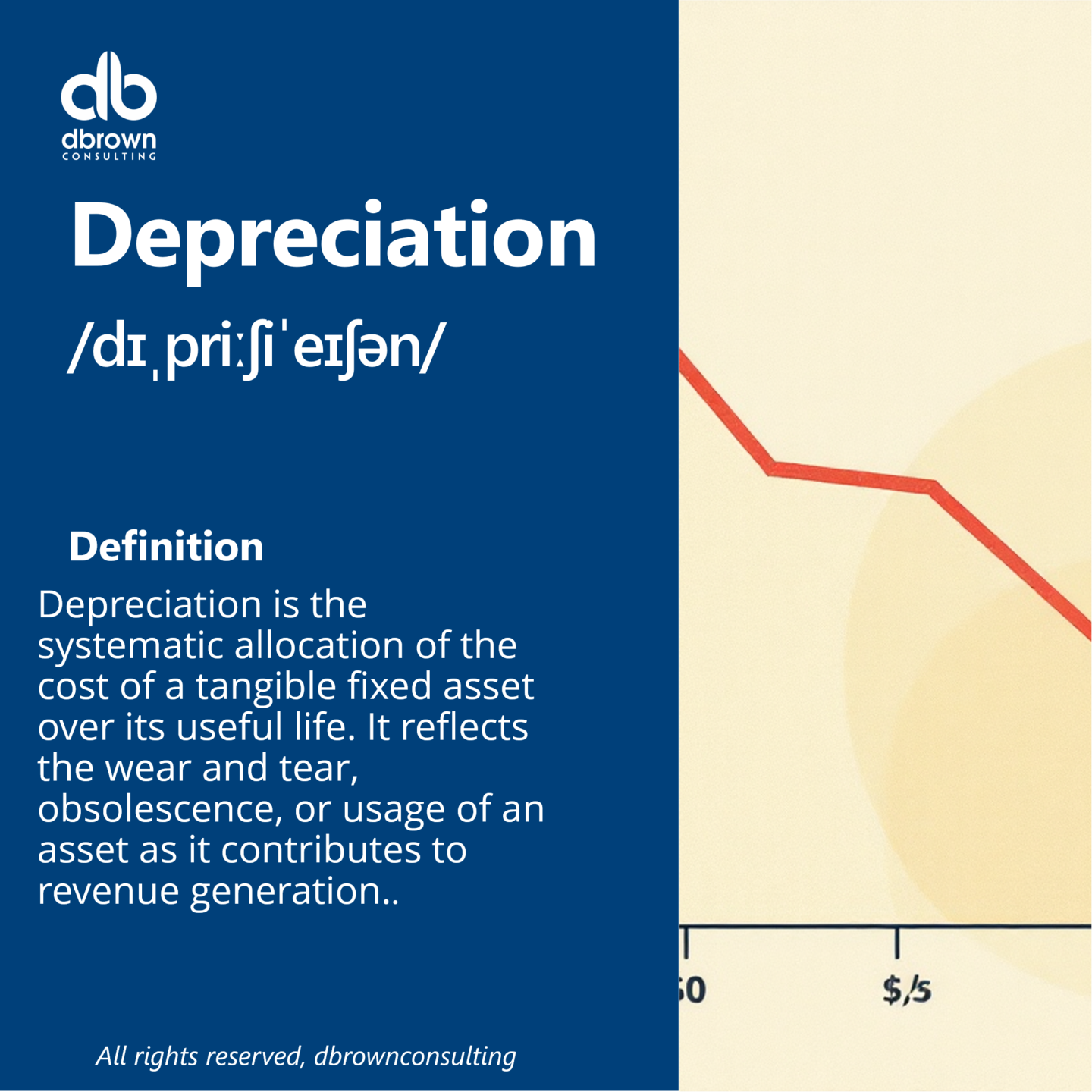

In the world of finance, few concepts are as foundational yet frequently misunderstood as depreciation. Whether you are an entrepreneur managing a growing startup, an investor scrutinizing a balance sheet, or an individual trying to understand the resale value of a vehicle, depreciation is the silent force that reshapes the value of tangible assets over time. At its most basic level, depreciation is an accounting method used to allocate the cost of a tangible asset over its useful life. Rather than deducting the entire cost of an expensive piece of equipment in the year it was purchased, businesses spread that cost out, matching the expense of the asset with the revenue it helps generate.

Understanding what is meant by depreciation requires a dive into both the practical mechanics of accounting and the strategic nuances of financial management. It is not merely a “loss in value”; it is a sophisticated tool for tax planning, profit measurement, and long-term capital budgeting.

The Fundamentals of Depreciation: Why Value Erodes

To grasp the essence of depreciation, one must first look at the nature of physical assets. From heavy machinery and delivery trucks to office furniture and computer hardware, most physical items lose their utility and market value as they age. This erosion of value doesn’t happen at random; it is driven by several predictable factors that financial professionals must quantify.

Why Assets Lose Value Over Time

The primary driver of depreciation is simple physical wear and tear. As a machine operates, its components degrade, leading to a decrease in efficiency and an eventual end to its operational life. However, depreciation also accounts for “obsolescence.” In a rapidly evolving economy, a piece of technology might be in perfect physical condition but lose its value because a newer, more efficient model has rendered it obsolete.

Furthermore, some assets depreciate due to the passage of time or legal limits, such as a leasehold improvement that loses value as the lease term nears its end. By recognizing these factors, depreciation allows a business to reflect the true “consumption” of its capital assets during each accounting period.

The Accounting Logic: The Matching Principle

In the “Money” niche, the most critical reason for depreciation is the “Matching Principle.” This accounting standard dictates that expenses should be matched with the revenues they help produce. If a construction company buys a $100,000 excavator that is expected to last ten years, charging the full $100,000 against the first year’s profits would be misleading. It would make the first year look like a failure and the subsequent nine years look artificially profitable. Depreciation solves this by distributing the $100,000 cost over the decade the excavator is actually working, providing a more accurate picture of the company’s annual profitability.

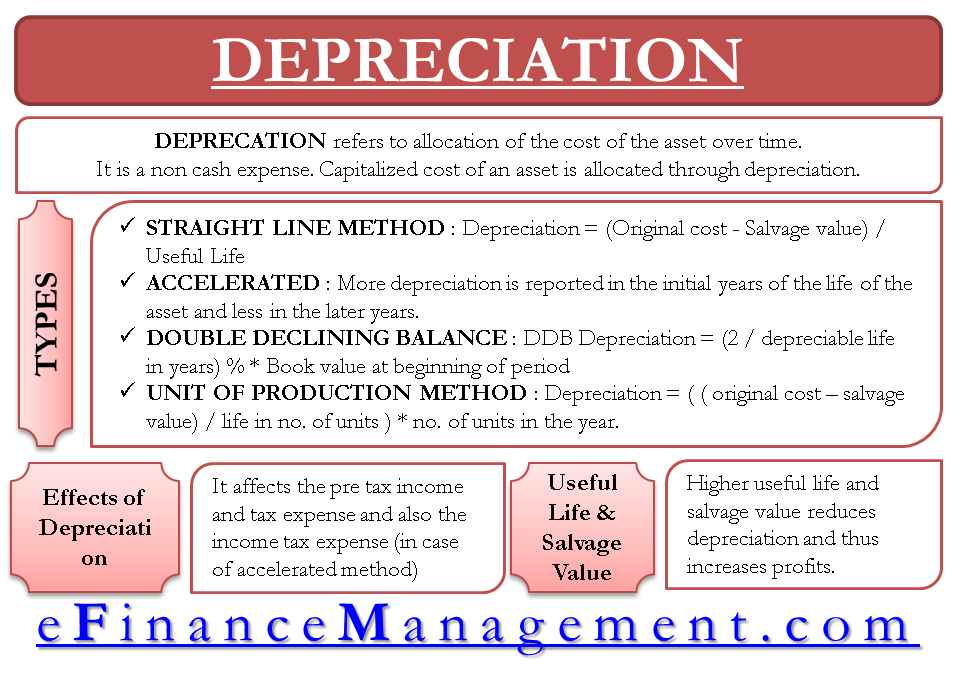

Methods of Calculating Depreciation: Choosing the Right Financial Approach

Not all assets lose value at the same rate. A building might decline in value slowly and steadily, while a high-tech computer system might lose the bulk of its value in the first twenty-four months. To account for these differences, several methods of depreciation are used, each with its own impact on a company’s financial statements.

Straight-Line Depreciation: The Standard for Consistency

The straight-line method is the most common and straightforward approach. To calculate it, you subtract the asset’s “salvage value” (what you expect it to be worth at the end of its life) from its original cost and divide that number by the years of its “useful life.”

For example, if a business buys a server for $11,000 with a salvage value of $1,000 and a five-year lifespan, the annual depreciation expense is $2,000. This method is preferred for its simplicity and for assets that provide a consistent level of utility throughout their existence. It results in a predictable expense on the income statement every year.

Accelerated Depreciation: Managing Tax and High-Utility Assets

In some cases, assets are significantly more productive in their early years. This is where accelerated depreciation methods, such as the Double Declining Balance or Sum-of-the-Years’ Digits, come into play. These methods allow a business to take higher depreciation expenses in the early years and lower expenses later.

From a strategic money management perspective, accelerated depreciation is a powerful tool for tax deferral. By reporting higher expenses early on, a company reduces its taxable income in the short term, preserving cash flow that can be reinvested into the business. This is particularly common with vehicles and specialized tech equipment that devalues rapidly the moment it leaves the showroom or factory.

Units of Production: Usage-Based Valuation

For some industrial assets, time is less important than usage. A printing press or a long-haul truck might have a lifespan defined by how many pages it prints or how many miles it drives rather than how many years have passed. The Units of Production method calculates depreciation based on actual output. If a machine is expected to produce one million units over its life, the depreciation expense for a given year is based on how many units were actually manufactured. This aligns the cost of the asset directly with the volume of business activity.

The Financial Impact: Depreciation on the Balance Sheet and Income Statement

Depreciation is unique because it is a “non-cash” expense. When a company records a depreciation charge, no money actually leaves its bank account. However, the impact on financial reporting and tax liability is profound.

Tax Advantages and Cash Flow Implications

One of the most important aspects of depreciation in business finance is its role as a “tax shield.” Because depreciation is a legitimate business expense, it reduces the net income reported to tax authorities. However, since it is a non-cash charge, the company still holds the cash it would have otherwise paid in taxes.

Smart financial managers use this “depreciation tax shield” to bolster cash flow. By choosing the right depreciation schedule (within the bounds of legal tax codes like MACRS in the United States), a business can effectively receive an interest-free loan from the government by deferring tax payments to later years.

Depreciation vs. Amortization: Clarifying the Confusion

While the terms are often used interchangeably in casual conversation, in professional finance, they refer to different types of assets. Depreciation applies strictly to tangible, physical assets—things you can touch, like buildings and machinery.

Amortization, on the other hand, is the process of spreading out the cost of intangible assets. This includes patents, trademarks, copyrights, and goodwill. While the mathematical logic is similar, the life cycles and legal frameworks surrounding intangible assets differ. Understanding this distinction is vital for accurate financial reporting and for investors who need to know whether a company’s “write-offs” come from physical decay or the expiration of intellectual property.

Strategic Asset Management: Why Depreciation Matters to Investors and Entrepreneurs

For the savvy investor or business owner, depreciation is more than just a line item on a spreadsheet; it is a diagnostic tool for assessing the health and future requirements of a business.

Capital Budgeting and Replacement Cycles

Depreciation provides a roadmap for future capital expenditures (CapEx). By tracking “Accumulated Depreciation” on the balance sheet—which is the total amount of depreciation taken on an asset since it was acquired—a manager can estimate when an asset is nearing the end of its useful life.

If a company has a fleet of trucks that are 90% depreciated, an investor knows that a massive cash outlay for new trucks is likely on the horizon. Ignoring depreciation can lead to a “liquidity crunch” where a business suddenly realizes its equipment is failing but hasn’t set aside the capital to replace it.

Evaluating Company Health Through EBITDA

In the world of investing and business valuation, a common metric used is EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization). By “adding back” depreciation to the net income, analysts can get a clearer view of a company’s operational cash flow.

This is particularly important when comparing companies in capital-intensive industries (like manufacturing or telecommunications) with those in asset-light industries (like software). Depreciation can make a highly successful, cash-rich manufacturing firm look unprofitable on paper due to large non-cash charges. By understanding what is meant by depreciation, an investor can look past the surface-level profit figures to see the true cash-generating power of the enterprise.

Conclusion: The Long-Term Value of Understanding Depreciation

Depreciation is the bridge between the physical reality of decaying assets and the abstract world of financial accounting. It ensures that a business remains honest about its costs, helps manage tax burdens efficiently, and provides a framework for future growth. Whether you are calculating the “book value” of a small business or analyzing a Fortune 500 company’s annual report, a mastery of depreciation allows you to see the real movement of money behind the scenes. In the end, depreciation isn’t just about things losing value; it’s about strategically managing that loss to build a more sustainable and profitable financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.