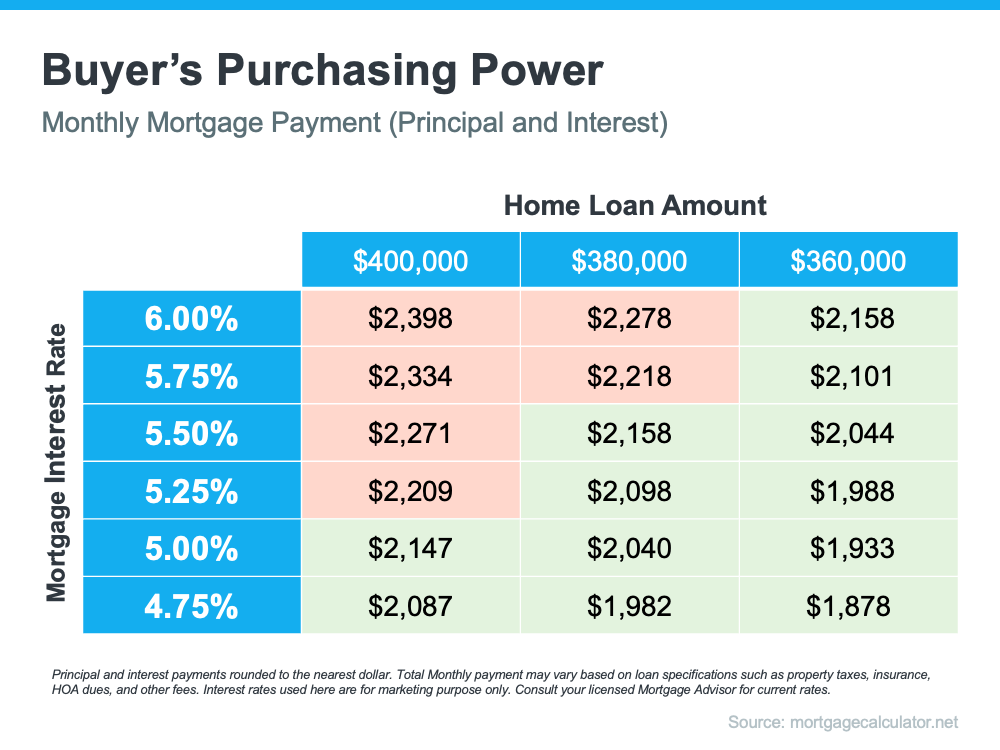

- 30-Year Fixed-Rate Mortgage: This is the most popular choice, offering stable monthly payments over three decades. Rates for 30-year fixed mortgages are generally higher than shorter-term options but provide predictability and lower monthly payments, making homeownership more accessible.

- 15-Year Fixed-Rate Mortgage: Offering a quicker path to ownership and significantly less interest paid over the life of the loan, the 15-year fixed rate typically comes with a lower interest rate than its 30-year counterpart. However, the monthly payments are substantially higher, requiring a greater financial commitment.

- Adjustable-Rate Mortgages (ARMs): ARMs offer an initial period (e.g., 3/1, 5/1, 7/1, 10/1) with a fixed, often lower, interest rate. After this period, the rate adjusts periodically based on a predetermined index plus a margin. While they can offer lower initial payments, the risk of future rate increases makes them suitable for borrowers who anticipate moving before the adjustment period or those comfortable with potential payment volatility.

Borrowers should consult reputable financial news sources, mortgage lenders, and rate comparison websites for the most up-to-the-minute average rates. These averages serve as a benchmark but are not necessarily the rate an individual will receive.

Factors Affecting Your Individual Rate

The advertised “average” rate is a starting point. Your personal financial profile significantly influences the actual rate a lender offers you.

- Credit Score: A strong credit score (typically FICO scores above 740-760) signals to lenders that you are a low-risk borrower, making you eligible for the most competitive rates. Lower scores will result in higher interest rates as lenders price in the increased risk.

- Down Payment: A larger down payment reduces the loan-to-value (LTV) ratio, signaling less risk for the lender. Borrowers with significant down payments (e.g., 20% or more) often qualify for better rates and avoid Private Mortgage Insurance (PMI).

- Loan Type: Government-backed loans (FHA, VA, USDA) often have more flexible credit requirements or lower down payment options, but their rates and associated fees (like FHA mortgage insurance premiums) differ from conventional loans.

- Lender: Different lenders have different overhead costs, risk appetites, and pricing models. Shopping around is crucial to finding the best rate.

- Loan Term and Program: As discussed, 15-year fixed rates are typically lower than 30-year fixed rates. ARMs usually start lower than fixed rates.

Navigating Rate Volatility

Given the constant flux, navigating today’s mortgage market requires vigilance. If you’re pre-approved at a certain rate, remember that this rate is usually “locked” for a specific period (e.g., 30-60 days). If rates rise during your home search, your locked rate protects you. However, if rates fall, you might be able to “float down” to a lower rate, depending on your lender’s policy and fees. Staying informed daily through financial news and regular communication with your loan officer is essential to making timely decisions.

Strategies for Securing the Best Mortgage Rate

Securing a favorable mortgage rate can save tens of thousands of dollars over the life of a loan. It requires preparation, diligent research, and strategic decision-making.

The Importance of a Strong Credit Profile

Your credit score is arguably the single most impactful factor in determining your mortgage rate. Lenders use it as a primary indicator of your creditworthiness. Before applying for a mortgage, take steps to improve your credit score:

- Pay bills on time, every time. Payment history is the biggest factor.

- Reduce credit card balances. Keep utilization below 30% of your available credit.

- Avoid opening new lines of credit. New credit inquiries can temporarily ding your score.

- Check your credit report for errors. Dispute any inaccuracies promptly.

A higher credit score not only leads to a lower interest rate but can also reduce or eliminate other costs like mortgage insurance.

Exploring Different Loan Products

Don’t settle for the first loan product offered. Educate yourself on the various options available and how they align with your financial goals and risk tolerance:

- Conventional Loans: For borrowers with good credit and a decent down payment.

- FHA Loans: Ideal for first-time buyers or those with lower credit scores and smaller down payments.

- VA Loans: For eligible service members, veterans, and surviving spouses, offering 0% down payment and no PMI.

- USDA Loans: For low-to-moderate-income buyers in eligible rural areas, also offering 0% down.

- Jumbo Loans: For loan amounts exceeding conventional loan limits.

Each product has specific eligibility criteria, rate structures, and associated fees that can impact your overall cost.

Shopping Around for Lenders

This cannot be stressed enough: compare offers from multiple lenders. Studies have shown that borrowers who get quotes from several lenders can save thousands of dollars. Banks, credit unions, and independent mortgage brokers all have different pricing structures.

- Get at least 3-5 quotes. Request detailed Loan Estimates that clearly break down the interest rate, APR, fees, and closing costs.

- Compare apples to apples. Ensure the loan terms (e.g., fixed vs. adjustable, loan amount, down payment) are identical when comparing offers.

- Negotiate. With competing offers in hand, you may be able to leverage them to negotiate a better rate or lower fees with your preferred lender.

Considering a Mortgage Rate Lock

Once you have an accepted offer on a home and a loan application underway, you’ll have the option to “lock” your interest rate. A rate lock guarantees that your interest rate will not change between the time of the lock and closing, typically for 30, 45, or 60 days.

- When to lock: If you believe rates are likely to rise, or if you simply want certainty, a rate lock is a wise decision.

- Float-down option: Some lenders offer a “float-down” option, allowing you to secure a lower rate if market rates fall significantly before closing, often for an additional fee.

- Lock period: Ensure the lock period is long enough to cover your expected closing date, with a buffer for potential delays.

Beyond the Rate: Hidden Costs and Long-Term Implications

Focusing solely on the interest rate can be a costly oversight. A holistic understanding of mortgage financing means considering all the associated expenses and their long-term impact on your financial health.

Understanding APR vs. Interest Rate

The Annual Percentage Rate (APR) is a crucial metric that often gets confused with the nominal interest rate.

- Interest Rate: This is the percentage of the principal loan amount that the lender charges for borrowing money. It determines your monthly interest payment.

- APR: This represents the total cost of the loan over its life, expressed as an annual percentage. It includes the interest rate plus most closing costs and other fees (like origination fees, discount points, and some mortgage insurance premiums). The APR gives a more accurate picture of the true cost of borrowing and is a better tool for comparing different loan offers. A loan with a lower interest rate might have a higher APR if its fees are substantial.

Closing Costs and Origination Fees

Closing costs are an unavoidable part of the homebuying process, typically ranging from 2% to 5% of the loan amount. These include:

- Origination Fees: Charged by the lender for processing the loan application.

- Appraisal Fees: For assessing the home’s value.

- Title Insurance: Protects both the lender and buyer against property title disputes.

- Escrow Fees: For managing the closing process.

- Recording Fees: For officially registering the new deed and mortgage.

- Discount Points: Fees paid upfront to reduce the interest rate. One point typically equals 1% of the loan amount. Deciding whether to pay points to “buy down” your rate depends on how long you plan to stay in the home – the longer you stay, the more likely you are to recoup the cost.

These costs can significantly impact the upfront financial outlay required for a mortgage and should be carefully reviewed in the Loan Estimate.

The Impact of Property Taxes and Insurance (PITI)

While not part of the interest rate or closing costs, property taxes and homeowner’s insurance are significant ongoing expenses for homeowners.

- Principal & Interest (P&I): This is determined by your loan amount, interest rate, and loan term.

- Taxes & Insurance (T&I): Lenders often require these to be paid into an escrow account monthly along with your P&I. This combined payment is known as PITI.

- PMI (Private Mortgage Insurance): If you put less than 20% down on a conventional loan, you’ll likely pay PMI until you reach 20% equity. FHA loans also have mortgage insurance premiums (MIP). These are additional monthly costs that increase your total housing payment.

Understanding the full PITI payment is crucial for budgeting and ensuring affordability beyond just the principal and interest.

Refinancing Considerations

For existing homeowners, “what is the home mortgage rate today?” is a question that often leads to considering refinancing. Refinancing involves taking out a new mortgage to pay off your old one, usually to secure a lower interest rate, change the loan term, or tap into home equity.

- Lowering Your Interest Rate: The primary driver for refinancing. Even a small drop in rate can save significant money over the loan’s life.

- Changing Loan Term: Shorten your term to pay off the mortgage faster, or extend it to lower monthly payments.

- Cash-Out Refinance: Borrow more than you owe on your current mortgage and take the difference in cash, often used for home improvements or debt consolidation.

When considering a refinance, carefully weigh the interest rate savings against the new closing costs. It’s only financially sensible if you’ll stay in the home long enough for the savings to outweigh these upfront expenses.

The Future Outlook for Mortgage Rates

Predicting the precise trajectory of mortgage rates is notoriously difficult, even for seasoned economists. However, by staying informed about current market trends and expert analyses, borrowers can make more educated guesses about what lies ahead.

Expert Predictions and Market Trends

Economists and housing market analysts constantly monitor global and domestic economic indicators to forecast interest rate movements. Their predictions often hinge on:

- The Federal Reserve’s stance: Will they raise, hold, or cut the federal funds rate? Their primary focus on inflation and employment greatly impacts expectations.

- Inflation trajectory: If inflation persists or accelerates, upward pressure on rates is likely.

- Economic growth: A strong economy often supports higher rates, while a slowdown can lead to rate decreases.

- Geopolitical stability: Global events can introduce uncertainty, causing investors to seek safe-haven assets, which can temporarily push down bond yields and mortgage rates.

It’s common to see a range of predictions, but a consensus often emerges regarding the general direction. Borrowers should consult reputable financial news outlets and analyses from major financial institutions for the most current outlook.

Preparing for Rate Changes

Given the inherent uncertainty, the best strategy for borrowers is to be prepared for various scenarios:

- For Buyers: If rates are expected to rise, locking in a rate sooner rather than later might be advantageous. If rates are anticipated to fall, a borrower with flexibility might wait, but this carries the risk of rates moving in the opposite direction.

- For Refinancers: Monitor rates diligently. Set up rate alerts with lenders. If rates dip significantly below your current rate, be ready to act quickly to take advantage of the opportunity, but always factor in closing costs.

Ultimately, the “best” time to secure a mortgage rate is when it aligns with your personal financial goals and affordability, regardless of whether it’s the absolute lowest rate ever recorded. A mortgage is a long-term commitment, and securing a rate that ensures comfort and stability for decades is often more valuable than chasing marginal, fleeting dips in the market.

In conclusion, “what is the home mortgage rate today?” is a question with a multi-faceted answer, shaped by global economics and tailored by individual financial profiles. By understanding the forces at play, meticulously preparing your finances, and diligently shopping for the best terms, you can confidently navigate the mortgage market and make a sound investment in your future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.