Navigating the world of car loans can often feel like deciphering a complex financial puzzle. Among the most crucial pieces of this puzzle is the Annual Percentage Rate (APR). Far more than just an interest rate, your car loan APR is a comprehensive measure of the true cost of borrowing, encompassing not only the interest but also various fees associated with the loan. Understanding what APR is, how it’s calculated, and what factors influence it is paramount for any prospective car buyer aiming to make a financially sound decision. In an era where vehicle prices continue to rise, securing a favorable APR can translate into thousands of dollars in savings over the life of your loan, making it a cornerstone of smart personal finance management when acquiring a new set of wheels. This article will delve deep into the mechanics of car loan APR, offering insights and strategies to empower you on your car buying journey.

Understanding the Fundamentals of Car Loan APR

The Annual Percentage Rate (APR) is a critical concept in personal finance, particularly when it comes to borrowing money for significant purchases like a car. It’s often misunderstood, leading many consumers to focus solely on the interest rate, missing the broader financial implications of their loan. Grasping the true definition and components of APR is the first step toward becoming a more informed borrower.

Defining APR: More Than Just Interest

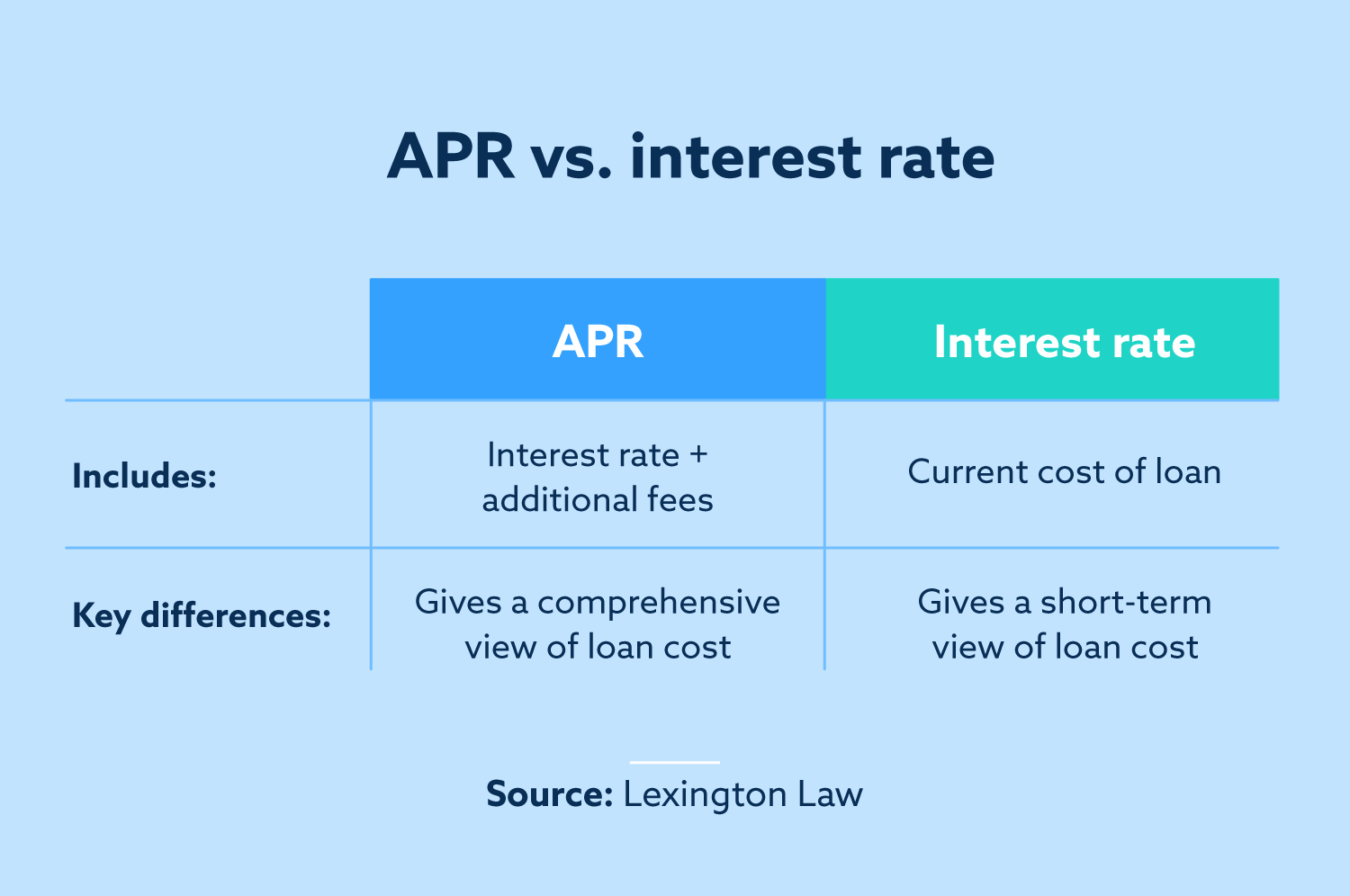

At its core, APR represents the annual cost of borrowing money, expressed as a percentage. While it certainly includes the interest rate, it’s a more encompassing figure. The interest rate is simply the percentage charged by the lender for the use of their money. APR, however, takes this a step further by incorporating other fees and charges that you might incur over the loan’s term. These can include origination fees, administrative costs, closing costs, and sometimes even points. The intention behind APR is to provide consumers with a standardized way to compare the true cost of different loan offers, giving them a more accurate picture than just the advertised interest rate alone. Without APR, comparing loans would be akin to comparing apples and oranges, as different lenders might structure their fees in varying ways.

The Components That Make Up Your APR

To fully appreciate the APR, it’s essential to understand its constituent parts. Primarily, the APR is driven by the interest rate – the charge for borrowing the principal amount. This is typically the largest component. However, lenders may also include various fees that are rolled into the total cost of the loan, thereby increasing the effective annual rate. Common fees that can be factored into APR for car loans include:

- Origination Fees: A fee charged by the lender for processing the loan application.

- Documentation Fees: Costs associated with preparing and handling loan documents.

- Underwriting Fees: Charges for evaluating and approving the loan.

- Processing Fees: General administrative fees for managing the loan.

It’s important to note that not all fees are always included in the APR calculation. For instance, late payment fees, prepayment penalties (less common in car loans but still possible), or fees for optional services like credit protection might not be reflected in the APR but will still add to the overall cost of the loan if incurred. Therefore, a careful review of the loan disclosure statement is always advisable to identify all potential costs.

Why APR Matters: The True Cost of Borrowing

Focusing solely on the monthly payment or a quoted interest rate can be deceptive. A low monthly payment might be achieved through a longer loan term, which often leads to a higher overall cost due to more interest accrual over time. Similarly, two lenders might offer the same interest rate, but if one has higher fees bundled into its APR, that loan will ultimately be more expensive.

Consider two hypothetical car loans, both for $30,000 over 60 months.

- Loan A: 5% interest rate, 0.5% origination fee. Let’s say this results in an effective APR of 5.2%.

- Loan B: 5% interest rate, 1.5% origination fee. This could result in an effective APR of 5.8%.

While the interest rate is identical, Loan B, with its higher fees reflected in the APR, will cost you more over the loan’s life. This difference, though seemingly small in percentage points, can amount to hundreds or even thousands of dollars in additional costs depending on the loan amount and term. By providing a standardized benchmark, APR empowers consumers to make direct, apples-to-apples comparisons between various loan products, ensuring they understand the true financial commitment before signing on the dotted line.

Factors Influencing Your Car Loan APR

While you might hope for the lowest possible APR on your car loan, several critical factors come into play that determine the rate you ultimately qualify for. Lenders assess risk, and your APR is a direct reflection of that assessment. Understanding these influences can help you proactively position yourself for a more favorable rate.

Your Credit Score: The Primary Driver

Without a doubt, your credit score is the single most significant factor influencing your car loan APR. Lenders use your credit score as a snapshot of your financial responsibility and ability to repay debt.

- Excellent Credit (720+ FICO): Individuals with strong credit histories, consistent on-time payments, and low debt-to-income ratios are perceived as low-risk borrowers. They typically qualify for the lowest available APRs, enjoying the best terms.

- Good Credit (660-719 FICO): Borrowers in this range can still secure competitive rates, though they might be slightly higher than those with excellent credit.

- Fair Credit (600-659 FICO): This tier often sees moderately higher APRs. Lenders might view these borrowers with some caution due to past credit challenges or limited credit history.

- Poor Credit (Below 600 FICO): For those with poor credit, obtaining a car loan can be challenging, and the APRs will be significantly higher to compensate lenders for the increased risk. Subprime lenders specialize in this market, but at a substantial cost.

Improving your credit score before applying for a loan can drastically reduce the APR you’re offered, saving you a considerable amount over the loan’s term.

Loan Term and Down Payment: Striking a Balance

The length of your loan and the amount of money you put down upfront also play crucial roles in determining your APR.

- Loan Term: Shorter loan terms (e.g., 36 or 48 months) generally come with lower APRs than longer terms (e.g., 72 or 84 months). This is because a shorter term means the lender is exposed to risk for a shorter period, and the overall interest paid is less. While longer terms offer lower monthly payments, they often result in a higher overall cost due to the higher APR and extended interest accrual.

- Down Payment: A substantial down payment reduces the amount you need to borrow, thereby decreasing the lender’s risk. Lenders are more inclined to offer lower APRs to borrowers who demonstrate financial commitment through a significant down payment. It also helps prevent you from being “upside down” on your loan (owing more than the car is worth) early on.

Vehicle Type and Age: Risk Assessment for Lenders

The characteristics of the vehicle itself can influence your APR.

- New vs. Used Cars: New cars often come with lower APRs, sometimes even promotional rates from manufacturers, due to their higher reliability and predictable depreciation. Used cars, particularly older models, generally carry higher APRs because they pose a greater risk of mechanical issues, have less predictable resale values, and might be harder to repossess and sell if the borrower defaults.

- Luxury vs. Economy: While less direct, lenders might also factor in the type of vehicle. Niche or high-end luxury vehicles can sometimes have different APR considerations due to their specialized market or higher repair costs.

Market Interest Rates and Economic Conditions

Beyond your personal financial profile and the vehicle, broader economic factors also influence the prevailing APRs. The Federal Reserve’s monetary policy, inflation rates, and the general health of the economy dictate the base interest rates at which lenders borrow money. When the Federal Reserve raises its benchmark rates, commercial banks and credit unions typically follow suit, leading to higher APRs across the board for consumers, including car loans. Conversely, in a low-interest-rate environment, car loan APRs tend to be more competitive.

Lender Type: Banks, Credit Unions, and Dealerships

Where you get your loan can also impact your APR.

- Banks: Large national and regional banks are common sources for car loans, offering competitive rates to well-qualified borrowers.

- Credit Unions: Often lauded for their member-focused approach, credit unions are non-profit organizations that can sometimes offer lower APRs and more flexible terms than traditional banks due to their cooperative structure.

- Dealerships (Captive Lenders): Dealerships often partner with specific financing arms (e.g., Toyota Financial Services, Ford Credit) or third-party lenders. They can offer convenient one-stop shopping, and sometimes provide promotional rates (0% or very low APR) for new vehicles to incentivize sales, particularly for borrowers with excellent credit. However, for those with less-than-perfect credit, dealership financing might come with higher rates.

Shopping around and comparing offers from multiple types of lenders is crucial to securing the most favorable APR.

Strategies to Secure a Lower Car Loan APR

Understanding the factors that influence your car loan APR is only half the battle. The other half involves actively implementing strategies to improve your chances of securing the lowest possible rate. A proactive approach can significantly reduce the overall cost of your vehicle.

Boost Your Credit Score Before Applying

Given that your credit score is the most significant determinant of your APR, taking steps to improve it before you apply is paramount.

- Pay Bills On Time: Payment history accounts for a large portion of your credit score. Ensure all your bills, especially credit cards and existing loans, are paid punctually.

- Reduce Debt: Lowering your credit utilization ratio (the amount of credit you’re using compared to your total available credit) can positively impact your score. Pay down credit card balances.

- Check Your Credit Report: Obtain free copies of your credit report from Equifax, Experian, and TransUnion. Review them for errors and dispute any inaccuracies, as these could be dragging down your score.

- Avoid New Credit Inquiries: Limit opening new credit accounts in the months leading up to your car loan application, as multiple hard inquiries can temporarily lower your score.

Shop Around: Get Multiple Loan Offers

Never settle for the first loan offer you receive, especially from a dealership.

- Pre-Approval from Multiple Lenders: Apply for pre-approval from at least three different lenders (banks, credit unions, online lenders) within a short window (typically 14-45 days, depending on the scoring model). This counts as a single hard inquiry on your credit report for scoring purposes, allowing you to compare offers without further damaging your score.

- Compare APRs, Not Just Monthly Payments: Focus on the APR as the most accurate measure of the loan’s true cost. A lower APR means less interest paid over time.

- Use Dealership Financing as Leverage: If a dealership offers financing, you’ll have pre-approved offers to compare it against, giving you stronger negotiation power.

Make a Sizable Down Payment

A larger down payment reduces the amount you need to borrow and signals to lenders that you are a lower-risk borrower.

- Reduce Principal: Less money borrowed means less interest accrual overall.

- Lower Loan-to-Value (LTV) Ratio: Lenders prefer a lower LTV ratio (the loan amount compared to the car’s value). A substantial down payment reduces this ratio, making the loan less risky for them and potentially qualifying you for a lower APR.

- Avoid Being Upside Down: A larger down payment helps prevent you from owing more on the car than it’s worth, particularly in the early years of ownership when depreciation is highest.

Consider a Shorter Loan Term (If Feasible)

While longer loan terms offer lower monthly payments, they often come with higher APRs and significantly increase the total interest paid over the life of the loan.

- Lower Overall Cost: A shorter term means you pay off the principal faster, reducing the period over which interest accrues. This typically results in a lower total cost for the vehicle.

- Potential for Lower APR: Lenders often offer lower APRs for shorter loan terms because their risk exposure is reduced.

- Assess Affordability: Ensure the higher monthly payments associated with a shorter term fit comfortably within your budget without straining your finances.

Negotiate Beyond the Sticker Price

While directly negotiating your APR might be challenging once an offer is made, negotiating the overall price of the vehicle can indirectly reduce your borrowing costs.

- Reduce Loan Amount: A lower purchase price means you need to borrow less money. Even if your APR remains the same, a smaller principal loan amount will result in lower total interest paid and lower monthly payments.

- Separate Negotiations: It’s often advisable to negotiate the vehicle’s price independently of the financing terms. Once you’ve settled on a price, you can then focus on securing the best financing.

By strategically approaching your car loan application with these tactics, you can significantly enhance your chances of securing a lower APR, ultimately saving you money and contributing to healthier personal finances.

Calculating and Comparing Car Loan APRs

Making an informed decision about your car loan requires more than just looking at the headline APR; it involves understanding how that figure translates into real costs and having the tools to compare different offers effectively. Dissecting the details is crucial for financial prudence.

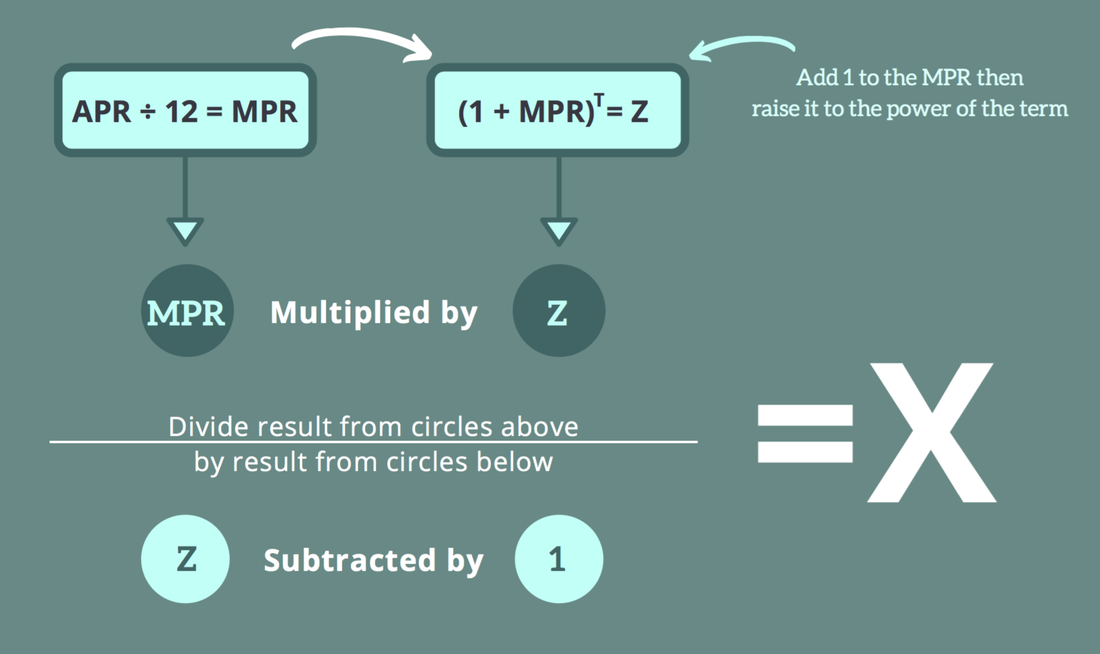

The APR Calculation Formula (Simplified)

While the exact calculation of APR can be complex, involving present value and annuity formulas, the core idea is to annualize the total cost of borrowing, including both interest and certain fees. A simplified way to think about it is that APR is the effective interest rate you’re paying annually over the loan’s term, considering all mandatory charges.

To approximate the impact of fees on APR, imagine a loan with an interest rate of 5% and an origination fee of 1% of the loan amount. If the loan is for one year, the APR would be approximately 6% (5% interest + 1% fee). For longer loans, the fee’s impact is spread out, making the calculation more intricate, but the principle remains: APR combines the direct cost of interest with other lender charges to give you a single, comparable annual rate. Financial regulations, like the Truth in Lending Act (TILA), mandate that lenders disclose the APR to ensure transparency.

Utilizing Online Calculators and Tools

You don’t need to be a mathematician to compare car loan offers. Numerous online tools and calculators can help you understand the impact of different APRs and loan terms.

- Loan Payment Calculators: Input the loan amount, interest rate (or APR), and term to estimate your monthly payments. This helps you understand affordability.

- APR Comparison Tools: Many financial websites and lender platforms offer tools that allow you to plug in different APRs, loan amounts, and terms to see the total cost of the loan, including total interest paid. This is invaluable for comparing offers side-by-side.

- Total Cost Calculators: Some advanced calculators can factor in down payments, trade-ins, and even sales tax to give you a comprehensive picture of the total cost of ownership over the loan term.

These tools empower you to model various scenarios and determine which loan offer truly aligns with your financial goals.

Reading the Fine Print: Hidden Fees and Terms

While APR is a standardized measure, it doesn’t encompass every potential cost or condition of a loan. It’s imperative to meticulously review the entire loan agreement before signing.

- Fees Not Included in APR: Be vigilant for fees that might not be rolled into the APR, such as late payment fees, prepayment penalties (less common with car loans but still possible), title transfer fees, registration fees, or charges for optional add-ons like extended warranties or GAP insurance (which, while useful, are often better purchased separately).

- Loan Covenants: Understand any specific conditions or requirements imposed by the lender.

- Prepayment Penalties: Confirm whether paying off your loan early incurs a penalty. While less common for simple interest car loans, some contracts might have them.

- Balloon Payments: Rarely for standard car loans, but be aware if your loan structure includes a large lump-sum payment at the end of the term.

A thorough review ensures there are no surprises down the road and that you fully comprehend your financial obligations.

Pre-Qualification vs. Pre-Approval

When shopping for a car loan, you’ll encounter the terms “pre-qualification” and “pre-approval.” Understanding the difference is crucial for effective loan comparison.

- Pre-Qualification: This is a preliminary assessment based on a soft credit inquiry (which doesn’t affect your credit score) and the financial information you provide. It gives you an estimate of what you might qualify for and at what approximate APR. It’s a good starting point for gauging your eligibility.

- Pre-Approval: This is a more definitive offer from a lender. It involves a hard credit inquiry (which may slightly ding your credit score temporarily) and a comprehensive review of your financial standing. A pre-approval provides a specific loan amount, APR, and terms that the lender is genuinely willing to offer you. This is what you need to confidently shop for a car and negotiate financing, as it’s a firm offer.

Always aim for pre-approval from multiple lenders to have concrete offers in hand, which significantly strengthens your position when negotiating with a dealership.

Refinancing Your Car Loan: A Second Chance at a Better APR

Securing a car loan is a significant financial commitment, but it’s not always set in stone. Market conditions change, and your financial profile can improve over time, opening up opportunities to revisit your loan terms through refinancing. Refinancing a car loan means taking out a new loan to pay off your existing one, ideally at a lower APR or with more favorable terms.

When to Consider Refinancing

Refinancing your car loan isn’t for everyone, but there are several scenarios where it makes sound financial sense:

- Improved Credit Score: If your credit score has significantly improved since you initially took out the loan, you’re likely to qualify for a lower APR today. Timely payments on your current loan, reducing other debts, or resolving past credit issues can all contribute to a better score.

- Lower Market Interest Rates: If general interest rates have fallen since you financed your car, you might be able to secure a new loan at a lower APR than your original.

- Desire for Different Loan Terms: You might want to refinance to extend your loan term to reduce monthly payments (though this often means more interest paid overall) or shorten it to pay off the car faster and save on total interest.

- Too High an Original APR: Perhaps you rushed into the original loan, didn’t shop around, or had poor credit at the time, resulting in a very high APR. Refinancing can be a “do-over” to correct that.

- Remove a Co-signer: If you initially needed a co-signer but your credit has since improved, refinancing can allow you to take sole responsibility for the loan.

The Refinancing Process

Refinancing a car loan is similar to applying for a new one, but with your existing loan as the item being paid off:

- Assess Your Current Loan: Gather all the details of your existing loan: current balance, APR, monthly payment, and remaining term.

- Check Your Credit Score: Ensure your credit profile is strong enough to warrant a better offer.

- Shop for New Lenders: Approach banks, credit unions, and online lenders for pre-approval offers. Compare their proposed APRs, fees, and terms.

- Submit an Application: Once you choose a lender, complete their application, providing necessary documentation like income verification and vehicle information.

- New Loan Pays Off Old Loan: If approved, the new lender will pay off your original car loan. Your new payments will then be made to the new lender at the new terms.

Potential Benefits and Drawbacks

Refinancing can offer significant advantages, but it’s crucial to weigh the pros against potential cons:

Benefits:

- Lower APR: The most common reason, leading to substantial savings on interest over the loan’s life.

- Lower Monthly Payments: Achieved through a lower APR or by extending the loan term, freeing up cash flow.

- Reduced Total Interest Paid: A lower APR or shorter term means less money goes to interest.

- Simplified Finances: If you consolidate multiple car loans, it can simplify your monthly budgeting.

Drawbacks:

- Potential Fees: The new loan might come with its own set of origination or processing fees, which could offset some of the savings.

- Extending Loan Term: While it lowers monthly payments, extending the term means you’ll pay interest for longer, potentially increasing the total cost of the loan even with a lower APR.

- Negative Equity: If you owe more than your car is worth (negative equity), refinancing can be challenging, as lenders are hesitant to lend more than the vehicle’s value.

- Impact on Credit Score: A hard credit inquiry for the new loan will temporarily impact your score.

Carefully calculate the total costs and savings before making the decision to refinance, ensuring it genuinely improves your financial standing.

Empowering Your Car Buying Journey

Understanding the Annual Percentage Rate (APR) for car loans is far more than an academic exercise; it’s a fundamental pillar of smart personal finance that directly impacts your wallet. From recognizing that APR encapsulates more than just the interest rate to knowing how your credit score, loan term, and even the vehicle type influence the rate you’re offered, being informed is your greatest asset.

By proactively boosting your credit score, diligently shopping around for pre-approved offers from various lenders, and making a strategic down payment, you position yourself to secure the most favorable terms. Remember to leverage online calculators to compare the true cost of different loans and always scrutinize the fine print to avoid hidden fees. Even after a loan is secured, the option to refinance provides a valuable second chance to optimize your financial commitment should your circumstances or market conditions change.

In a world where car prices and interest rates can fluctuate significantly, being an empowered consumer means taking control of your financial decisions. Your car is a major investment, and understanding its financing is key to ensuring it enhances, rather than burdens, your financial well-being. By applying the insights shared here, you can navigate the complexities of car loans with confidence, making choices that save you money and pave the way for a healthier financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.