Economic policy serves as the primary steering mechanism for a nation’s financial health. It encompasses the diverse range of actions, regulations, and systems implemented by governments and central banks to influence economic activity. From the interest rates on your savings account to the taxes deducted from your paycheck, economic policy dictates the rhythm of the marketplace and the standard of living for citizens.

In the world of finance and business, understanding economic policy is not merely an academic exercise; it is a prerequisite for successful investing, strategic corporate planning, and personal wealth management. By analyzing how leaders manipulate the levers of the economy, individuals and organizations can better navigate the complexities of inflation, recession, and growth.

Understanding the Core Pillars of Economic Policy

To grasp the magnitude of economic policy, one must first distinguish between its two primary engines: fiscal policy and monetary policy. While they both aim to achieve macroeconomic stability, they utilize different tools and are governed by different institutions.

Fiscal Policy: Taxation and Spending

Fiscal policy is the domain of the government—specifically the executive and legislative branches. It involves the use of government spending and tax revenue to influence the economy. When a government increases spending on infrastructure, such as bridges or digital networks, it injects capital directly into the economy, creating jobs and stimulating demand. Conversely, by adjusting tax rates, the government can either increase the disposable income of its citizens (through tax cuts) or cool down an overheated economy (through tax hikes).

The balance between spending and revenue determines the fiscal stance. A “budget deficit” occurs when spending exceeds revenue, often used during recessions to jumpstart growth. A “budget surplus” happens when revenue exceeds spending, which can be used to pay down national debt or prevent the economy from expanding too rapidly and causing inflation.

Monetary Policy: Interest Rates and Money Supply

Monetary policy is typically managed by a nation’s central bank, such as the Federal Reserve in the United States or the European Central Bank in the EU. Unlike fiscal policy, which deals with physical cash flow and projects, monetary policy focuses on the cost and availability of money.

The primary tool of monetary policy is the manipulation of interest rates. When interest rates are low, borrowing becomes cheaper for businesses and consumers, encouraging investment and spending. When inflation rises, central banks often increase interest rates to “tighten” the money supply, making borrowing more expensive and slowing down price increases. Additionally, central banks use open market operations—buying or selling government bonds—to directly influence the amount of money circulating within the banking system.

The Synergy Between Fiscal and Monetary Action

While these two pillars operate independently, they are most effective when they work in tandem. For example, during a severe economic downturn, a government might implement expansionary fiscal policy (increased spending), while the central bank simultaneously lowers interest rates. This dual approach provides a powerful stimulus, ensuring that there is both public investment and affordable private credit available to facilitate recovery.

The Primary Objectives of Economic Policy

Every economic policy decision is driven by specific goals. While different administrations may prioritize different outcomes based on their political or economic philosophy, three core objectives remain universal in modern finance.

Promoting Sustainable GDP Growth

Gross Domestic Product (GDP) is the total value of all goods and services produced within a country. A primary goal of economic policy is to ensure steady, sustainable growth in GDP. Growth signifies that a country is becoming more productive, businesses are expanding, and the overall wealth of the nation is increasing.

However, policy makers must balance “fast” growth with “sustainable” growth. If an economy grows too quickly, it can lead to asset bubbles or resource depletion. Economic policy aims for a “Goldilocks” scenario—growth that is neither too hot (causing inflation) nor too cold (leading to stagnation).

Maintaining Price Stability and Controlling Inflation

Inflation is the rate at which the general level of prices for goods and services rises, subsequently eroding purchasing power. High inflation can be devastating for personal finance, as it devalues savings and makes long-term planning difficult for businesses.

Economic policy, particularly monetary policy, targets a specific inflation rate—often around 2%. This level is considered healthy because it encourages consumers to spend rather than hoard cash, without causing the cost of living to spiral out of control. When inflation moves significantly away from this target, policy shifts occur to bring the economy back into alignment.

Achieving Full Employment

A functioning economy requires a robust labor market. High unemployment leads to decreased consumer spending, social instability, and a loss of human capital. Economic policy aims to create an environment where everyone who is willing and able to work can find employment.

This is often achieved through supply-side policies (improving labor market flexibility and education) or demand-side policies (stimulating the economy to ensure businesses need to hire more workers). It is important to note that “full employment” does not mean 0% unemployment; there will always be people transitioning between jobs. Rather, it refers to the lowest level of unemployment an economy can sustain without triggering excessive inflation.

Mechanisms of Implementation and Policy Tools

How are these high-level goals translated into real-world action? The implementation of economic policy requires a sophisticated toolkit that allows for both broad strokes and surgical precision.

Quantitative Easing and Contractionary Measures

In times of extreme crisis, traditional interest rate adjustments may not be enough. This is where “Quantitative Easing” (QE) comes into play. In QE, a central bank purchases long-term securities from the open market to increase the money supply and encourage lending and investment. It is a form of “monetary bazooka” used when rates are already near zero.

On the opposite end of the spectrum are contractionary measures. If the economy is “overheating”—evidenced by skyrocketing property prices or excessive speculation—the central bank will sell bonds and raise the reserve requirements for banks. This reduces the amount of capital available for lending, effectively putting the brakes on the economy to prevent a future crash.

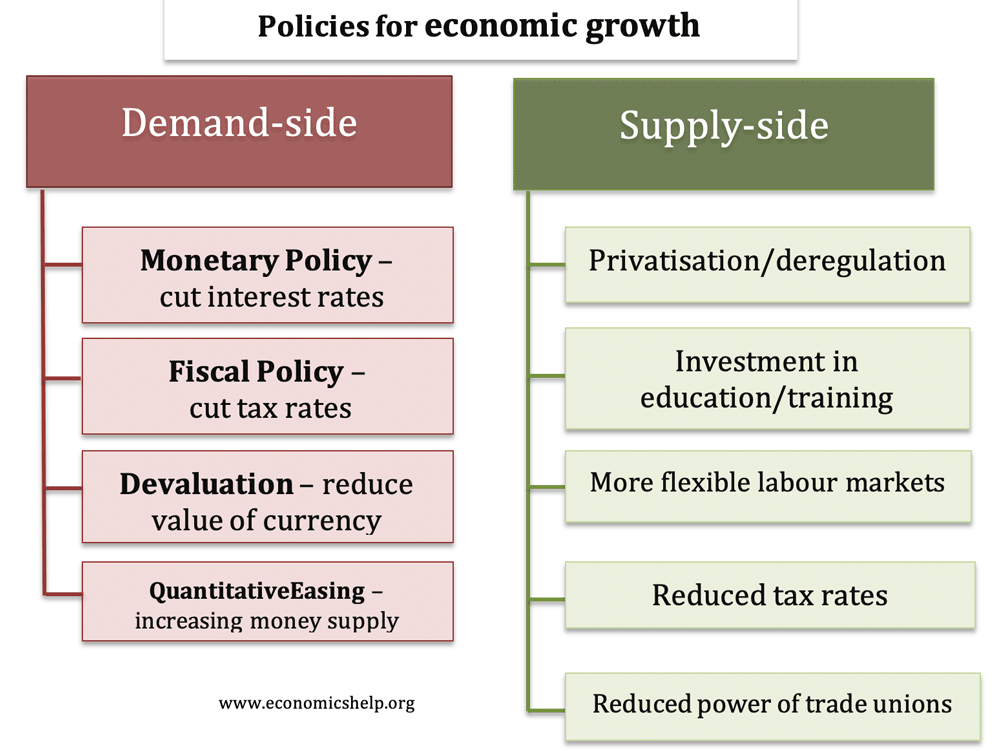

Supply-Side vs. Demand-Side Approaches

Economic policy often fluctuates between two competing philosophies: supply-side and demand-side economics.

Demand-side (Keynesian) economics focuses on the consumer. The idea is that by putting money in the hands of the people—through social programs, infrastructure jobs, or middle-class tax cuts—the increased demand will force businesses to expand and hire.

Supply-side economics focuses on the producers. This theory suggests that by lowering corporate taxes and reducing regulations, businesses will have more capital to invest in innovation and expansion. The resulting “trickle-down” effect is intended to create jobs and lower prices for everyone. Most modern economies use a hybrid of these two approaches depending on the current economic climate.

Automatic Stabilizers in the Economy

Not all economic policy requires a new act of government. “Automatic stabilizers” are built-in mechanisms that react to the economic cycle without immediate political intervention. Examples include unemployment insurance and progressive income taxes. When the economy slows down, more people qualify for unemployment benefits, which injects money into the economy. Simultaneously, because incomes fall, people move into lower tax brackets, effectively receiving an automatic “tax cut.” These mechanisms help dampen the volatility of the business cycle.

The Impact of Economic Policy on Personal Finance and Investing

For the individual investor or business owner, economic policy is not just a headline; it is a direct influence on their financial portfolio. Every policy shift creates winners and losers in the market.

How Interest Rates Affect Mortgages and Savings

The most direct impact of monetary policy on the average person is through interest rates. When the central bank raises the federal funds rate, commercial banks follow suit. For savers, this is good news: high-yield savings accounts and Certificates of Deposit (CDs) begin to offer better returns.

However, for borrowers, the news is less positive. The cost of a 30-year fixed mortgage, auto loans, and credit card interest rates all climb. This reduces the “disposable income” of households with debt, which in turn can lead to a decrease in consumer spending across the broader economy.

Economic Cycles and Stock Market Performance

Investors watch economic policy closely because it dictates the “discount rate” used to value future corporate earnings. When policy is expansionary (low rates, high spending), stocks generally perform well because the “cost of capital” is low and consumer demand is high.

Conversely, when the government signals a shift toward “austerity” (cutting spending) or the central bank enters a “hawkish” phase (raising rates), the stock market often experiences volatility. Sector-specific policies also matter; for instance, a fiscal policy that prioritizes green energy will drive capital into the renewables sector while potentially penalizing traditional fossil fuel industries.

Challenges and Criticisms of Modern Economic Policy

Despite the sophisticated models used by economists, implementing economic policy is an imperfect science. There are several inherent challenges that can cause even the best-laid plans to go awry.

The Problem of Time Lags

One of the greatest difficulties in economic policy is the “lag” effect. There is a recognition lag (the time it takes to realize there is a problem), a decision lag (the time it takes for politicians to agree on a solution), and an implementation lag (the time it takes for the policy to actually affect the economy). By the time a stimulus package is fully operational, the recession may have already ended, potentially leading to unnecessary inflation.

The Growing Concern of National Debt

Heavy reliance on expansionary fiscal policy often leads to a significant increase in national debt. While borrowing is necessary during crises, a high debt-to-GDP ratio can eventually become a drag on the economy. Future generations may face higher taxes or reduced public services to pay for the interest on this debt. Critics of modern economic policy argue that we are often “borrowing from the future” to pay for the comforts of the present.

The Risk of Policy Miscalculation

Economic systems are incredibly complex and involve billions of individual decisions. A central bank might raise rates too quickly, inadvertently triggering a deeper recession than intended. Similarly, a government might spend too much during a period of supply constraints, leading to “stagflation”—a painful combination of stagnant growth and high inflation. The margin for error is slim, and the consequences of miscalculation can be felt for decades.

In conclusion, economic policy is the invisible hand that guides the modern financial world. By understanding the interplay between fiscal spending, monetary regulation, and the overarching goals of growth and stability, individuals can make more informed decisions about their money. Whether you are managing a corporate budget or a personal retirement account, staying attuned to the shifts in economic policy is essential for long-term financial success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.