In the world of personal finance, estate planning, and wealth management, the term “immediate family” is more than just a sentimental descriptor of our closest relatives. It is a critical legal and financial designation that determines who has access to your benefits, who is entitled to your assets upon your death, and how you are taxed by the government. Understanding the specific boundaries of this definition is essential for anyone looking to secure their financial future and protect their loved ones.

While the colloquial definition might vary from person to person, financial institutions, insurance companies, and the Internal Revenue Service (IRS) use strict criteria to define immediate family. This article explores those definitions and the profound impact they have on your money, your legacy, and your long-term financial strategy.

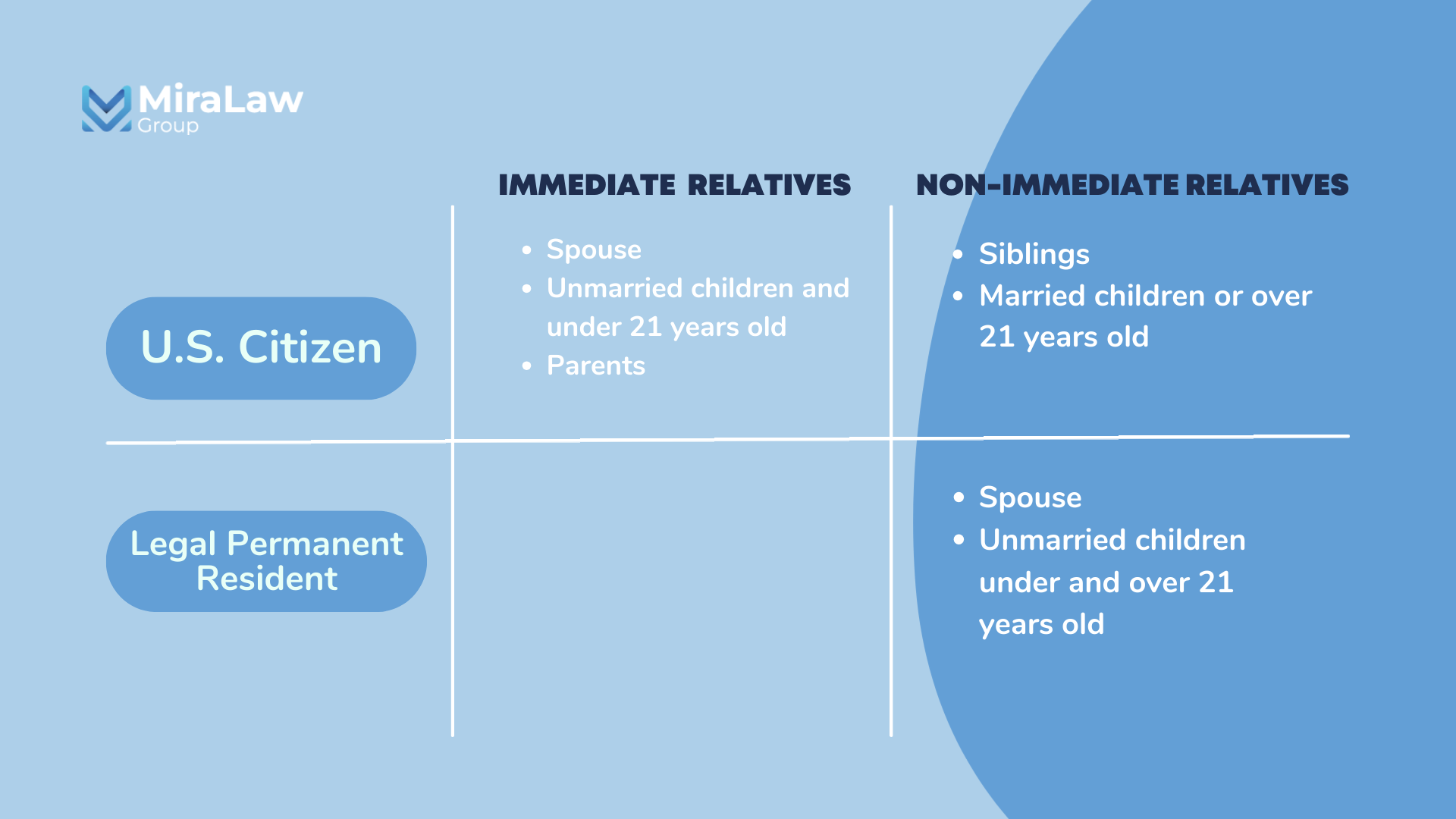

Defining Immediate Family in the Financial Landscape

The definition of “immediate family” is not universal; it shifts depending on the entity requesting the information. For a bank, the definition might be narrow, while a life insurance policy might allow for a broader interpretation. However, at its core, the designation serves to identify the primary circle of individuals who share a direct legal or blood connection to an account holder or taxpayer.

The Core Legal Definition

Generally, the most basic definition of immediate family includes a person’s spouse, parents, and children. In most financial contexts, this also extends to siblings. This “nuclear” definition is the bedrock of most inheritance laws and basic insurance coverage. These relationships are often prioritized because they involve a direct line of descent or a legal union (marriage) that carries inherent financial obligations, such as child support or spousal maintenance.

Broadening the Scope: IRS vs. Private Institutions

The IRS has its own specific sets of rules, which can vary depending on whether you are looking at dependency credits, gift tax exclusions, or retirement account distributions. For instance, for tax purposes, “immediate family” may include step-children, foster children, and in-laws, provided they meet certain residency and financial support requirements.

Conversely, private institutions like banks or investment firms might use a broader definition for “family office” services or multi-generational wealth management. In these cases, grandparents, grandchildren, and even aunts or uncles might be included if the goal is the comprehensive management of a family’s total net worth.

The Role of Dependency and Residency

In many financial scenarios, particularly regarding health insurance and tax deductions, the definition of immediate family is tied to dependency. If you provide more than half of an individual’s financial support, the IRS may treat them as immediate family for tax-saving purposes, even if they are a more distant relative. Residency also plays a role; living under the same roof for more than half the year can often validate a claim of “immediate” status in the eyes of insurance providers.

The Financial Stakes: Inheritance and Estate Planning

One of the most significant reasons to understand the definition of immediate family is for estate planning. If you pass away without a clear will or trust (a state known as “intestacy”), your assets are distributed based on state laws that prioritize your immediate family.

Intestate Succession and the “Immediate Family” Priority

When a person dies intestate, the court follows a hierarchy to distribute assets. The spouse is almost always first in line, followed by children, parents, and then siblings. If you have a non-traditional family structure—such as a long-term partner to whom you are not legally married—they may be completely excluded from this definition. Understanding this hierarchy allows you to realize where your financial gaps lie and prompts the necessity of a formal will to bypass standard legal definitions.

Life Insurance Beneficiary Designations

Life insurance is a cornerstone of financial security for many families. While you can technically name anyone as a beneficiary, most policies are designed to provide for immediate family members who would suffer a financial loss upon your death. When a policy refers to “family riders” or “dependents,” it is using the strict definition of immediate family. Ensuring your beneficiaries are correctly categorized ensures that claims are processed quickly and without the legal hurdles that can arise when “distant” relatives or non-relatives are named.

Trusts: Protecting the Next Generation

A trust is a powerful financial tool that allows you to define “family” on your own terms. However, many standard trust templates use the “immediate family” language to simplify the distribution of interest and principal. By working with a financial advisor, you can use a trust to either narrow the scope (ensuring assets stay only with blood descendants) or broaden it to include individuals who may not meet the legal definition of immediate family but play a significant role in your life.

Maximizing Tax Benefits Through Family Status

The government provides numerous tax incentives designed to support the stability of the family unit. Knowing who qualifies as immediate family can lead to significant annual savings.

Filing Status: Head of Household vs. Joint Filing

Your filing status is the single most impactful decision you make on your tax return. To file as “Head of Household,” you must have a qualifying person—usually an immediate family member—living with you for whom you provide the majority of support. This status offers a higher standard deduction and more favorable tax brackets than filing as “Single,” directly impacting your take-home pay and investment capital.

The Gift Tax Exclusion and Family Wealth Transfers

For those focused on generational wealth, the annual gift tax exclusion is a vital tool. As of 2024, an individual can give $18,000 per year to any number of individuals without triggering a gift tax return. While you can give this to anyone, most people utilize this to transfer wealth to immediate family members. By “splitting” gifts with a spouse, a couple can give $36,000 per year to a child or grandchild, effectively moving assets out of a taxable estate while providing immediate financial support to the next generation.

Education Savings: 529 Plans and the Family Tree

529 college savings plans are highly flexible regarding the definition of family. You can change the beneficiary of a 529 plan at any time, provided the new beneficiary is a “member of the family” of the original beneficiary. This includes children, siblings, parents, cousins, and even in-laws. This broad definition allows for the efficient movement of capital within the extended family to ensure that education is funded with tax-advantaged dollars.

Workplace Benefits and the Immediate Family Clause

Your employment contract and benefits package are often built around the “immediate family” concept. Misunderstanding these definitions can result in missed opportunities for coverage or even disciplinary action for misuse of leave.

Health Insurance Eligibility and Dependent Coverage

Employer-sponsored health insurance is typically restricted to the employee and their immediate family (spouse and children). With the passage of the Affordable Care Act, “children” now includes adult children up to age 26. However, siblings or parents are rarely eligible for coverage under a standard employer plan. Understanding this boundary is essential when calculating the total value of a job offer or planning for the healthcare needs of aging parents.

Paid Family Leave and Bereavement Policies

The Family and Medical Leave Act (FMLA) allows eligible employees to take unpaid, job-protected leave to care for immediate family members with serious health conditions. However, the federal definition of immediate family for FMLA is relatively narrow: spouse, parents, and children. Siblings and grandparents are often excluded unless they acted in loco parentis (as a parent) when the employee was a child. Reviewing your company’s specific handbook is vital, as many modern brands are expanding these definitions to remain competitive in the talent market.

Retirement Accounts: Spousal Rights and Inherited IRAs

Retirement assets like 401(k)s and IRAs have unique rules regarding immediate family. For a 401(k), federal law dictates that a spouse is the automatic beneficiary unless they sign a written waiver. For IRAs, an immediate family member who inherits the account (especially a spouse) has much more flexibility in how they “roll over” the assets compared to a non-spouse beneficiary. These rules are designed to prevent the immediate taxation of retirement wealth, allowing it to continue growing for the survivor’s benefit.

Strategies for Managing Family Wealth Distribution

To truly master your personal finances, you must take a proactive approach to how your “immediate family” is documented across your financial life.

Defining Your “Financial Family” Early

Do not wait for a crisis to determine who counts as immediate family in your financial ecosystem. Map out your primary beneficiaries across all accounts: bank accounts (Transfer on Death), brokerage accounts, and retirement plans. Ensure that your legal documents (wills and power of attorney) match the definitions used by your financial institutions.

The Risks of Ambiguous Language in Financial Documents

Vague terms like “my heirs” or “my relatives” can lead to years of expensive litigation. In the eyes of the law, these terms are open to interpretation. Instead, use specific names and define the relationship clearly. If you intend to include step-children or domestic partners who are not legally recognized as “immediate family” in your jurisdiction, you must explicitly state this in your legal and financial documents to ensure they are treated as such.

Utilizing Financial Professionals to Bridge the Gap

Estate attorneys and certified financial planners (CFPs) are experts at navigating the nuances of family definitions. They can help you structure “Family Limited Partnerships” or “Crummey Trusts” that allow for the controlled distribution of wealth to a broader circle while maintaining the tax benefits associated with immediate family transfers. By seeking professional advice, you ensure that your definitions are compliant with current tax codes and robust enough to withstand legal challenges.

In conclusion, “immediate family” is a foundational concept that dictates the flow of capital, the burden of taxes, and the security of your legacy. By understanding how this term is applied in the realms of law and finance, you can better position yourself to maximize your benefits, minimize your liabilities, and ensure that your wealth serves the people who matter most to you.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.