For veterans, active-duty service members, and eligible surviving spouses, the VA home loan program represents one of the most significant financial benefits earned through military service. However, in an era of fluctuating inflation and shifting central bank policies, the question of “what is the current VA loan interest rate” is rarely met with a single, static number. Because VA loans are provided by private lenders—not the Department of Veterans Affairs itself—rates vary based on market conditions, lender appetites, and individual financial profiles.

Understanding the mechanics of VA loan interest rates is essential for any veteran looking to maximize their purchasing power or optimize their long-term wealth. This guide explores the factors driving today’s rates, how they compare to the broader market, and the strategies you can employ to secure the most favorable terms for your financial future.

Understanding the Fundamentals of VA Loan Rates

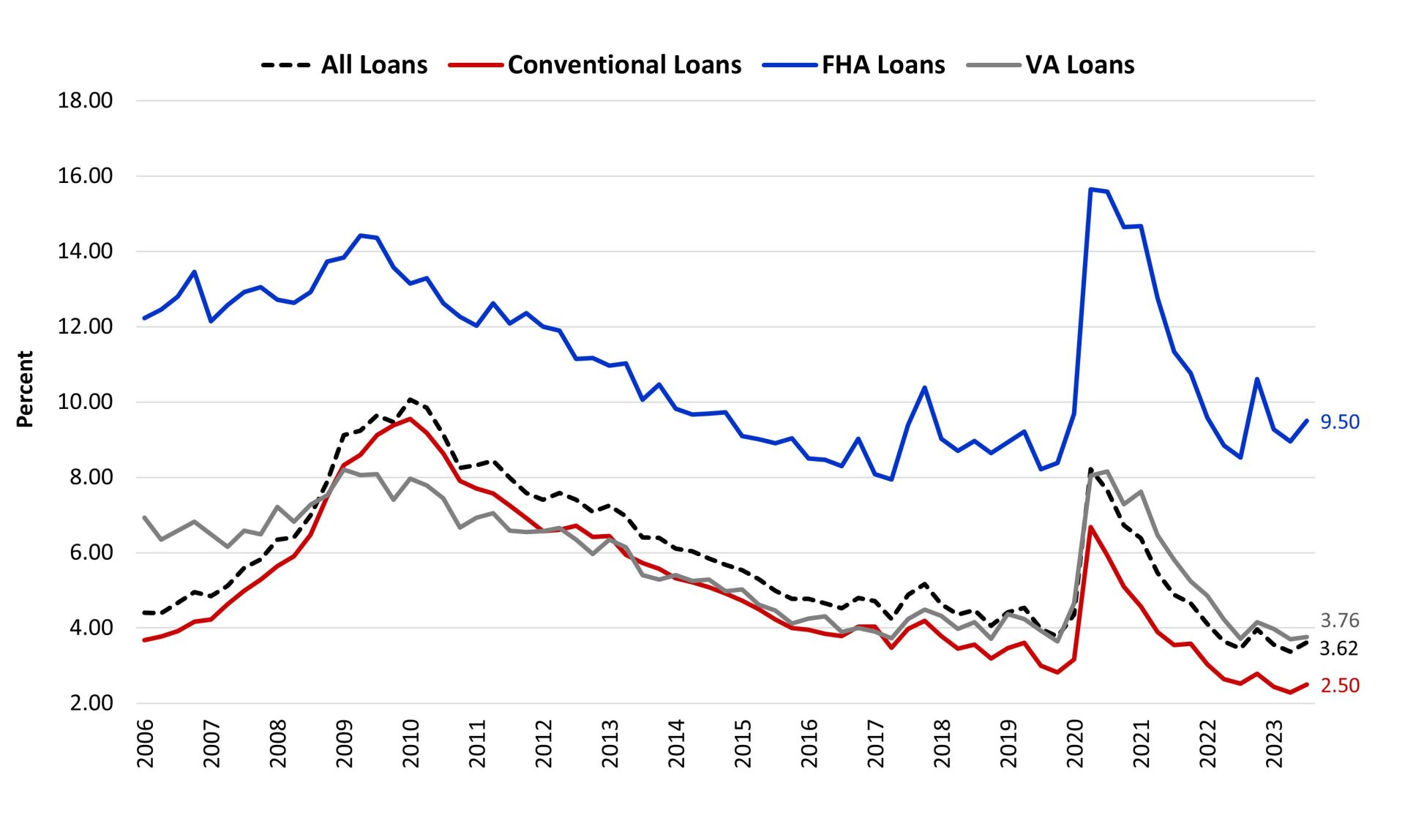

To understand why VA loan rates sit where they do today, one must first understand that the VA does not set interest rates. Instead, the VA provides a government guarantee to private lenders, promising to repay a portion of the loan if the borrower defaults. This “safety net” reduces risk for banks, which is why VA interest rates are historically lower than those of conventional mortgages.

How VA Loan Rates Differ from Conventional Mortgages

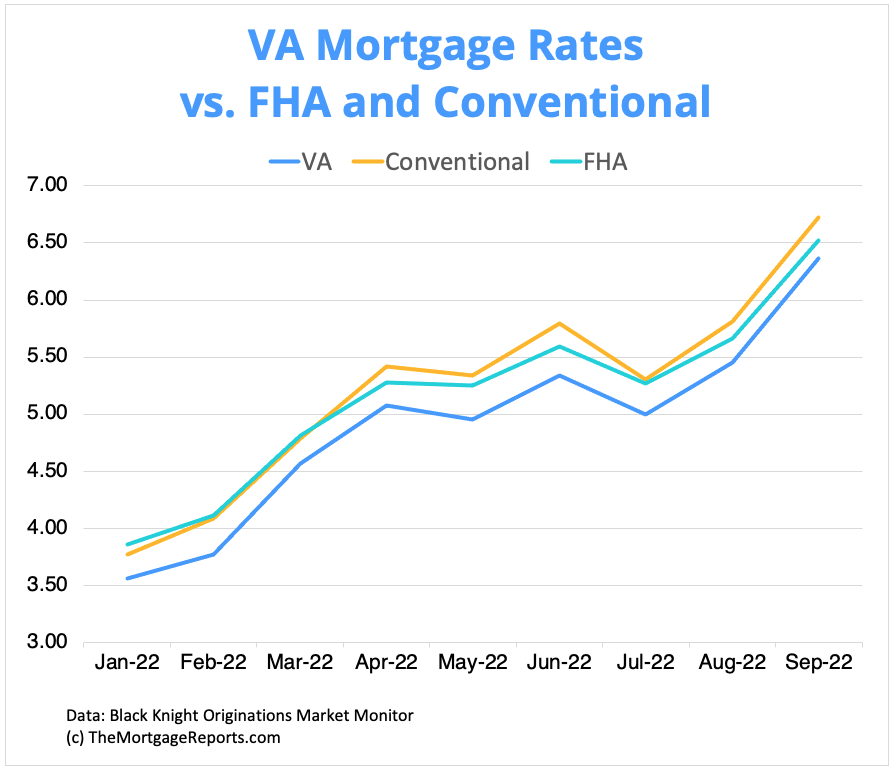

Traditionally, VA loan interest rates hover between 0.25% and 0.50% lower than conventional 30-year fixed-rate mortgages. This gap exists because of the federal guarantee. In a high-interest-rate environment, this delta becomes even more critical. While a conventional borrower might be looking at a rate that prices them out of a specific neighborhood, a veteran using their entitlement might still find the monthly payment manageable due to the competitive edge of the VA program. Furthermore, because VA loans do not require Private Mortgage Insurance (PMI), the “effective” rate—the total cost of borrowing—is significantly lower than other low-down-payment options like FHA or 3% down conventional loans.

The Impact of the Federal Reserve on Veteran Lending

While the VA doesn’t set rates, the Federal Reserve’s monetary policy serves as the primary engine behind them. When the Fed raises the federal funds rate to combat inflation, the yield on the 10-year Treasury note typically rises. Mortgage rates, including those for VA loans, are closely tied to the movement of these Treasury yields. In recent years, as the Fed has navigated a “higher-for-longer” interest rate environment, VA rates have climbed from their historic pandemic lows. However, because VA loans are bundled into Ginnie Mae mortgage-backed securities (MBS), they often attract investors seeking government-backed stability, which helps keep rates relatively suppressed compared to the volatile private market.

Factors That Influence Your Specific VA Interest Rate

Even when the national average for a VA loan is quoted at a specific percentage, your individual offer may differ. Lenders use “risk-based pricing” to determine the specific interest rate they are willing to offer an applicant.

Credit Scores and Their Role in VA Financing

One of the biggest myths in veteran lending is that credit scores don’t matter because the loan is government-backed. While the VA itself does not mandate a minimum credit score, individual lenders (known as “overlays”) do. Typically, a borrower with a credit score of 740 or higher will receive the “par rate”—the best available rate without paying extra fees. Borrowers with scores in the 620 to 660 range may still qualify for a VA loan, but they will likely face a higher interest rate to compensate the lender for the perceived increase in risk. Improving your credit score by even 20 points before applying can potentially save you tens of thousands of dollars in interest over the life of a 30-year loan.

Debt-to-Income Ratio (DTI) and Loan Terms

Lenders also look closely at your Debt-to-Income (DTI) ratio, which measures how much of your gross monthly income goes toward debt payments. While the VA is more flexible with DTI than conventional programs—sometimes allowing ratios upwards of 41% or even higher with compensating factors—a high DTI can sometimes lead a lender to increase the interest rate. Additionally, the length of the loan significantly impacts the rate. A 15-year fixed-rate VA loan will almost always offer a lower interest rate than a 30-year fixed-rate loan, as the lender is exposed to market volatility for a shorter period.

Strategies to Secure the Lowest Possible VA Interest Rate

Securing a competitive interest rate requires more than just showing up with a Certificate of Eligibility (COE). It requires a proactive approach to financial management and a willingness to negotiate with multiple financial institutions.

The Power of Discount Points

If you have extra cash on hand at closing, you can “buy down” your interest rate using discount points. One point typically costs 1% of the total loan amount and reduces your interest rate by approximately 0.25%. For a veteran planning to stay in their home for ten years or more, paying for points can be a brilliant financial move. The “break-even point” is the moment when the monthly savings from the lower rate exceed the initial cost of the points. In a market where rates are expected to remain stable or rise, locking in a lower rate via points provides long-term certainty and significant interest savings.

Shopping Around: Comparing Lenders and APRs

Perhaps the most overlooked strategy is shopping around. There is a common misconception that all VA lenders offer the same rate because it is a government program. This is false. Rates can vary by as much as 0.5% between a large national bank, a local credit union, and a specialized online mortgage lender. When comparing offers, it is vital to look at the Annual Percentage Rate (APR) rather than just the nominal interest rate. The APR includes the interest rate plus lender fees, origination charges, and other costs. A lender offering a “low rate” might be hiding high closing costs that make the loan more expensive in the long run.

Current Market Trends and Future Projections for VA Loans

As we move through the current fiscal year, the trajectory of VA loan interest rates remains a focal point for economists and home buyers alike. The market is currently in a state of “price discovery,” where participants are trying to gauge when the Federal Reserve will begin its next cycle of rate cuts.

The Economic Outlook for Veterans

Economists generally agree that mortgage rates have likely peaked, but the descent to the ultra-low rates of 2020 is unlikely to happen anytime soon. For veterans, this means the focus should shift from “timing the market” to “time in the market.” Historically, even a 6% or 7% interest rate is moderate compared to the double-digit rates seen in the 1980s. The current trend suggests a period of stabilization. For those waiting for rates to drop to 3% again, the opportunity cost of rising home prices may outweigh the benefit of a lower rate later.

Is Now the Right Time to Buy or Refinance?

The decision to buy now or wait depends on the individual’s “buy-and-hold” strategy. One unique advantage of the VA program is the Interest Rate Reduction Refinance Loan (IRRRL), often called a “VA Streamline.” This allows veterans to refinance their existing VA loan into a lower-rate VA loan with minimal paperwork and no out-of-pocket costs. This “refinance optionality” means that if you buy now at a 6.5% rate and rates drop to 5.5% in two years, you can easily pivot to the lower rate. This makes the “current” rate less of a permanent barrier and more of a temporary entry point.

Long-Term Financial Benefits of the VA Loan Program

When evaluating the current VA loan interest rate, it is important to view it within the context of the total financial package. A VA loan is often the most mathematically sound way for a veteran to build wealth through real estate.

No Down Payment and No Private Mortgage Insurance (PMI)

The absence of a down payment requirement allows veterans to keep their capital invested in other assets, such as the stock market or high-yield savings accounts, which may be earning a return that offsets the mortgage interest. Furthermore, the lack of PMI is a massive financial boon. On a conventional loan with 5% down, PMI can add hundreds of dollars to a monthly payment. Because VA loans forgo this, a veteran with a 6.5% interest rate often has a lower total monthly payment than a conventional borrower with a 6.0% rate who is forced to pay PMI.

The VA Funding Fee vs. Lifetime Interest Savings

While most VA loans require a “funding fee”—a one-time payment that helps sustain the program for future generations—this fee can be rolled into the loan amount. For veterans with a service-connected disability, this fee is waived entirely. Even for those who pay it, the cost is typically eclipsed by the savings generated by the lower interest rates and the lack of monthly insurance premiums over 30 years. When you calculate the “net present value” of a VA loan versus any other mortgage product, the VA loan almost always wins, making the current interest rate just one piece of a very favorable financial puzzle.

In conclusion, while the “current” VA loan interest rate is subject to the whims of the global economy and Federal Reserve policy, the program remains the gold standard of personal finance for those who have served. By understanding the factors that influence these rates and utilizing strategies like discount points and lender comparisons, veterans can secure a home and build a foundation for lasting financial security.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.