For anyone entering the world of personal finance and investing, the term “S&P 500” is inescapable. It is cited daily on news broadcasts, discussed in boardroom meetings, and forms the bedrock of millions of retirement accounts. But for the uninitiated, it can often feel like just another piece of financial jargon. Understanding the S&P 500—what it represents, how it functions, and how you can use it to build wealth—is perhaps the most important step any investor can take toward financial literacy.

The Standard & Poor’s 500, commonly known as the S&P 500, is a stock market index that tracks the performance of 500 of the largest companies listed on stock exchanges in the United States. It is widely regarded as the best single gauge of large-cap U.S. equities and a primary barometer for the health of the American economy. Unlike the Dow Jones Industrial Average, which only tracks 30 companies, the S&P 500 offers a much broader and more accurate reflection of the market’s overall movement.

Understanding the Mechanics: How the S&P 500 Works

To appreciate the S&P 500 as a financial tool, one must first understand that it is an “index”—a statistical measure of change in a representative group of individual data points. In this case, those data points are the stock prices of 500 massive corporations. However, the S&P 500 is not a simple average; it is a complex, curated list managed by the S&P Dow Jones Indices.

Market-Cap Weighting Explained

The S&P 500 is a float-adjusted, market-capitalization-weighted index. This means that companies with higher market values (market cap) have a greater impact on the index’s performance than smaller companies. Market capitalization is calculated by multiplying the current stock price by the number of outstanding shares.

In a market-cap-weighted system, if a trillion-dollar company like Apple or Microsoft sees a 2% increase in its stock price, it will move the entire index much more significantly than a 2% move from a company at the bottom of the list. This structure is intended to reflect the actual economic impact of these companies; larger businesses have more influence over the economy, so they have more influence over the index.

The Selection Process and Criteria

A common misconception is that the S&P 500 is simply the 500 largest companies in America. In reality, a committee at S&P Dow Jones Indices selects the constituents based on specific eligibility criteria. This ensures the index remains a high-quality representation of the investable universe. To be considered, a company must:

- Be a U.S.-based corporation.

- Have a market capitalization of at least $15.8 billion (this threshold is adjusted periodically).

- Maintain high liquidity (the shares must be easy to buy and sell).

- Have a public float of at least 10% of its shares.

- Show positive earnings over the most recent quarter and the sum of the previous four quarters.

Sector Representation

The index is designed to span all sectors of the economy. While Technology currently dominates a large portion of the weighting, the S&P 500 also includes Healthcare, Financials, Consumer Discretionary, Communication Services, Industrials, Consumer Staples, Energy, Utilities, Real Estate, and Materials. This diversity is what makes the index a reliable proxy for the broader business cycle.

Why the S&P 500 Matters to Your Personal Finance

For the individual investor, the S&P 500 is more than just a news headline; it is a powerful vehicle for wealth creation. Historically, the index has been the “gold standard” against which all other investments are measured. If a professional hedge fund manager cannot “beat the S&P 500,” they are often considered to have failed their clients.

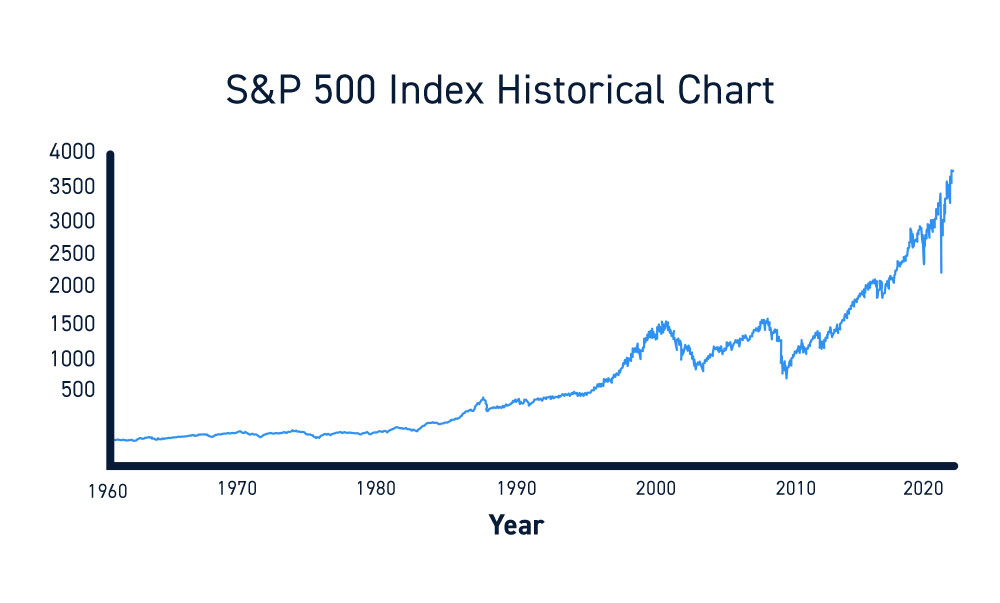

Historical Performance and the Power of Compounding

Over the last several decades, the S&P 500 has provided an average annual return of approximately 10% before inflation. While the market does not go up every year—it can experience significant drops during recessions—the long-term trajectory has been consistently upward.

For someone focused on personal finance, the S&P 500 represents the most efficient way to capture the growth of the American corporate world. By investing in the index, you are essentially betting on the collective ingenuity and profitability of the 500 most successful companies in the country. Over twenty or thirty years, the power of compounding these 10% average returns can turn modest monthly savings into a substantial “nest egg” for retirement.

The Benchmark for Risk and Reward

The S&P 500 serves as a “benchmark.” When you look at your own investment portfolio, you should compare its performance to the S&P 500. If you are taking on the risk of picking individual stocks but your returns are lower than the index, you are taking on more work and more risk for less reward. For many, this realization leads to the “passive investing” philosophy: if you can’t beat the index, simply own the index.

Inflation Hedge

Because the S&P 500 consists of companies that sell goods and services, it naturally acts as a hedge against inflation. When prices rise across the economy, these companies often raise their prices to maintain profit margins. As their profits grow in nominal terms, their stock prices tend to follow, helping investors preserve the purchasing power of their capital over long horizons.

How to Invest: Financial Tools and Strategies

You cannot “buy” the S&P 500 index itself because it is merely a list and a mathematical formula. However, the financial industry has created specific products that allow you to invest in a fund that mimics the index perfectly. These are known as Index Funds and Exchange-Traded Funds (ETFs).

Index Mutual Funds vs. ETFs

The two primary ways to gain exposure to the S&P 500 are through Mutual Funds and ETFs.

- Index Mutual Funds: These are purchased directly from a fund provider (like Vanguard or Fidelity). They are typically traded only once a day after the market closes. They are excellent for automatic, recurring investments from a paycheck.

- ETFs: These trade on an exchange just like individual stocks. You can buy and sell them throughout the trading day. ETFs are often preferred by investors for their tax efficiency and flexibility.

Popular Financial Tools for Investors

Several major financial institutions offer S&P 500 tracking funds with extremely low fees. In the world of personal finance, minimizing fees (expense ratios) is crucial, as high fees can eat away at your returns over time. Popular options include:

- SPY (SPDR S&P 500 ETF Trust): The first and oldest ETF, often used by institutional traders.

- VOO (Vanguard S&P 500 ETF): Known for its incredibly low expense ratio, making it a favorite for long-term retail investors.

- IVV (iShares Core S&P 500 ETF): Another highly liquid, low-cost option from BlackRock.

- FXAIX (Fidelity 500 Index Fund): A mutual fund option often found in 401(k) plans.

The Strategy of Dollar-Cost Averaging

Because the S&P 500 can be volatile in the short term, many financial advisors recommend “Dollar-Cost Averaging” (DCA). Instead of trying to time the market and buy at the “perfect” moment, you invest a fixed amount of money at regular intervals (e.g., $500 every month). This ensures that you buy more shares when prices are low and fewer when prices are high, resulting in a favorable average cost over time.

Risks, Diversification, and the Future of the Index

While the S&P 500 is often seen as a “safe” investment compared to buying a single penny stock, it is not without risk. Understanding these risks is essential for maintaining a balanced financial strategy.

Concentration Risk and the “Magnificent Seven”

In recent years, the S&P 500 has become increasingly concentrated in a handful of massive technology companies, often referred to as the “Magnificent Seven” (Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta, and Tesla). Because the index is market-cap weighted, these seven companies now represent a significant percentage of the entire index’s value.

The risk here is that if the tech sector faces a specific downturn—due to regulation or a shift in AI sentiment—the entire S&P 500 will suffer, even if the other 493 companies are doing well. Investors who want “true” diversification may sometimes look at “Equal Weight” S&P 500 funds, where every company has a 0.2% stake regardless of size.

Market Volatility

The S&P 500 can and does go down. During the Great Recession of 2008, the index lost over 50% of its value from peak to trough. During the COVID-19 crash of 2020, it dropped over 30% in a matter of weeks. To succeed with an S&P 500 investment strategy, an individual must have the emotional discipline to stay invested during these downturns. Selling during a crash turns “paper losses” into real, permanent losses.

The Role of Rebalancing

The S&P 500 is a “self-cleansing” mechanism. When a company fails or shrinks, it is eventually removed from the index. When a new, innovative company rises, it is added. This ensures that the index always represents the “winners” of the current economy. This internal rebalancing is one of the primary reasons the S&P 500 has been able to survive and thrive through world wars, depressions, and technological revolutions.

In conclusion, the S&P 500 is the ultimate tool for participation in the growth of the modern economy. For anyone looking to master their money, it offers a path to diversification, historical growth, and simplicity. By understanding its mechanics and utilizing low-cost investment vehicles, you can move from being a passive observer of the economy to a partial owner of the world’s most successful enterprises.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.