The abbreviation CVC, often seen on the back of credit and debit cards, stands for Card Verification Value. It’s a crucial security feature designed to protect both consumers and merchants from fraudulent transactions. While commonly referred to as CVC, you might also encounter other terms for this three or four-digit code, such as CVV (Card Verification Value) used by Visa, CVC2 (Card Verification Code 2) by Mastercard, CID (Card Identification Number) by American Express, and CSC (Card Security Code). Regardless of the specific nomenclature, their purpose remains the same: to verify that the physical card is in the possession of the person attempting to make a purchase, especially in “card-not-present” transactions like online or phone orders.

Understanding the CVC is paramount in navigating the digital economy safely. As e-commerce continues its explosive growth, the ability to conduct transactions securely online has become an everyday necessity. This necessitates a clear understanding of the security protocols that underpin these digital exchanges, and the CVC is a cornerstone of that system. By demystifying its function and importance, consumers can empower themselves to shop online with greater confidence and mitigate the risks associated with digital payments.

The Genesis and Evolution of Card Security Codes

The introduction of security codes like CVC was a natural progression in the ongoing battle against payment card fraud. As transactions moved beyond the physical point-of-sale terminal, new vulnerabilities emerged. The magnetic stripe on the back of cards contained static information that could be relatively easily duplicated. This led to the development of more dynamic and sophisticated security measures.

Early Security Measures and Their Limitations

In the early days of credit card usage, transactions relied heavily on the physical presentation of the card. Merchants would manually imprint the card details onto a sales slip, and often require a signature. While this provided a degree of verification, it was susceptible to issues such as forged signatures and the theft of card details when cards were lost or stolen. The advent of the magnetic stripe revolutionized the speed and efficiency of transactions, but it also introduced the risk of data skimming, where the information on the stripe could be copied.

The Birth of the CVC: A Response to Growing Fraud

As the volume of “card-not-present” transactions, particularly those conducted over the phone and later online, began to surge, so too did the incidence of fraud. Criminals found it easier to exploit stolen card numbers obtained through various means. In response, card networks like Visa and Mastercard, along with American Express, began developing additional security layers. The CVC was conceived as a way to add a unique, non-static piece of information that was not stored in the magnetic stripe or embossed on the card’s face, thus making it harder for fraudsters to use stolen card details without possessing the physical card.

Differentiating CVC, CVV, CVC2, and CID

While the underlying principle is the same, the different card networks have adopted their own terminology:

- CVV (Card Verification Value): This is Visa’s term for the security code. It is typically a three-digit number found on the back of Visa cards.

- CVC (Card Verification Code): This is Mastercard’s term. It is also a three-digit number located on the back of Mastercard.

- CVC2 (Card Verification Code 2): This is a more specific designation, often used in technical documentation, to distinguish it from earlier versions of the code. For everyday users, it functions identically to CVC.

- CID (Card Identification Number): American Express uses a four-digit code, which they call CID. This is usually found on the front of American Express cards, above the embossed account number.

The presence of a unique code for each card, generated independently by the issuer and not stored by the merchant, significantly raises the bar for fraudulent activities. It ensures that even if a criminal has managed to obtain the card number and expiry date, they would still need access to the physical card to complete a transaction.

Locating and Understanding Your CVC

The CVC is designed to be a readily accessible yet distinct piece of information on your card, serving as a tangible link between you and your financial instrument. Knowing where to find it and what it represents is the first step in leveraging its security benefits.

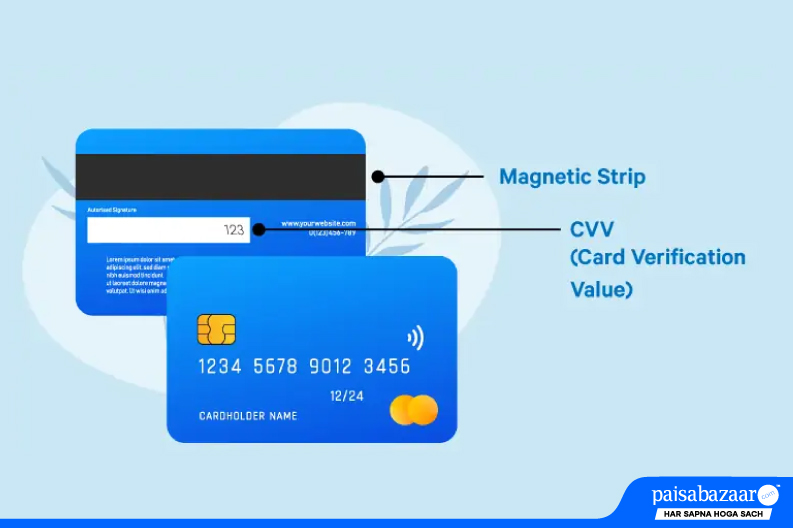

The Physical Location of the CVC

For the vast majority of credit and debit cards, including Visa and Mastercard, the CVC is a three-digit number printed on the back of the card, typically in or near the signature strip. You’ll usually find it after the full card number (or a portion of it) has been repeated.

American Express cards are the primary exception. Their Card Identification Number (CID) is a four-digit code and is typically located on the front of the card, above the embossed account number, often on the right-hand side.

It’s important to note that the CVC is not embossed like the card number, expiry date, or cardholder’s name. This is a deliberate security measure. If it were embossed, it would be more susceptible to being captured by skimming devices that focus on raised lettering. The printed nature of the CVC means that it’s not automatically captured by most standard point-of-sale terminals that read the magnetic stripe or chip.

Why the CVC is Not Stored by Merchants

A fundamental tenet of CVC security is that merchants are prohibited from storing this information after a transaction has been authorized. This is a critical security protocol mandated by card brands. When you make an online or phone purchase, you are asked to provide your CVC. The merchant’s payment gateway transmits this code to the acquiring bank and then to the card network for verification. Once the transaction is approved or declined, the CVC should be discarded by the merchant.

This policy is essential because if merchants were allowed to store CVCs, a data breach at a merchant’s system could expose not only card numbers and expiry dates but also these crucial verification codes. This would render the CVC largely ineffective as a fraud prevention tool, as criminals would have all the necessary information to make fraudulent transactions. This prohibition forces fraudsters to physically possess the card or obtain the CVC through other, more direct means, such as phishing scams or physical theft.

The CVC and Recurring Payments

The rule about not storing CVCs presents a challenge for recurring payments, such as subscriptions or regular billing. In these cases, merchants often use a tokenization system. Instead of storing the actual CVC, they store a unique, randomly generated token that represents your card details. This token can be used for future transactions without the CVC needing to be re-entered each time. The initial transaction would have involved you providing your CVC, and the system would then generate and store this token. If you update your card details, you will typically need to re-enter the CVC for the new card, which will then generate a new token. This ensures that even if the token is compromised, it’s not directly linked to your actual card security code.

The Role of CVC in Online Security

The CVC plays a pivotal role in safeguarding online transactions, acting as a digital handshake that verifies the legitimacy of a purchase. Its effectiveness hinges on its unique properties and the rigorous security protocols surrounding its use.

Verifying “Card-Not-Present” Transactions

The primary function of the CVC is to authenticate transactions where the physical card is not present. This includes:

- Online Shopping: When you enter your card details into a website’s checkout form.

- Phone Orders: When you provide your card information to a sales representative over the phone.

- Mail Orders: Similar to phone orders, where card details are submitted via mail.

- App Purchases: Transactions made within mobile applications.

In these scenarios, the card number and expiry date can be obtained through various means, such as data breaches, phishing emails, or malware. However, the CVC is generally not stored in the magnetic stripe or chip and is not typically captured by simple skimming devices. Therefore, requiring the CVC adds an extra layer of security, significantly reducing the likelihood of fraudulent transactions using stolen card numbers alone. The assumption is that if a fraudster has obtained your card number and expiry date, but not the CVC, they likely do not have physical possession of your card.

How the CVC Verification Process Works

When you enter your CVC during an online or phone transaction, the following process generally occurs:

- Submission: The CVC is transmitted securely, usually encrypted, along with your card number and expiry date, to the merchant’s payment gateway.

- Authorization Request: The payment gateway forwards the transaction details, including the CVC, to the acquiring bank.

- Card Network Verification: The acquiring bank sends the request to the relevant card network (Visa, Mastercard, American Express, etc.).

- Issuer Check: The card network routes the request to your card-issuing bank. The issuing bank compares the CVC provided with the CVC on file for that specific card.

- Response: The issuing bank sends back an approval or denial code. If the CVC matches, it contributes to a higher confidence score for the transaction. If it does not match, it is often a strong indicator of fraud, and the transaction may be declined.

- Merchant Notification: The card network relays the approval or denial back to the acquiring bank, which then informs the payment gateway, and finally, the merchant.

The issuing bank is the only entity that truly knows the correct CVC for your card. The card networks and their processing systems facilitate the comparison, but they do not store the CVC in a retrievable format for merchants. This distributed security model is designed to minimize the impact of any single point of failure.

CVC and 3D Secure Protocols (e.g., Verified by Visa, Mastercard Identity Check)

While the CVC is a strong standalone security feature, it is often used in conjunction with more advanced authentication protocols. 3D Secure is a protocol developed by Visa and adopted by other card networks that adds an extra layer of security to online credit and debit card transactions. Examples include:

- Verified by Visa

- Mastercard Identity Check (formerly SecureCode)

- American Express SafeKey

- Discover ProtectBuy

These protocols often prompt the cardholder to authenticate themselves directly with their card issuer, usually by entering a password, a one-time code sent via SMS, or by using a biometric authentication method. When you encounter a website that uses 3D Secure, you might be redirected to a page hosted by your bank, where you’ll be asked to verify your identity.

The CVC plays a role in the initial stages of these 3D Secure transactions by helping to validate that the person initiating the transaction is in possession of the card. If the CVC is incorrect, the 3D Secure process might not even begin, or it will likely result in a decline. However, the ultimate authentication happens directly between the cardholder and the issuing bank through the 3D Secure interface. Therefore, while the CVC is a vital component, it’s part of a broader ecosystem of security measures designed to protect your financial data.

Protecting Your CVC and Preventing Fraud

The CVC is a powerful tool against fraud, but its effectiveness relies on your vigilance in protecting this sensitive information. Treating your CVC with the same care as your card number and PIN is essential for secure financial practices.

Best Practices for Handling Your CVC

- Never Share Your CVC: Treat your CVC as you would your PIN. Do not share it with anyone, including friends, family, or customer service representatives, unless you are explicitly making a purchase and are on a secure, trusted platform.

- Be Wary of Unsolicited Requests: If you receive an email, text message, or phone call asking for your CVC, especially if you did not initiate the contact, it is highly likely to be a phishing attempt. Legitimate businesses will not ask for your CVC in such a manner.

- Check Your Card Before Entering CVC: When shopping online or over the phone, make sure you are physically looking at your card to retrieve the correct CVC.

- Inspect Your Card: Regularly check your physical credit and debit cards for any signs of tampering or damage that might compromise the security features.

- Use Secure Websites: When shopping online, ensure the website uses encryption (look for “https://” in the URL and a padlock icon in your browser’s address bar). This helps protect the information you submit, including your CVC.

- Avoid Saving CVCs Unless Necessary: While some online retailers offer the option to save card details for faster checkout, be cautious. If you do, understand their security measures. For recurring payments, tokenization is a more secure alternative than storing the CVC directly.

What to Do if Your CVC is Compromised

If you suspect your CVC or any other card information has been compromised, immediate action is crucial:

- Contact Your Bank Immediately: This is the most important step. Report the suspected fraud to your card-issuing bank or credit card company. They can help you cancel the compromised card and issue a new one.

- Monitor Your Account Statements: Even after reporting the compromise, meticulously review your bank and credit card statements for any unauthorized transactions.

- Change Passwords and Security Questions: If you believe your email or other online accounts may have been compromised in conjunction with your card details, change your passwords and update security questions for those accounts.

- Report Phishing Attempts: If you believe you fell victim to a phishing scam, report it to your email provider and relevant consumer protection agencies.

The CVC and Data Breaches: A Complex Relationship

While the CVC is designed to prevent fraud even when card numbers are stolen, data breaches can still complicate matters. If a breach exposes card numbers, expiry dates, and CVCs simultaneously (which should not happen if merchants adhere to security protocols), it creates a high-risk scenario. However, the prohibition on merchants storing CVCs is a strong safeguard. Most breaches that expose card numbers do not include the CVC because merchants are forbidden from keeping it. The CVC’s true strength lies in its non-storage by merchants and its requirement for “card-not-present” transactions, making it a persistent obstacle for fraudsters.

In conclusion, the CVC is a vital security feature that adds a significant layer of protection to your financial transactions, particularly in the digital realm. By understanding its purpose, how to locate it, and how to protect it, you can navigate the world of online commerce with greater confidence and security. Always remember that your vigilance is your strongest defense against financial fraud.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.