For many Americans, a car is not just a convenience; it’s a necessity for work, family, and daily life. But this essential asset comes with a significant cost, and the monthly car payment is often one of the largest recurring expenses for households. Understanding the average car payment in America is more than just a statistical curiosity; it’s a vital benchmark for personal financial planning. It helps individuals assess if their own payments are in line with market trends, provides context for budget allocation, and highlights the broader economic forces at play in the automotive market. As vehicle prices continue to climb and financing options evolve, staying informed about these averages becomes crucial for making financially sound decisions and avoiding the pitfalls of overspending on transportation. This article will delve into the current landscape of car payments, explore the factors influencing these figures, discuss their financial implications, and offer actionable strategies for managing and potentially reducing this significant monthly outlay.

Understanding the Current Landscape of Car Payments

The automotive market is dynamic, influenced by everything from global supply chains to consumer credit scores. As a result, average car payments are not static figures but rather a reflection of numerous intersecting factors. Grasping these influences is the first step toward making an informed car-buying decision.

Key Factors Influencing Average Payments

Several critical elements combine to determine the average car payment. Understanding how each plays a role can empower you to navigate the purchasing process more effectively.

- New vs. Used Cars: Unsurprisingly, the most significant differentiator is whether you’re buying new or used. New cars command a higher price tag due to depreciation, advanced features, and brand new condition, leading to substantially higher monthly payments. Used cars, having already absorbed the initial depreciation hit, are generally more affordable, though their payments are also on the rise.

- Loan Term Lengths: The duration of your loan, typically expressed in months (e.g., 60, 72, 84 months), has a direct impact on your monthly payment. Longer terms lead to lower monthly payments but result in more interest paid over the life of the loan. Shorter terms mean higher monthly payments but less overall interest and faster debt repayment. The industry has seen a trend towards longer loan terms as vehicle prices increase, making monthly payments more “affordable” but often at a greater total cost.

- Interest Rates: The interest rate attached to your car loan is paramount. It is heavily influenced by your credit score, market interest rates (set by the Federal Reserve), and the specific lender. Borrowers with excellent credit scores qualify for the lowest rates, while those with lower scores face higher rates, significantly increasing both their monthly payment and the total cost of the vehicle.

- Down Payment: The amount of money you put down upfront directly reduces the principal amount you need to borrow. A larger down payment translates to a smaller loan, which in turn leads to lower monthly payments and less interest accumulated over the loan term. Experts often recommend a down payment of at least 10-20% for new cars and 10% for used cars to mitigate financial risk.

- Vehicle Type and Price: The make, model, and trim level of the vehicle are obvious determinants. A luxury SUV will naturally have a higher payment than an economy sedan. Features like all-wheel drive, premium sound systems, and advanced safety packages all add to the total vehicle price and, consequently, the monthly payment.

- Additional Costs and Fees: Beyond the sticker price, various taxes, registration fees, documentation fees, and optional add-ons like extended warranties or GAP insurance are often rolled into the total loan amount, increasing the principal and thus the monthly payment.

Recent Trends and Data Points

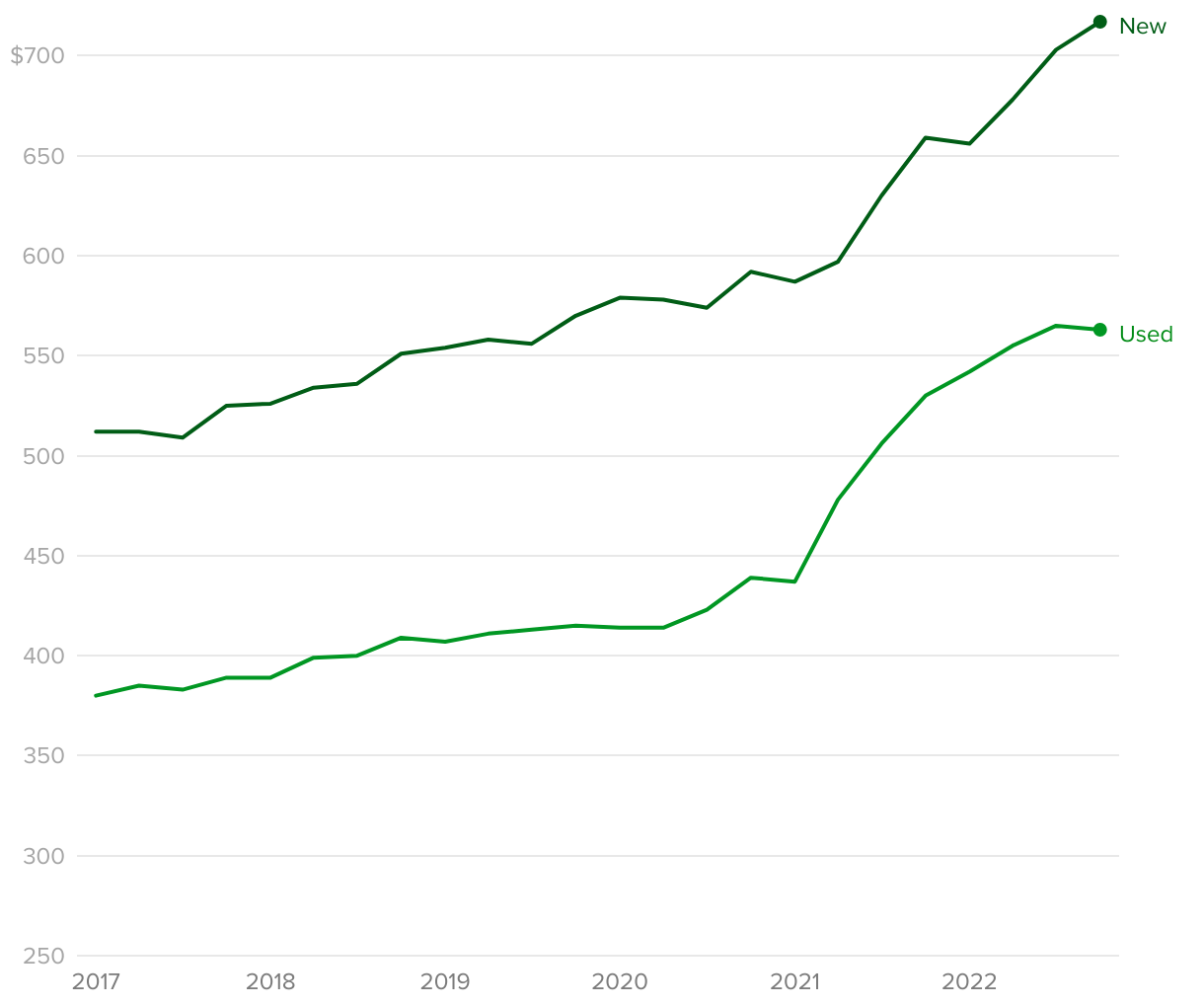

Reputable financial institutions and automotive industry trackers regularly compile data on average car payments. While these figures fluctuate, they provide valuable insight into the market. As of recent reports from sources like Experian and Edmunds, the average new car payment in America has frequently hovered in the range of $700 to $750 per month, while the average used car payment has been closer to $500 to $550 per month. It’s crucial to note these are averages, and individual experiences will vary widely based on the factors mentioned above.

Several key trends underpin these rising averages:

- Escalating Vehicle Prices: The average transaction price for both new and used vehicles has been on an upward trajectory, driven by factors like inflation, supply chain disruptions, and a shift in consumer preference towards more expensive SUVs and trucks.

- Longer Loan Terms: To keep monthly payments seemingly manageable in the face of higher prices, lenders and consumers increasingly opt for extended loan terms. While an 84-month (7-year) car loan was once rare, it has become more common, especially for new vehicles. While this reduces the monthly burden, it significantly increases the total interest paid and raises the risk of being “upside down” (owing more than the car is worth).

- Higher Interest Rates: As the Federal Reserve has raised interest rates to combat inflation, car loan rates have also climbed. This makes borrowing more expensive, pushing monthly payments higher even for the same vehicle price and loan term.

- Improved Credit Quality for New Loans: Despite the rising costs, lenders have also become more selective, often approving loans for buyers with better credit scores, which can paradoxically keep the average interest rate from skyrocketing even more than it otherwise would. However, this means those with lower credit scores face even more challenging financing conditions.

These trends highlight a challenging environment for car buyers, necessitating careful financial planning and a thorough understanding of all costs involved.

The Financial Implications of Your Car Payment

A car payment isn’t just a number on a statement; it’s a commitment that can profoundly impact your personal finances. Understanding these implications is crucial for maintaining financial health and achieving broader financial goals.

Impact on Your Monthly Budget

The most immediate and tangible effect of a car payment is its strain on your monthly budget. For many, it represents a significant portion of their discretionary income, and sometimes even their essential expenses.

- Budgetary Allocation: Financial advisors often recommend that car-related expenses (payment, insurance, fuel, maintenance) should not exceed a certain percentage of your gross income, commonly cited as the “20/4/10” rule (20% down payment, finance for no more than 4 years, and total car costs not exceeding 10% of gross income). While this rule might be harder to follow with today’s car prices, it underscores the need for a realistic assessment of affordability. A high car payment can force cuts in other areas, such as housing, groceries, or entertainment, or worse, lead to reliance on credit card debt.

- Opportunity Cost: Every dollar allocated to a car payment is a dollar that cannot be used for other financial goals. This is known as opportunity cost. That money could be contributing to an emergency fund, invested for retirement, used to pay down high-interest debt, or saved for a down payment on a house. A higher-than-necessary car payment can significantly delay wealth accumulation and financial independence.

- Debt-to-Income Ratio: Lenders, especially for mortgages and other large loans, scrutinize your debt-to-income (DTI) ratio. Your car loan contributes to your total monthly debt obligations. A high DTI can make it harder to qualify for other loans or lead to less favorable terms, potentially hindering future financial aspirations like homeownership.

The Long-Term Cost of Car Ownership

While the monthly payment is a primary concern, focusing solely on it can obscure the true, long-term cost of owning a vehicle. Car ownership extends far beyond the loan principal and interest.

- Beyond the Loan: The “total cost of ownership” (TCO) encompasses all expenses associated with your vehicle, not just the payment. This includes:

- Insurance: A mandatory and often substantial expense, varying based on vehicle type, driver history, location, and coverage limits.

- Fuel: A variable cost that can significantly add up, especially with rising gas prices and longer commutes.

- Maintenance and Repairs: Regular oil changes, tire rotations, and unexpected repairs are inevitable. Newer cars might have lower initial maintenance costs but eventually require service; older cars often come with higher repair likelihood.

- Depreciation: The decline in a car’s value over time is often the single largest “cost” of ownership, even though it’s not a direct monthly outlay. New cars depreciate rapidly in their first few years.

- Registration and Licensing Fees: Annual or biennial fees required by state governments.

- The Trap of Negative Equity: Longer loan terms, combined with rapid depreciation, increase the risk of negative equity (or being “upside down”). This means you owe more on your car loan than the car is currently worth. If your car is totaled or stolen, insurance might pay out less than you owe, leaving you responsible for the difference. It also makes trading in or selling the vehicle challenging, as you’d have to pay the difference out-of-pocket or roll it into a new loan, perpetuating the cycle of debt. Avoiding negative equity often involves a substantial down payment, choosing shorter loan terms, or purchasing a vehicle that holds its value well.

Strategies for Managing and Reducing Your Car Payment

Given the significant financial impact of a car payment, proactive strategies for managing and potentially reducing this expense are essential. This involves smart planning before you buy and intelligent optimization during and after the purchase.

Before You Buy: Smart Planning and Research

The most impactful decisions regarding your car payment are made before you ever step foot in a dealership. Thorough preparation can save you thousands over the life of your loan.

- Know Your Budget First: Before falling in love with a specific car, establish a firm budget based on your overall financial health, not just what a lender says you can afford. Consider all car-related expenses (payment, insurance, fuel, maintenance) and ensure they fit comfortably within your monthly income without compromising other financial goals. Use online affordability calculators to get a realistic picture.

- Improve Your Credit Score: Your credit score is the single biggest factor determining your interest rate. A higher score (e.g., 720+) grants access to the most favorable rates, significantly reducing your total interest paid and monthly payment. Take time to review your credit report for errors and work on improving your score by paying bills on time and reducing other debts before applying for a car loan.

- Save for a Larger Down Payment: Aim for a down payment of at least 20% for a new car and 10% for a used car. A substantial down payment reduces the principal amount borrowed, leading to lower monthly payments and less interest accrual. It also helps to prevent negative equity.

- Research Vehicle Values and Total Cost of Ownership (TCO): Don’t just look at the sticker price. Research the actual transaction prices for the vehicle you’re interested in, taking into account market demand. More importantly, research the TCO for different models, factoring in expected depreciation, insurance costs, fuel efficiency, and typical maintenance expenses. A slightly more expensive car upfront might be cheaper over five years if it’s more fuel-efficient and reliable.

- Shop for Financing First (Pre-Approval): Obtain pre-approval from multiple banks, credit unions, and online lenders before visiting a dealership. This gives you a concrete interest rate offer, which you can then use as leverage to negotiate with the dealership’s finance department. It separates the car-buying process from the loan-getting process, reducing pressure and allowing you to focus on getting the best deal on each.

- Negotiate the Price, Not Just the Payment: Dealerships often try to focus on the monthly payment to make a car seem affordable. Always negotiate the total price of the car first. A lower selling price will naturally result in a lower monthly payment, regardless of the loan terms. Be wary of extended loan terms or add-ons that inflate the total cost in exchange for a slightly lower perceived monthly payment.

During and After Purchase: Optimizing Your Loan

Even after you’ve purchased a car, there are still opportunities to manage and potentially reduce your car payment or the overall cost of ownership.

- Refinancing Options: If interest rates have dropped since you bought your car, or if your credit score has significantly improved, consider refinancing your car loan. Refinancing can secure a lower interest rate, which will reduce your monthly payment and/or the total interest paid. Some might even refinance to a shorter loan term to pay off the car faster if their budget allows.

- Paying More Than the Minimum: If your budget allows, making extra payments or rounding up your monthly payment can significantly reduce the total interest you pay and shorten the loan term. Ensure that any extra payments are applied directly to the principal, not just towards future interest.

- Selling Your Current Vehicle Wisely: If you have an existing vehicle, research its market value thoroughly. Selling it privately can often yield a higher price than trading it in at a dealership, which gives you more cash for a down payment on your next vehicle.

- Consider Leasing vs. Buying (with caution): While not for everyone, leasing can sometimes offer lower monthly payments for access to a new car every few years. However, leasing comes with mileage restrictions, wear-and-tear clauses, and no ownership equity, so it’s essential to understand the full financial implications and only consider it if it truly aligns with your lifestyle and financial goals.

Beyond the Averages: Personalizing Your Car Payment Decision

While average car payments offer a useful benchmark, personal finance is inherently personal. What’s affordable for one individual might be a crippling burden for another. Moving beyond statistics to personalize your car payment decision is paramount.

When a Higher Payment Might Be Acceptable (and When Not)

A higher car payment isn’t inherently bad, nor is a lower one always good. The appropriateness depends entirely on your financial situation and priorities.

- When It Might Be Acceptable:

- High and Stable Income: If you have a significantly higher-than-average, stable income with ample disposable cash, a higher payment might be manageable without impacting other financial goals.

- Minimal Other Debts: If you have no credit card debt, student loans, or mortgage, you have more bandwidth to allocate towards a car payment.

- Specific Needs: If a particular vehicle is essential for your business, a specialized hobby, or provides critical safety features for your family, and you can truly afford it, a higher payment might be justifiable.

- Strong Savings: If you have a robust emergency fund and are consistently contributing to retirement and other long-term savings, a higher payment might be a conscious choice.

- When It’s a Warning Sign:

- Stretching Your Budget: If the car payment requires you to cut back on essential expenses (food, housing, healthcare) or consistently dips into your savings.

- Sacrificing Financial Goals: If a high payment prevents you from building an emergency fund, saving for retirement, or paying off high-interest debt.

- Relying on Longer Terms: If you’re only able to afford a car by stretching the loan to 72 or 84 months, you’re likely buying more car than you can truly afford, increasing total interest and the risk of negative equity.

- No Down Payment or Negative Equity: Rolling negative equity from a previous car into a new loan or buying with zero down indicates financial strain and a dangerous cycle of debt.

The Role of Financial Goals and Priorities

Your car payment decision should always align with your broader financial goals and priorities. Is your primary goal to be debt-free quickly? To save for a down payment on a house? To retire early? To invest aggressively?

- Debt-Free Living: If you prioritize becoming debt-free, a higher car payment might detract from this goal. You might consider an older, less expensive car, or pay off your current vehicle aggressively.

- Investing for Retirement vs. Luxury Vehicle: Every extra dollar spent on a car payment is a dollar not invested. Over decades, the compounding returns on even a modest investment can far outstrip the pleasure of a more luxurious car. Consider the long-term impact on your net worth.

- Emergency Fund Importance: Before committing to a large car payment, ensure you have a fully funded emergency fund (3-6 months of living expenses). Unexpected car repairs or job loss can quickly turn an “affordable” payment into a financial crisis without this safety net.

Tools and Resources for Smart Car Financing

Leveraging available tools and resources can significantly enhance your decision-making process.

- Online Calculators: Utilize online car loan calculators to estimate monthly payments based on different vehicle prices, interest rates, and loan terms. Affordability calculators can help you determine how much car you can truly afford based on your income and expenses.

- Credit Score Monitoring Services: Regularly check your credit score and report through services like Credit Karma, Experian, or your bank. Understanding your credit health is crucial for securing the best interest rates.

- Financial Advisors: For complex financial situations or major purchases, consulting a certified financial advisor can provide personalized guidance and help you integrate car ownership into your overall financial plan.

- Automotive Research Sites: Websites like Edmunds, Kelley Blue Book (KBB), and Consumer Reports offer invaluable data on vehicle pricing, reliability, total cost of ownership, and reviews, helping you choose a car that aligns with your budget and needs.

Conclusion

The average car payment in America is a statistic that tells a story of evolving market conditions, rising vehicle prices, and the ongoing financial commitments faced by consumers. While current averages for new cars hover around $700-$750 and used cars around $500-$550, these numbers are just starting points. The true financial impact of a car payment is deeply personal, shaped by individual creditworthiness, down payment strategies, loan terms, and a host of other factors.

Making an informed decision about your car payment requires moving beyond these averages to conduct thorough research, plan meticulously, and align your choices with your unique financial situation and long-term goals. By understanding the key factors that influence payments, recognizing the full spectrum of ownership costs, and employing smart strategies for financing, you can secure reliable transportation without derailing your financial well-being. Ultimately, the goal is not just to afford a car, but to afford it wisely, ensuring it enhances rather than hinders your journey towards financial security.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.