The landscape of homeownership has undergone a seismic shift over the last few years. For nearly a decade, prospective homebuyers enjoyed a climate of historically low interest rates, often dipping below the 3% mark. However, as global economic pressures, inflation, and shifting monetary policies have taken center stage, the “new normal” for mortgage rates looks significantly different. Understanding what the current interest rates on home loans are—and more importantly, what drives them—is essential for any individual looking to make a sound financial investment in real estate.

In the current financial environment, a difference of even half a percent in your mortgage rate can equate to tens of thousands of dollars over the life of a loan. This article explores the intricate world of mortgage interest rates, the macroeconomic factors that dictate their movement, and the personal financial strategies you can employ to secure the best possible terms for your home purchase.

The Macroeconomic Landscape: What Drives Mortgage Rates?

Mortgage rates do not exist in a vacuum. They are the product of a complex interplay between government policy, investor sentiment, and global economic health. While many people believe the Federal Reserve sets mortgage rates directly, the reality is more nuanced.

The Role of the Federal Reserve and the Federal Funds Rate

The Federal Reserve (the Fed) influences mortgage rates primarily through the Federal Funds Rate—the interest rate at which commercial banks borrow and lend to one another overnight. When the Fed raises this rate to combat inflation, the cost of borrowing increases across the board. While this doesn’t move mortgage rates in a 1:1 ratio, it sets the floor for consumer lending. When banks pay more to borrow money, they pass those costs on to consumers in the form of higher interest rates on home loans, credit cards, and auto loans.

Inflation and the 10-Year Treasury Yield

Perhaps the most significant indicator for current mortgage rates is the 10-year Treasury bond yield. Investors view mortgages as long-term debt securities. To remain competitive, mortgage-backed securities (MBS) must offer a higher yield than “risk-free” government bonds. When inflation is high, the purchasing power of the future interest payments on a mortgage is eroded. To compensate for this risk, lenders demand higher interest rates. Consequently, when you see the 10-year Treasury yield rise, mortgage rates almost inevitably follow suit.

Economic Growth and Market Volatility

In a robust, growing economy, the demand for capital increases, which can push interest rates higher. Conversely, during a recession, the Fed often lowers rates to stimulate borrowing and spending. Current rates reflect the market’s attempt to find a balance between cooling an overheated, inflationary economy and avoiding a full-scale recession. This “tug-of-war” is why we often see daily fluctuations in the rates offered by major lenders.

Comparing Loan Products: Fixed-Rate vs. Adjustable-Rate Mortgages

When researching current interest rates, it is vital to distinguish between the different types of loan products available. The “headline” rate you see in news reports usually refers to the 30-year fixed-rate mortgage, but this is far from the only option.

The Stability of the 30-Year and 15-Year Fixed-Rate Mortgage

The 30-year fixed-rate mortgage remains the gold standard for American homeowners. It offers the security of a consistent monthly payment for three decades, protecting the borrower from future interest rate hikes. The 15-year fixed-rate mortgage typically offers a significantly lower interest rate—often 0.5% to 1% lower than the 30-year—because the lender is exposed to risk for a shorter duration. However, the trade-off is a much higher monthly payment, as the principal is amortized over half the time.

The Strategic Use of Adjustable-Rate Mortgages (ARMs)

In a high-interest-rate environment, Adjustable-Rate Mortgages (ARMs) often regain popularity. An ARM typically offers a lower “teaser” rate for an initial period (usually 5, 7, or 10 years). After this period, the rate adjusts annually based on current market indices. For a buyer who plans to sell the home or refinance before the initial period ends, an ARM can be a sophisticated financial tool to save thousands in interest during the early years of the loan. However, the inherent risk is that if rates are even higher when the adjustment period hits, the monthly payment could skyrocket.

Personal Financial Factors That Determine Your Specific Rate

While market conditions set the “base” rate, your personal financial profile determines the “risk premium” a lender adds to that base. Two borrowers applying on the same day for the same loan amount can receive vastly different interest rate offers.

The Critical Importance of Your Credit Score

Your credit score is the single most influential factor within your control. Lenders categorize borrowers into “tiers.” Those with “excellent” credit (typically 740 to 850) receive the lowest advertised rates. If your score falls into the “fair” category (below 670), you may face a “Loan Level Price Adjustment” (LLPA). This is an additional fee or a higher interest rate tacked on to compensate the lender for the increased risk of default. Improving your score by even 20 points before applying can potentially lower your interest rate by 0.25%, saving you a fortune over time.

Down Payments and Loan-to-Value (LTV) Ratios

The amount of equity you have in the home also dictates your rate. A 20% down payment is the traditional benchmark; it eliminates the need for Private Mortgage Insurance (PMI) and signals to the lender that you are a low-risk borrower. If you put down 3.5% (common for FHA loans) or 5%, you are considered a higher risk. Paradoxically, sometimes FHA loans have lower base interest rates than conventional loans, but when the mandatory mortgage insurance premiums are added, the “Effective Rate” or APR (Annual Percentage Rate) is often higher.

Debt-to-Income (DTI) Ratio and Cash Reserves

Lenders also look at your DTI—the percentage of your gross monthly income that goes toward paying debts. A lower DTI suggests you have the financial “breathing room” to handle a mortgage payment even if your income fluctuates. Additionally, having significant “cash reserves” (liquid savings equal to 6–12 months of mortgage payments) can sometimes help you negotiate a slightly better rate or qualify for specialized “portfolio” loans that aren’t available to the general public.

Strategies to Secure the Best Possible Rate

In a volatile market, being a passive observer can be expensive. To secure the most favorable interest rate on a home loan, you must be proactive and utilize the financial tools available to you.

The Art of the Rate Lock

Once you have found a home and started the loan process, you will have the opportunity to “lock in” your rate. A rate lock guarantees that your interest rate won’t change between the time you apply and the time you close, provided you close within a specific window (usually 30 to 60 days). If rates rise during that period, you are protected. Some lenders also offer a “float-down” provision, which allows you to take advantage of a lower rate if the market happens to drop before you close.

Buying Down the Rate with Discount Points

Borrowers can “buy” a lower interest rate by paying “points” at closing. One point is equal to 1% of the total loan amount. In exchange for this upfront payment, the lender permanently lowers your interest rate (often by about 0.25% per point). This is a mathematical calculation: you must determine your “break-even point.” If paying $4,000 upfront saves you $100 a month, it will take 40 months to break even. If you plan to stay in the home for 10 years, buying points is a highly effective way to reduce the total interest paid.

Aggressive Comparison Shopping

It is a common mistake to simply use the bank where you have a checking account. Mortgage brokers, credit unions, and online lenders all have different “appetites” for risk and different overhead costs. Obtaining at least three “Loan Estimates” allows you to compare the APR—not just the interest rate. The APR includes the interest rate plus lender fees, making it the most accurate tool for an apples-to-apples comparison.

The Long-Term Financial Implications of Rate Fluctuations

To truly understand the importance of current interest rates, one must look at the long-term mathematical impact on wealth accumulation. A mortgage is often the largest debt a person will ever carry, and the interest is front-loaded in the early years of the loan.

Impact on Monthly Cash Flow and Opportunity Cost

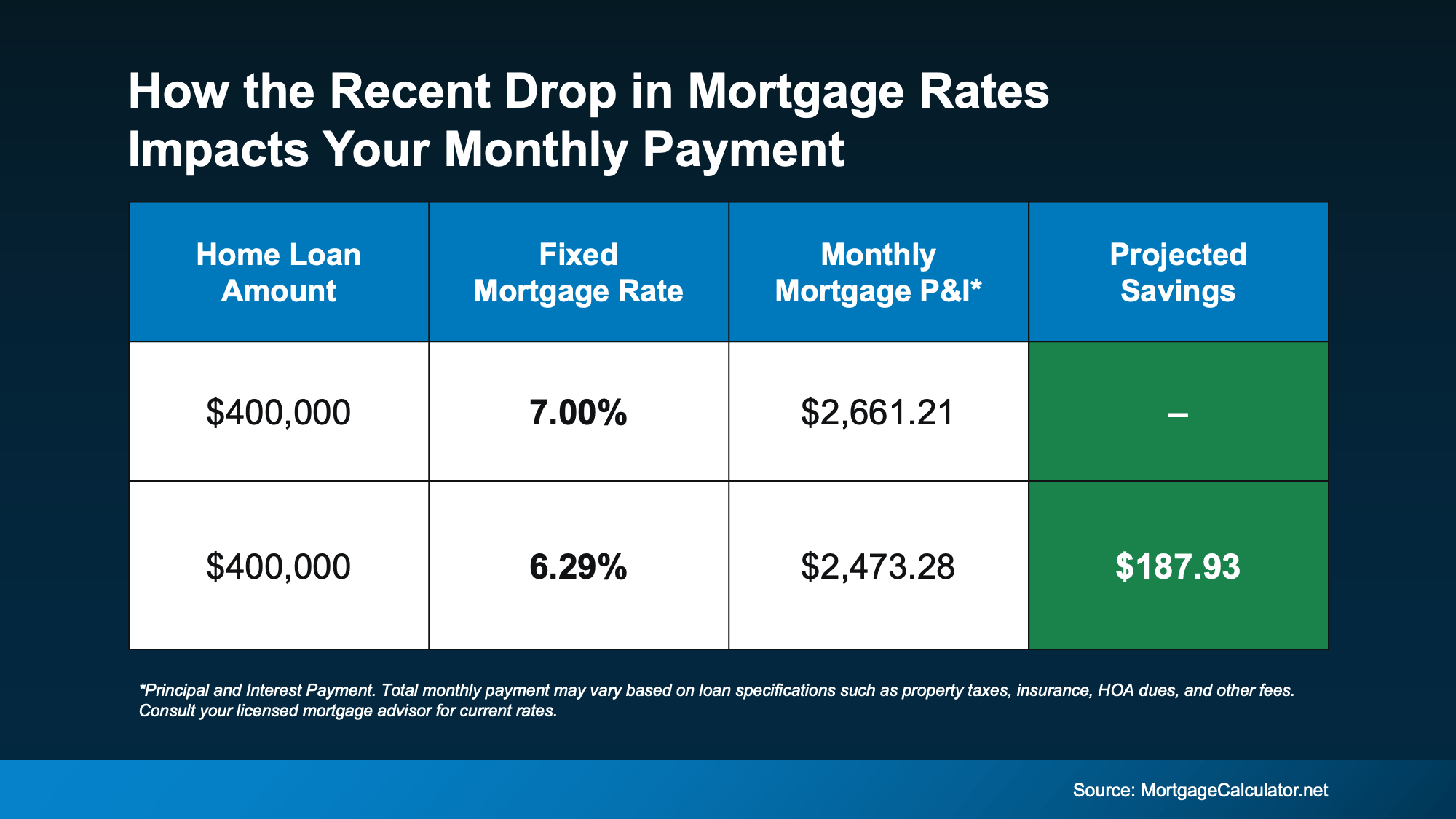

A higher interest rate reduces your monthly discretionary income. For example, on a $400,000 loan, the difference between a 4% rate and a 7% rate is roughly $750 per month. That is $750 that cannot be invested in a 401(k), used for home improvements, or put toward a child’s education. Over 30 years, that “opportunity cost” is staggering when you consider the lost compound interest from those potential investments.

Total Interest Paid Over the Life of the Loan

Using the same $400,000 example, at a 4% interest rate, you would pay approximately $287,000 in total interest over 30 years. At a 7% interest rate, you would pay approximately $558,000. In this scenario, the higher interest rate results in you paying nearly the entire value of the loan again just in interest. Understanding this helps homeowners realize that the “price” of the house is only one part of the equation; the “cost of the money” is equally important.

The Refinance Strategy: “Marry the House, Date the Rate”

A popular mantra in the current real estate market is to “marry the house and date the rate.” This philosophy suggests that if you find the right property, you should purchase it even at a higher current rate, with the intention of refinancing when rates eventually drop. While this is a viable financial strategy, it requires careful planning. You must ensure you can comfortably afford the current payment, and you must maintain good credit and home equity to qualify for a refinance in the future.

In conclusion, while we may no longer be in an era of “free money,” understanding the mechanics of current interest rates on home loans allows you to navigate the market with confidence. By optimizing your credit, choosing the right loan product, and understanding the macroeconomic signals, you can secure a mortgage that serves as a foundation for long-term financial stability rather than a burden on your wealth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.