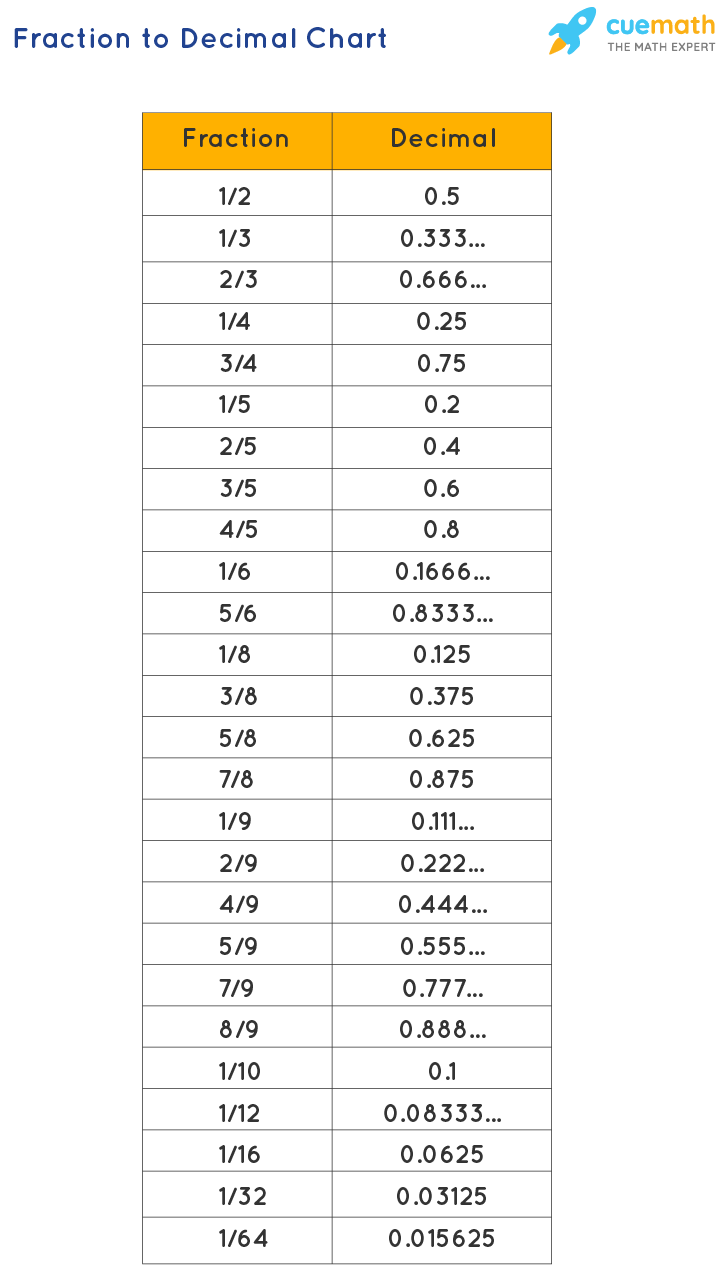

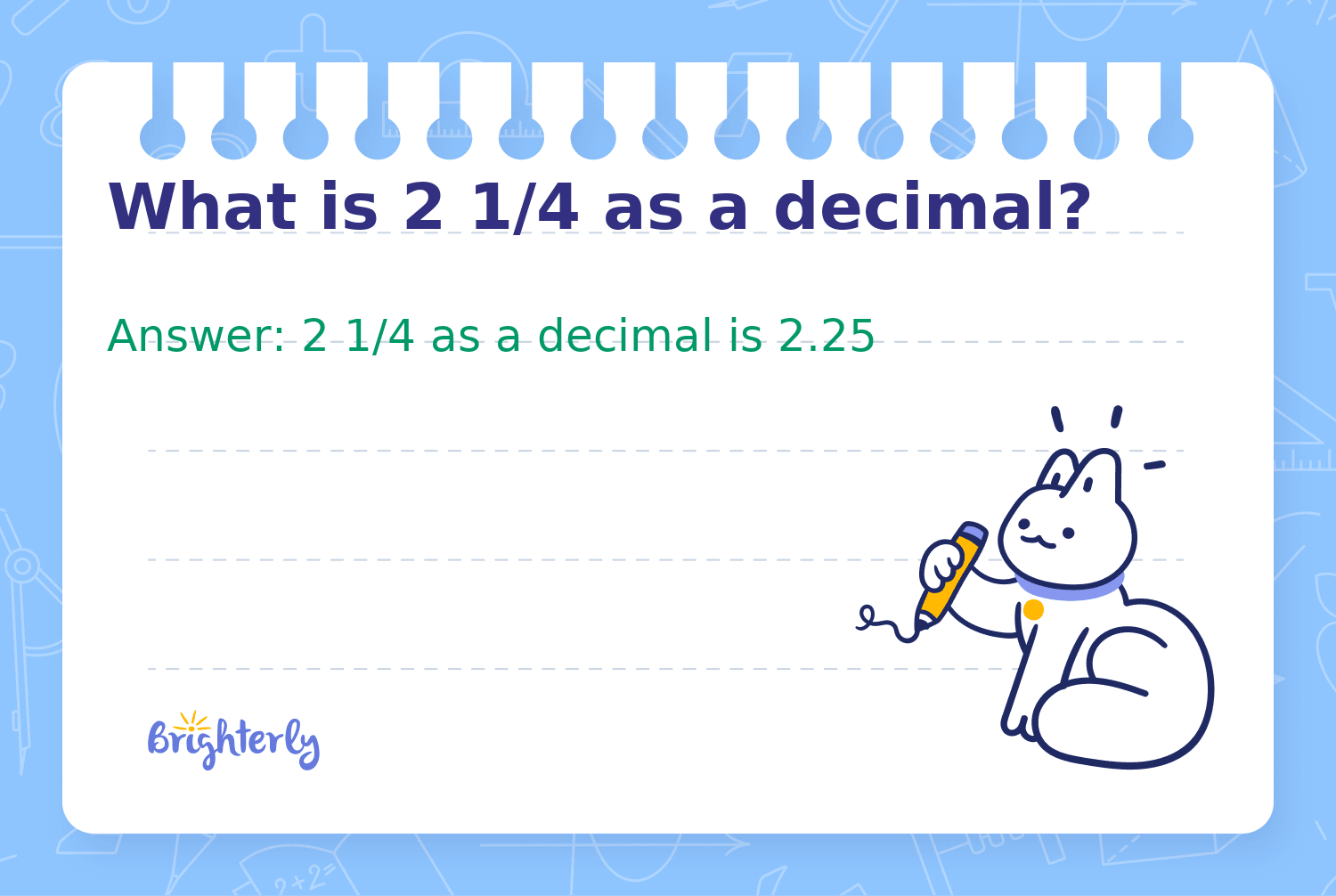

In the world of finance, precision is more than just a mathematical requirement; it is the bedrock of wealth accumulation, risk management, and strategic planning. While a student in a classroom might ask, “What is the decimal for 2 1/2?” simply to pass a quiz, a savvy investor or a homeowner asks the same question to understand the trajectory of their financial future. The answer, 2.5, is a figure that appears across balance sheets, interest rate announcements, and dividend yield reports.

Understanding how to convert fractions to decimals—and more importantly, understanding what those decimals represent in a monetary context—is a fundamental skill for anyone looking to master their personal finances. This article explores the significance of the number 2.5 in the financial landscape, the transition from fractional to decimal reporting in markets, and how small decimal points dictate the growth of your capital.

From Fractions to Decimals: Why Financial Clarity Matters

For decades, the financial world operated on a system of fractions. If you looked at the New York Stock Exchange in the mid-1990s, stock prices weren’t listed in neat decimals like $20.50; they were listed in eighths, sixteenths, or thirty-seconds of a dollar. A stock might be quoted at 20 1/2, meaning twenty dollars and fifty cents.

The Transition from Traditional Brokerage to Digital Platforms

The shift from fractions to decimals, known as “decimalization,” occurred in the early 2000s and revolutionized the way we perceive money. Before this shift, the smallest spread (the difference between the buy and sell price) was often 1/8 of a dollar, or 12.5 cents. By moving to a decimal system where 2 1/2 became 2.50, the minimum spread dropped to a single penny.

For the average investor, this meant significantly lower transaction costs. When we ask for the decimal equivalent of 2 1/2 today, we are participating in a modernized financial system that prioritizes transparency and narrow margins. This clarity allows for high-frequency trading and more accurate algorithmic modeling, ensuring that your “2.5” is exactly that—no hidden fractional slippage involved.

How 2.5 Percent Impacts Compounding Interest

In the realm of personal finance, 2 1/2 is most commonly encountered as 2.5%. While 2.5 may seem like a small number, the power of compounding interest turns this decimal into a formidable force over time. Whether it is the interest rate on a high-yield savings account or the annual inflation rate, the difference between 2% and 2.5% is substantial when projected over a decade.

Compounding interest is the process where the value of an investment increases because the earnings on an investment, both capital gains and interest, earn interest as time passes. If you have $100,000 invested at 2.5%, you earn $2,500 in the first year. In the second year, you earn interest on $102,500. Over twenty years, that extra “1/2” (the 0.5%) can result in thousands of dollars of difference compared to a flat 2% rate.

Calculating the Real-World Impact of a 2.5% Interest Rate

To truly appreciate the decimal 2.5, one must look at its application in debt and savings. In a low-interest-rate environment, 2.5% often serves as a psychological and economic benchmark for “cheap money” or “stable growth.”

Mortgage and Loan Amortization

For many individuals, the most significant “2.5” they will ever encounter is a mortgage interest rate. When a borrower secures a home loan at 2 1/2 percent versus 3 percent, the long-term savings are transformative. On a $400,000 mortgage over 30 years, the difference of that 0.5% (the fractional “1/2”) amounts to approximately $40,000 in interest payments.

This is why financial literacy involves a deep comfort with converting fractions to decimals. When a bank quotes a rate of 2 1/2, a borrower must immediately recognize it as 2.5% to input it into amortization calculators. Understanding this conversion allows for a direct comparison between lenders who may use different notation styles, ensuring the borrower chooses the most cost-effective path to homeownership.

High-Yield Savings Accounts and Inflation Hedging

On the flip side of debt is the world of savings. For much of the last decade, finding a savings account that offered a 2.5% return was considered a win for conservative investors. When the decimal for 2 1/2 is applied to a liquid savings account, it often acts as a baseline for preserving purchasing power.

Economists generally target an inflation rate of around 2%. If your money is earning 2.5% in a decimalized savings account, you are achieving a “real rate of return” of 0.5%. While this isn’t enough to build massive wealth, it is essential for an emergency fund. Understanding that 2 1/2 equals 2.5 allows a saver to quickly scan financial news and determine if their current banking products are keeping pace with the cost of living.

Investment Strategies Centered on 2.5% Benchmarks

In the stock and bond markets, the number 2.5 often serves as a “yield hurdle.” Many professional investors look for specific percentages to trigger buy or sell orders, and 2.5% is a frequent target for dividend-seeking portfolios.

Dividend Yields and Reinvestment Plans

A dividend yield is a financial ratio that tells you how much a company pays out in dividends each year relative to its stock price. If a stock is trading at $100 and pays a $2.50 annual dividend, its yield is 2.5%. For an income investor, seeing a yield of “two and a half percent” is a signal of a mature, stable company.

Converting 2 1/2 to 2.5 is the first step in a Dividend Reinvestment Plan (DRIP). By understanding the decimal value, investors can calculate how many fractional shares they will receive upon each payout. If you own 100 shares of a company, a 2.5% yield provides a predictable stream of capital that can be used to acquire more assets, further fueling the engine of compound interest.

The 2.5% Withdrawal Rule in Retirement Planning

In retirement planning, the “4% Rule” has long been the gold standard for how much one can safely withdraw from a portfolio each year without running out of money. However, in volatile markets or eras of lower expected returns, many financial advisors suggest a more conservative “2.5% Withdrawal Rule.”

By choosing to live off 2.5 (the decimal for 2 1/2) percent of a portfolio rather than 4 percent, an individual significantly increases the longevity of their wealth. This strategy is particularly popular among the FIRE (Financial Independence, Retire Early) community. For a retiree with a $2 million portfolio, the difference between a 4% withdrawal ($80,000) and a 2.5% withdrawal ($50,000) is the difference between potential portfolio depletion and perpetual wealth.

Advanced Financial Tools for Decimal Conversion and Modeling

In the modern era, we rarely perform these conversions by hand, but the logic remains vital. Professional-grade financial tools and software rely on decimal inputs to generate the complex projections that drive corporate finance and personal wealth management.

Using Spreadsheets for Precise Financial Projections

Whether you are using Microsoft Excel, Google Sheets, or specialized financial software, the system does not recognize “2 1/2” as a numerical value for calculation purposes. It views it as text. To perform any meaningful analysis—such as calculating Net Present Value (NPV) or Internal Rate of Return (IRR)—the user must input the decimal 2.5.

Mastering the use of decimals in spreadsheets allows you to build “What-If” scenarios. For instance, what happens to your retirement fund if your annual return is 2.5% versus 7%? By using the decimal format, you can automate these calculations across thousands of cells, providing a visual roadmap of your financial trajectory.

The Role of Financial Calculators in Debt Management

Financial calculators, both physical and digital, are designed to handle decimal inputs to solve for time-value-of-money problems. When calculating the payoff period for a credit card or a student loan, the interest rate is the most volatile variable. Many older loan contracts still reference fractional rates (e.g., Prime + 2 1/2).

To use a financial calculator effectively, one must convert that fractional “add-on” into 2.5. This allows the user to determine the exact daily interest charge, empowering them to make informed decisions about debt consolidation or accelerated payment strategies.

Conclusion: Integrating Decimal Precision into Your Financial Life

What is the decimal for 2 1/2? On the surface, it is 2.5. But in the context of money, it is a symbol of clarity, a lever for interest rates, and a benchmark for investment success. Whether you are calculating the interest on a small loan, evaluating the dividend yield of a Fortune 500 company, or planning a conservative withdrawal strategy for retirement, the transition from fractions to decimals is a transition toward better financial control.

By embracing the decimal system, we move away from the ambiguity of the past and toward a future where every tenth of a percent can be tracked, managed, and optimized. In the pursuit of financial independence, remember that precision is your greatest ally. The difference between 2 and 2.5 might seem negligible in a notebook, but in a brokerage account over thirty years, it is the difference between a comfortable retirement and a strained one. Stay precise, stay informed, and always look at the decimals behind the fractions.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.