The phrase “annual deductible” often surfaces in discussions about insurance, particularly health insurance, but its implications extend far beyond healthcare and touch upon various aspects of personal finance, financial tools, and even brand perception. Understanding what an annual deductible is, how it functions, and how it impacts your financial planning is crucial for making informed decisions and building a robust financial safety net.

Decoding the Deductible: Your First Line of Financial Defense

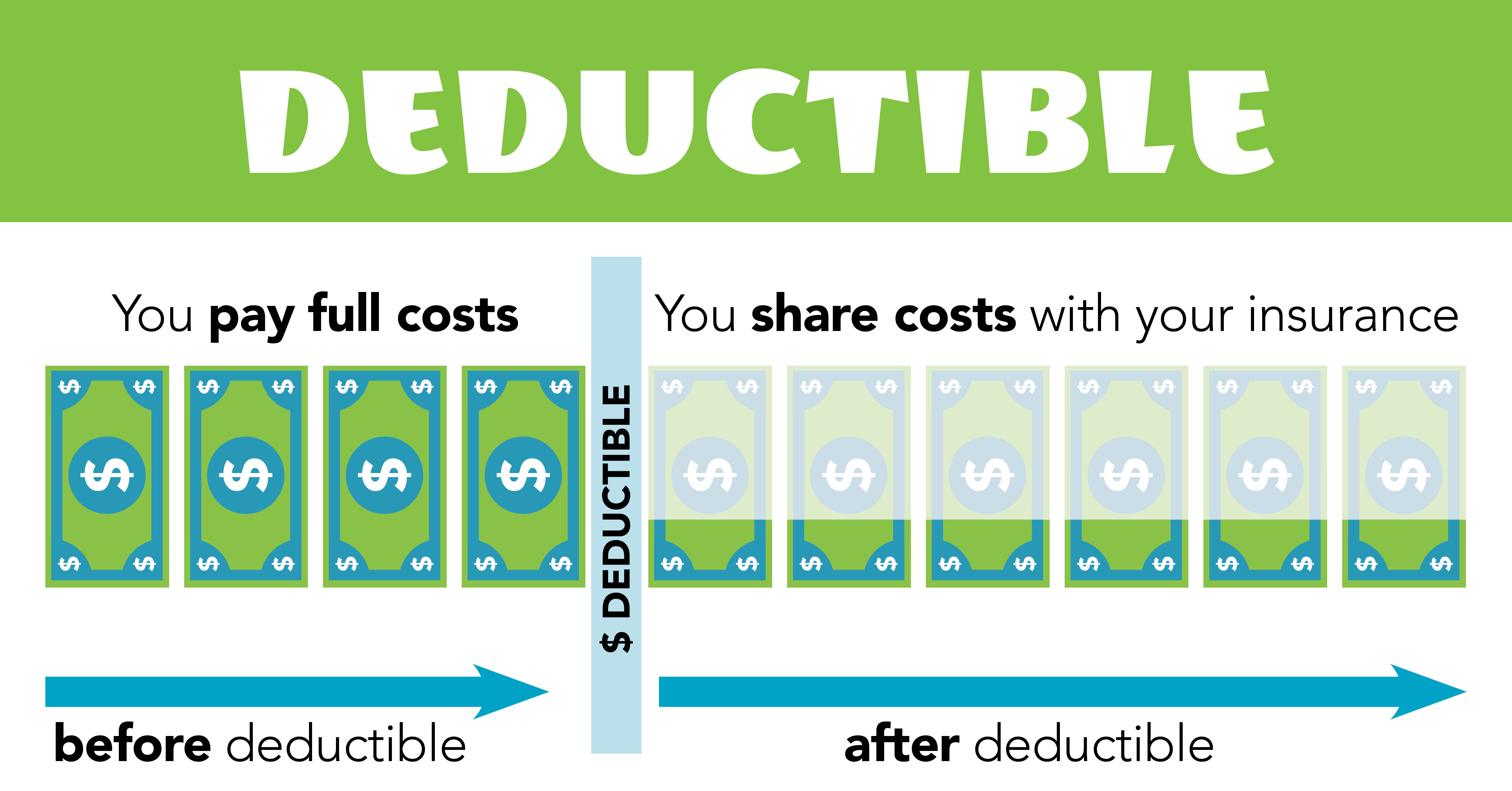

At its core, an annual deductible is the amount of money you agree to pay out-of-pocket for covered healthcare services before your insurance plan begins to pay. Think of it as the initial threshold you must cross before your insurance benefits truly kick in. This concept is foundational to many insurance policies, including health, auto, homeowners, and even some types of business insurance. While the context might change, the fundamental principle remains the same: you bear a specific financial responsibility before the insurer steps in.

The Mechanics of How Deductibles Work

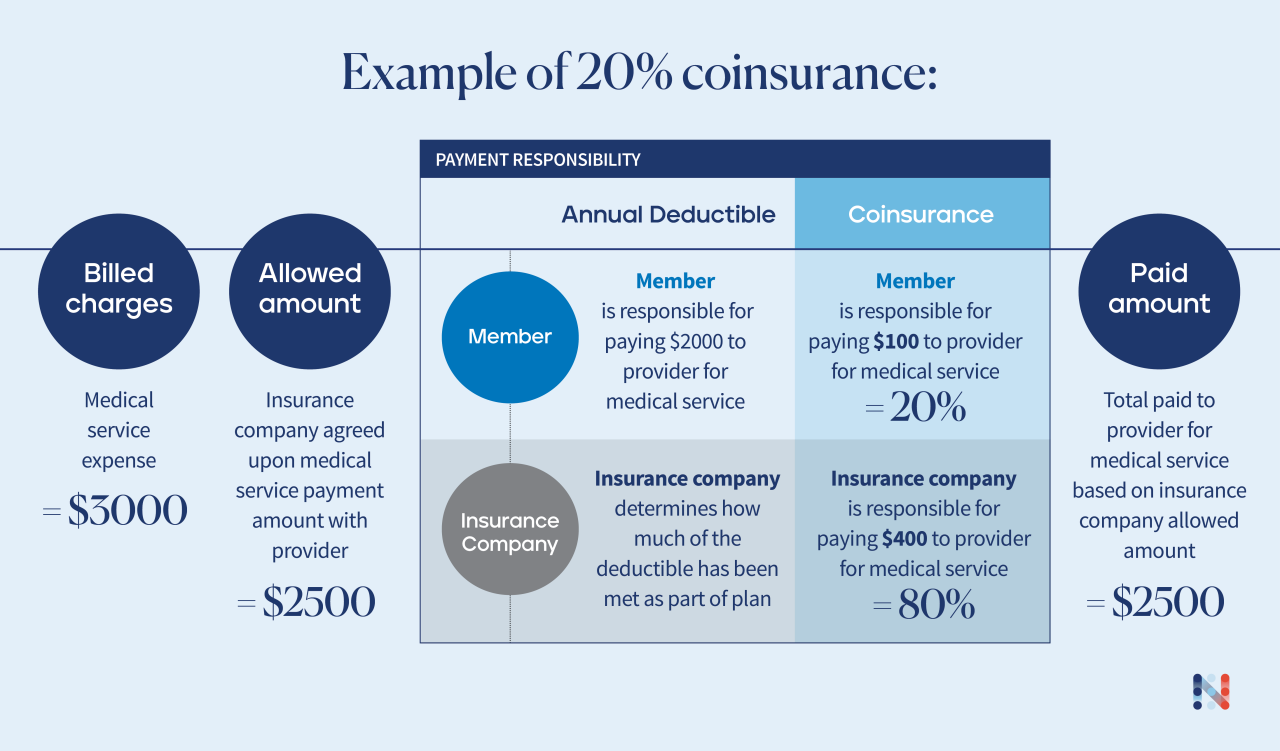

Let’s break down the mechanics of an annual deductible. Imagine you have a health insurance plan with an annual deductible of $1,000. This means that for any covered medical expenses incurred within a policy year (typically 12 months), you are responsible for paying the first $1,000 yourself. Once you have paid this $1,000, your insurance coverage then begins to contribute to the remaining costs.

Example:

- You have a doctor’s visit that costs $200. Since this is less than your $1,000 deductible, you pay the full $200 out-of-pocket. You still have $800 remaining on your deductible.

- Later in the year, you have a surgical procedure that costs $5,000. You’ve already paid $200, so you will pay the next $800 to meet your $1,000 deductible.

- After you’ve paid the remaining $800, your insurance plan will now start covering its share of the subsequent costs. For example, if your plan has an 80/20 coinsurance, your insurer would pay 80% of the remaining $4,200 ($5,000 – $800 = $4,200), which is $3,360, and you would pay your 20% share, which is $840. In this scenario, your total out-of-pocket for the surgery would be $800 (to meet deductible) + $840 (your coinsurance share) = $1,640.

It’s important to note that deductibles are “annual.” This means they reset at the beginning of each policy year. The expenses you pay towards your deductible in one year do not carry over to the next.

Key Terms Related to Deductibles

Understanding deductibles also requires familiarity with related insurance terminology:

- Premium: This is the regular payment you make to maintain your insurance coverage, usually monthly. A higher deductible often correlates with a lower premium, and vice-versa.

- Copayment (Copay): This is a fixed amount you pay for a covered healthcare service after you’ve met your deductible. For example, you might have a $20 copay for each doctor’s visit or a $50 copay for an emergency room visit.

- Coinsurance: This is your share of the costs of a covered healthcare service, calculated as a percentage (e.g., 20%) of the allowed amount for the service. You pay coinsurance after you’ve met your deductible.

- Out-of-Pocket Maximum: This is the most you will have to pay for covered services in a policy year. Once you reach this limit, your health insurance plan pays 100% of the allowed amount for covered benefits for the rest of the year. The annual deductible is a component of this out-of-pocket maximum.

Strategic Financial Planning and the Annual Deductible

The concept of an annual deductible is not just an insurance detail; it’s a significant factor in personal finance, particularly for budgeting and risk management. Your chosen deductible level directly impacts your immediate cash flow and your potential financial exposure in case of an unforeseen event.

Choosing the Right Deductible for Your Budget and Risk Tolerance

When selecting an insurance plan, you’ll often be presented with a range of deductible options. This decision is a balancing act between your monthly expenses and your ability to absorb a significant one-time cost.

- High Deductible, Low Premium: Opting for a higher deductible typically means you’ll pay a lower monthly premium. This can be an attractive option if you are generally healthy, have a strong emergency fund, and are comfortable taking on more financial risk in exchange for lower ongoing costs. It requires disciplined saving to ensure you can cover the deductible if needed.

- Low Deductible, High Premium: Conversely, a lower deductible results in a higher monthly premium. This is often preferred by individuals or families who anticipate frequent medical needs or prefer the security of knowing their out-of-pocket expenses will be capped at a lower amount relatively quickly. This option offers more predictable costs but at a higher recurring expense.

Your financial planning strategy should consider:

- Your Emergency Fund: Can you realistically afford to pay your deductible if an unexpected medical bill arises tomorrow? If not, a lower deductible might be a safer choice, or you’ll need to prioritize building your emergency savings.

- Your Health Status and Family Needs: Do you or your family members have chronic conditions requiring regular medical attention? Or are you generally healthy with infrequent doctor visits? The former might lean towards a lower deductible, while the latter might benefit from a higher one.

- Your Income Stability: If your income is variable or prone to fluctuations, a higher deductible might be too risky.

The Deductible as a Financial Tool: Budgeting and Saving

The annual deductible serves as a crucial anchor for your financial planning. It compels you to think about potential large expenses and to prepare for them.

- Budgeting for the Unexpected: When you select an insurance plan, you should actively incorporate the potential deductible amount into your budget as a savings goal. This isn’t a monthly expense like a premium, but rather a sum you need to have accessible. Consider it a self-insurance component of your financial strategy.

- The Role of Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs): For health insurance, the concept of a deductible is closely linked to tax-advantaged savings accounts.

- Health Savings Accounts (HSAs): These are often paired with High-Deductible Health Plans (HDHPs). Contributions to an HSA are tax-deductible, the money grows tax-free, and withdrawals for qualified medical expenses are also tax-free. This allows you to save specifically for your deductible and other medical costs in a tax-efficient manner.

- Flexible Spending Accounts (FSAs): These accounts, often offered by employers, allow you to set aside pre-tax money from your paycheck to pay for qualified medical expenses. While they offer similar tax advantages, FSAs typically have a “use-it-or-lose-it” policy, meaning you generally must spend the funds within the plan year or by a grace period.

Using these tools can significantly mitigate the financial burden of meeting your annual deductible, making higher-deductible plans more accessible and financially viable for many.

Beyond Health Insurance: Deductibles in Other Financial Arenas

While most commonly associated with health insurance, the principle of an annual deductible is present in other forms of insurance, influencing how we manage risk and protect our assets.

Auto Insurance Deductibles: Protecting Your Vehicle

Your auto insurance policy will likely include deductibles for collision and comprehensive coverage.

- Collision Deductible: This is the amount you pay out-of-pocket if your car is damaged in a collision with another vehicle or object.

- Comprehensive Deductible: This covers damages to your vehicle not caused by a collision, such as theft, vandalism, fire, or natural disasters.

Similar to health insurance, you’ll often have a choice between a higher deductible (lower premium) and a lower deductible (higher premium). The decision often hinges on the value of your vehicle, your driving habits, and your comfort level with financial risk. For an older, less valuable car, a higher deductible might make sense, as the cost to repair could exceed the car’s worth. For a newer, more expensive vehicle, a lower deductible might offer better protection.

Homeowners and Renters Insurance: Safeguarding Your Property

Homeowners and renters insurance policies also feature deductibles, typically for specific types of covered perils.

- Standard Deductible: This applies to most covered damages, such as those from fire, windstorms, or theft.

- Specific Peril Deductibles: Some policies may have separate, often higher, deductibles for specific events like hurricanes, hail, or earthquakes, reflecting the increased risk associated with these events in certain regions.

Choosing your deductible level here involves assessing the value of your property, your risk of experiencing a covered peril, and your ability to pay for repairs or replacements out of pocket.

The Brand and Reputation Aspect of Deductible Choices

While not a direct financial calculation, the choices you make regarding deductibles can subtly reflect on your financial prudence and risk management, which can, in turn, indirectly influence how you’re perceived.

Perceived Financial Savvy and Risk Management

A well-thought-out decision regarding your annual deductible – whether it’s choosing a higher one with a robust emergency fund or a lower one for peace of mind – can signal a mature approach to financial planning. Conversely, being caught unprepared for a deductible can expose financial vulnerabilities.

- For Individuals: Demonstrating the capacity to manage potential out-of-pocket expenses can contribute to a perception of financial responsibility and stability.

- For Businesses: For small businesses, understanding and effectively managing deductibles for property, liability, or cyber insurance is crucial for maintaining operational continuity and financial health. This prudent approach can bolster confidence among stakeholders, investors, and partners.

The Long-Term Financial Health and Brand of Your Finances

Your deductible choices are part of a larger financial picture. Consistently making sound decisions about insurance coverage, emergency savings, and budgeting for potential deductibles contributes to the overall “brand” of your personal finances. This brand is built on consistency, foresight, and the ability to weather financial storms. Over time, this proactive approach can lead to greater financial security, reduce stress, and provide a solid foundation for achieving long-term financial goals.

In conclusion, the annual deductible is far more than a mere insurance term; it’s a fundamental concept in financial literacy. It empowers individuals and businesses to understand their financial responsibilities, make informed choices about risk management, and build robust financial strategies. By grasping the nuances of deductibles and their interplay with premiums, copays, coinsurance, and savings vehicles, you can effectively navigate your insurance landscape and strengthen your overall financial well-being.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.