In the complex ecosystem of modern finance, the ability to categorize, analyze, and compare businesses is fundamental to making sound investment decisions and managing risk. Whether you are a corporate lender, a venture capitalist, or an equity researcher, you require a standardized language to group companies by their primary activities. This is where the Standard Industrial Classification (SIC) system comes into play.

Established in the 1930s, the SIC system remains a cornerstone of business finance, providing a structured framework for identifying the industrial activities of businesses. While newer systems have emerged, the SIC classification remains deeply embedded in financial reporting, government regulation, and market research. Understanding what SIC classification is and how it functions is essential for anyone navigating the realms of business finance and industrial analysis.

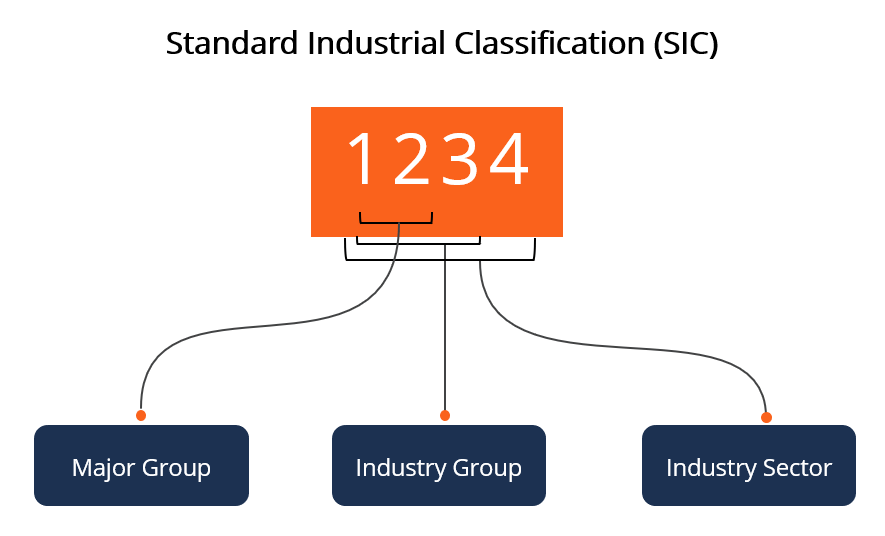

The Architecture of SIC: Understanding the Four-Digit Hierarchy

To utilize SIC codes effectively in a financial context, one must first understand the logic behind their structure. The system is designed as a numerical hierarchy that moves from broad economic sectors to highly specific industrial activities. Every SIC code consists of four digits, with each digit or pair of digits adding a layer of granularity.

How the Four-Digit System Works

The first two digits of an SIC code represent the “Major Group.” This level of classification identifies the broad sector of the economy, such as Agriculture, Forestry, and Fishing (01-09), Manufacturing (20-39), or Finance, Insurance, and Real Estate (60-67).

The third digit defines the “Industry Group.” This narrows the scope further. For example, within the Major Group for “Food and Kindred Products” (20), the third digit might specify “Dairy Products” (202). Finally, the fourth digit identifies the specific “Industry.” Using the same example, 2021 would represent “Creamery Butter,” while 2022 would represent “Natural, Processed, and Imitation Cheese.”

The Hierarchy from Industry Groups to Specific Segments

This hierarchical approach allows financial analysts to “roll up” or “drill down” into data. If an analyst wants to understand the performance of the entire manufacturing sector, they can aggregate data from all codes starting with 20 through 39. Conversely, if they are evaluating a niche startup producing specialized medical equipment, they would look specifically at code 3841 (Surgical and Medical Instruments and Apparatus). This precision is vital for ensuring that financial benchmarks are applied to truly comparable entities.

SIC in Business Finance and Risk Management

For financial institutions and corporate lenders, SIC classification is more than just a labeling system; it is a critical tool for risk assessment and capital allocation. When a business applies for a commercial loan, the SIC code assigned to that business dictates how the bank perceives its risk profile.

Risk Assessment and Credit Scoring

Banks and credit agencies maintain historical data on the failure rates and profitability of various industries. By looking at an applicant’s SIC code, a lender can compare the company’s financial ratios—such as debt-to-equity or current ratio—against the industry average. If a business operates in a “high-risk” SIC category, such as 5812 (Eating Places), it may face more stringent borrowing requirements or higher interest rates compared to a business in a more stable sector, such as 4911 (Electric Services).

Peer Group Comparison and Benchmarking

In business finance, performance is relative. A 10% profit margin might be exceptional in one industry but mediocre in another. SIC codes allow financial managers to perform “peer group analysis.” By identifying companies with the same SIC classification, a CFO can benchmark their firm’s performance against direct competitors. This helps in identifying operational inefficiencies and setting realistic financial targets for the fiscal year.

The Investor’s Lens: Leveraging SIC for Portfolio Strategy

Beyond the banking sector, the investment community relies heavily on SIC codes to organize market data and build diversified portfolios. From equity research to macroeconomic trend analysis, SIC classification provides the framework necessary for sector-based investing.

Sector Allocation and Diversification

A fundamental rule of investing is diversification. To avoid over-exposure to a single economic shock, an investor must ensure their capital is spread across different industries. SIC codes facilitate this by allowing investors to track their holdings by industrial classification. By categorizing a portfolio using SIC codes, an investor can see if they are too heavily weighted in, for instance, “Chemicals and Allied Products” (Major Group 28) and rebalance accordingly to include “Communications” (Major Group 48).

Tracking Market Trends through Industrial Data

Government agencies, such as the Securities and Exchange Commission (SEC) in the United States, use SIC codes to organize the filings of public companies. When an investor uses the EDGAR database to research a company’s 10-K or 10-Q filing, the SIC code is a primary search filter. This allows researchers to track broader market trends. If data suggests that companies under SIC 7372 (Prepackaged Software) are seeing a universal spike in R&D spending, it signals a shift in the tech economy that could influence investment strategies across the board.

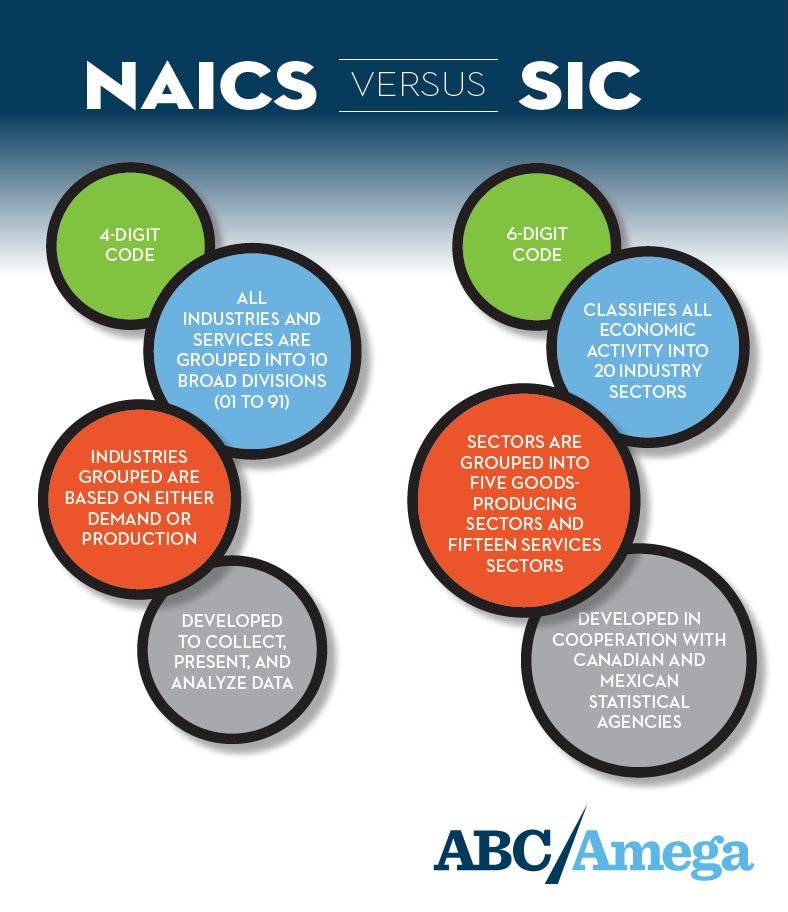

SIC vs. NAICS: Choosing the Right Financial Tool

While the SIC system is venerable, it is not the only classification system in use. In 1997, the North American Industry Classification System (NAICS) was introduced to replace the SIC system in many government functions. However, the transition has not led to the extinction of SIC codes, particularly in the financial sector.

Key Differences for Financial Professionals

The primary difference lies in the philosophy of classification. SIC is largely based on the end product or the market the business serves. NAICS, on the other hand, is based on the production process or the type of work performed. NAICS uses a six-digit code, offering more detail and accounting for modern industries like high-tech manufacturing and digital services that did not exist when the SIC was originally drafted.

For a financial professional, NAICS is often better for analyzing supply chains and production efficiency. However, SIC remains the standard for many legacy financial databases and is still the preferred classification system for the SEC.

Why Older Systems Persist in Financial Reporting

The persistence of SIC in finance is largely due to historical continuity. Decades of financial data are organized by SIC codes. For an analyst performing a longitudinal study on industry profitability over the last 50 years, switching to NAICS mid-stream would create significant data reconciliation issues. Consequently, many credit bureaus, insurance companies, and marketing firms continue to provide data indexed by SIC to ensure compatibility with historical records and existing financial models.

The Future of Industrial Classification in the Era of Big Data

As we move further into the digital age, the way we classify businesses is evolving. Traditional SIC codes are being augmented by “dynamic” classification systems and Artificial Intelligence. However, the logic of the SIC system continues to provide the foundation for these innovations.

The Role of AI in Industrial Categorization

One of the limitations of the traditional SIC system is that many modern companies are “conglomerates” that operate across multiple industries. A single four-digit code may fail to capture the complexity of a company like Amazon or Alphabet.

Today, financial technology (FinTech) firms are using AI and natural language processing (NLP) to scan company websites and financial reports. These tools can assign “weighted” SIC codes to a company, reflecting the percentage of revenue derived from different industrial activities. This provides a more nuanced view of a company’s financial exposure than a static, single-code classification.

Integrating SIC with Modern Financial Tools

Even with the advent of AI, SIC codes remain a vital “anchor” for data. They provide a standardized baseline that ensures different software systems can communicate with one another. In the world of business finance, where data integrity is paramount, the SIC code acts as a universal ID. Whether it is used for tax reporting, identifying eligibility for government grants, or screening stocks, the SIC system remains an indispensable component of the global financial infrastructure.

In conclusion, the SIC classification system is far more than a relic of 20th-century bureaucracy. It is a vital instrument for financial clarity. By providing a structured, hierarchical method for industrial categorization, it enables more accurate risk assessment, more effective peer benchmarking, and smarter investment strategies. For any professional involved in the financial management or analysis of a business, mastering the SIC system is a prerequisite for navigating the complexities of the modern economy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.