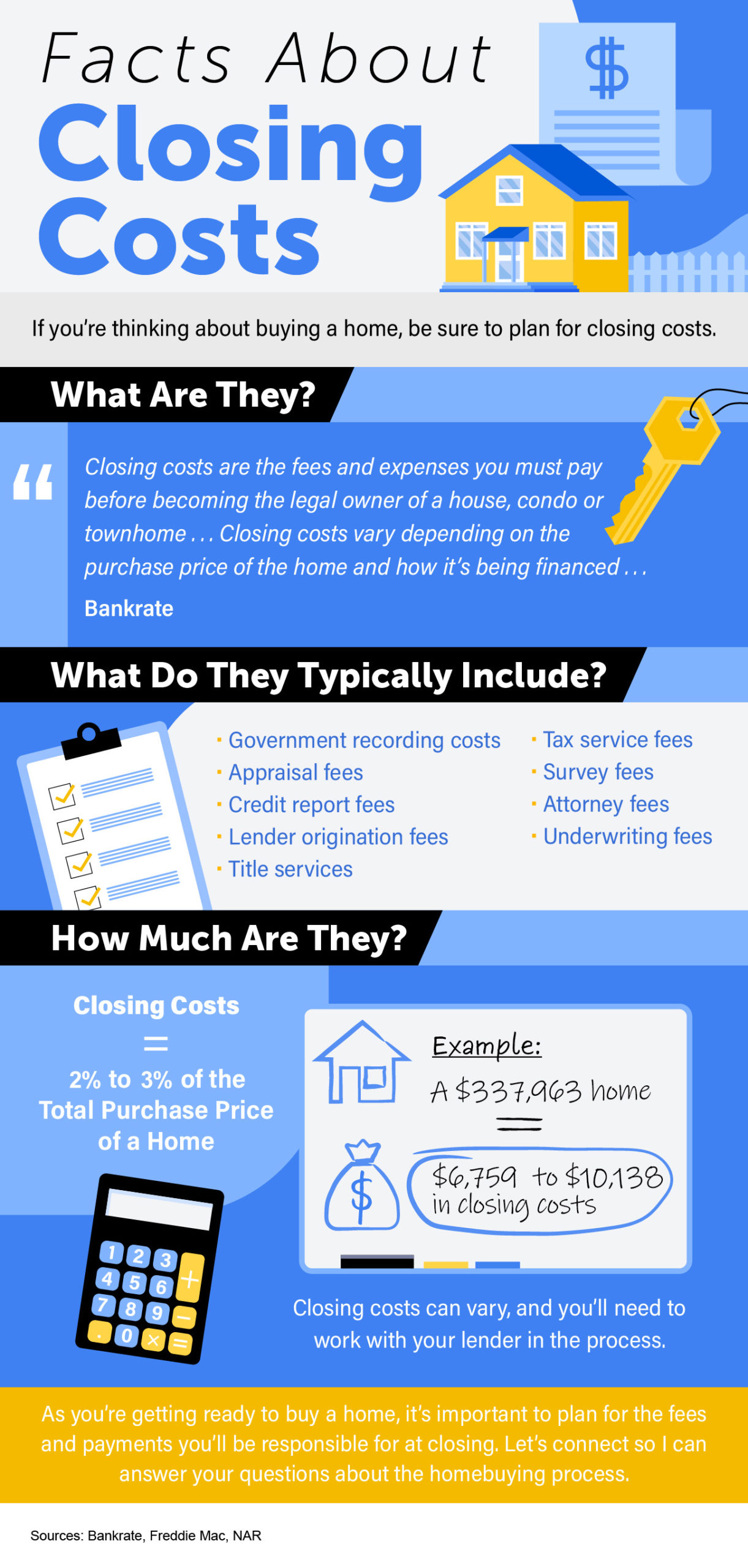

When you embark on the journey of buying or selling a home, the term “closing costs” will inevitably surface. It’s a crucial concept, representing a significant financial component that often catches first-time buyers and even seasoned sellers by surprise. These aren’t just arbitrary fees; they are a collection of expenses incurred by both parties during the finalization of a real estate transaction. Understanding what closing costs entail, why they exist, and how to manage them effectively is paramount to a smooth and financially sound property transfer.

Understanding the Components of Closing Costs

Closing costs are not a single, monolithic fee. Instead, they are an amalgamation of various charges, fees, and expenses that arise from the legal and administrative processes involved in transferring property ownership. These costs can vary significantly based on the location, the type of loan obtained, the price of the property, and the specific services rendered by professionals involved. For buyers, these costs typically represent a substantial out-of-pocket expense beyond the down payment, while sellers also incur their own set of closing expenses, often related to commissions and transfer taxes.

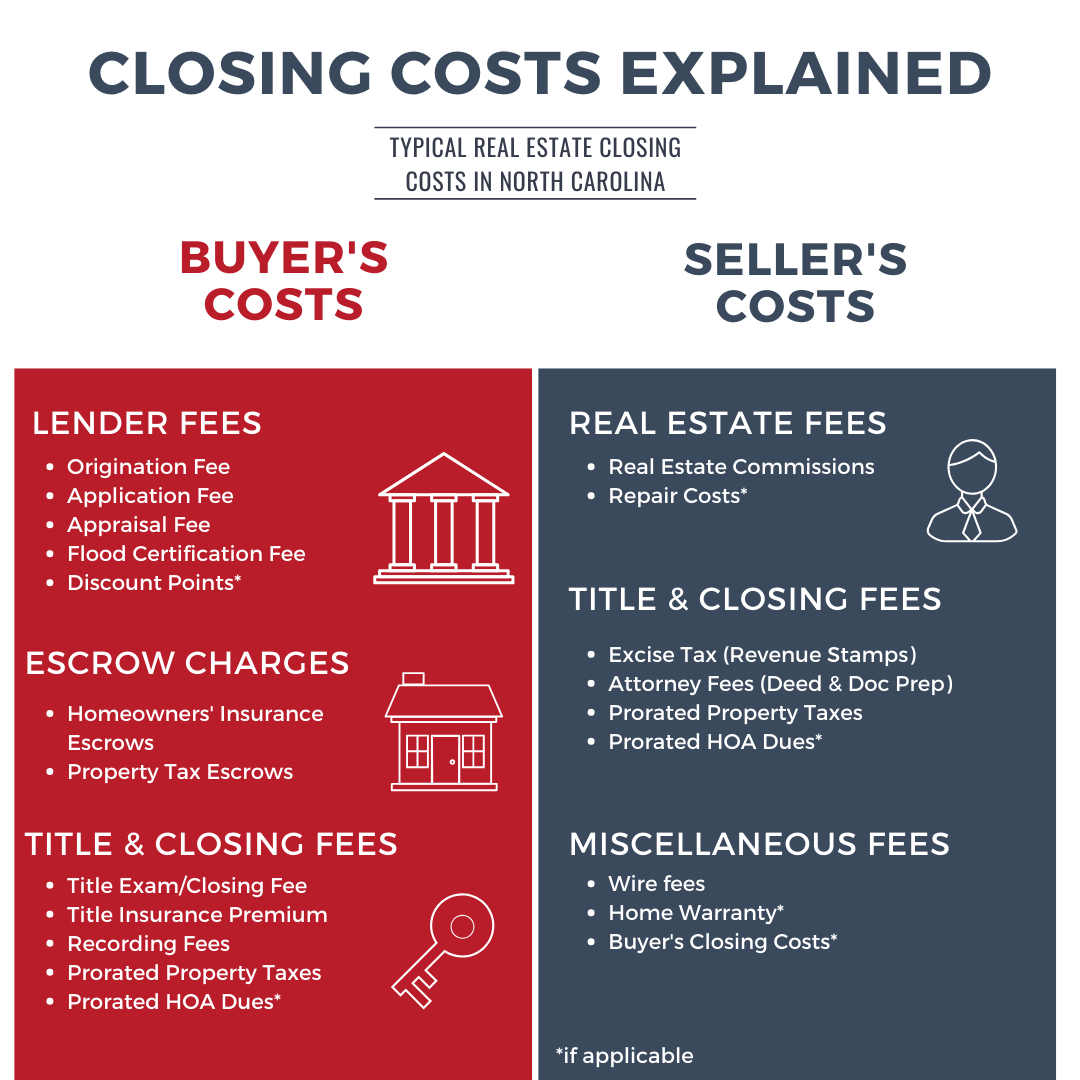

For the Buyer: The Buyer’s Closing Costs

For the buyer, closing costs are often more extensive and can range from 2% to 5% of the loan amount, or even higher in some markets. These costs are essential to secure the financing, ensure the property is legally sound, and officially transfer ownership into your name.

Origination Fees and Loan-Related Charges

These are fees charged by the lender for processing your mortgage application.

- Loan Origination Fee: This is a fee charged by the lender for processing and underwriting your mortgage application. It’s typically a percentage of the loan amount, often around 0.5% to 1%.

- Discount Points: While not always mandatory, buyers might choose to pay “points” to lower their interest rate over the life of the loan. One point is equal to 1% of the loan amount. This is a strategic decision that should be weighed against how long you plan to stay in the home.

- Underwriting Fee: The lender charges this fee to assess the risk of lending you money, verifying your financial information.

- Credit Report Fee: This covers the cost of obtaining your credit history and score from the three major credit bureaus.

- Appraisal Fee: A professional appraiser is hired to determine the market value of the property. Lenders require this to ensure the loan amount doesn’t exceed the home’s worth.

- Flood Certification Fee: This fee confirms whether the property is located in a flood zone, which would require flood insurance.

Title and Escrow Fees

These costs are associated with ensuring the property has a clear title and facilitating the transfer of funds and ownership.

- Title Search: A title company researches public records to ensure there are no liens, encumbrances, or ownership disputes on the property.

- Title Insurance: This is a crucial protection for both the lender and the buyer. Lender’s title insurance protects the lender against any title defects. Owner’s title insurance protects you, the buyer, against potential future claims against your ownership.

- Escrow Fee: The escrow company acts as a neutral third party to hold funds and documents until all conditions of the sale are met. They charge a fee for their services.

- Recording Fees: Local government agencies charge fees to record the new deed and mortgage in public records, making the ownership transfer official.

Pre-Paid Expenses and Reserves

These are not fees for services, but rather payments made in advance or set aside for future expenses.

- Homeowner’s Insurance Premium: Lenders typically require you to pay the first year’s premium upfront.

- Property Taxes: You’ll likely need to pay a portion of your property taxes, often for the remainder of the current tax period, and your lender will also collect a few months’ worth to establish an escrow account for future tax payments.

- Prepaid Interest: You’ll pay per diem interest on your loan from the closing date until the end of the month.

- HOA Dues (if applicable): If the property is part of a homeowner’s association, you may need to pay an initial fee or prorated dues.

Other Potential Buyer Costs

- Home Inspection Fee: While not always a mandatory closing cost required by the lender, a home inspection is highly recommended to identify any structural issues or necessary repairs before you commit to the purchase.

- Survey Fee: In some areas, a land survey is required to verify property boundaries.

- Attorney Fees: Depending on your state and local customs, you may need to hire a real estate attorney to review documents and represent your interests.

For the Seller: The Seller’s Closing Costs

While buyers often bear the brunt of closing costs, sellers also have their share of expenses that reduce their net proceeds from the sale. These costs are typically a percentage of the sale price.

Real Estate Agent Commissions

This is usually the largest expense for a seller. The commission is split between the buyer’s agent and the seller’s agent. Commissions are negotiable but typically range from 5% to 6% of the sale price.

Transfer Taxes and Recording Fees

- Transfer Tax/Stamps: Many states and some municipalities impose a tax on the transfer of real property from one owner to another. This is often a percentage of the sale price.

- Recording Fees: Similar to buyers, sellers may incur fees to record the deed and other necessary documents.

Outstanding Mortgage and Liens

- Payoff of Existing Mortgage: If you have an outstanding mortgage on the property, you will need to pay off the remaining balance at closing.

- Other Liens: Any other liens on the property, such as home equity loans or mechanic’s liens, must also be settled.

Attorney Fees and Other Miscellaneous Costs

- Attorney Fees: Similar to buyers, sellers may need to hire an attorney to handle legal aspects of the sale.

- Escrow Fees: While often shared, sellers might contribute to the escrow company’s fees.

- HOA Dues and Assessments: Any outstanding HOA dues or special assessments will need to be paid.

- Repairs and Seller Concessions: If agreed upon during negotiations, costs for agreed-upon repairs or seller concessions (e.g., contributing to the buyer’s closing costs) will be deducted from the seller’s proceeds.

Why Do Closing Costs Exist?

The existence of closing costs stems from the complex and legally binding nature of real estate transactions. Each fee serves a specific purpose in ensuring the transfer of property is conducted legally, accurately, and with adequate protection for all parties involved.

- Legal Protection: Title insurance and attorney fees are there to protect both the buyer and seller from potential legal disputes or undiscovered issues with the property’s ownership history.

- Financial Verification: Lender fees, appraisal, and credit report fees are necessary for the lender to assess the borrower’s ability to repay the loan and to ensure the property’s value supports the loan amount.

- Government Compliance: Recording fees and transfer taxes are governmental charges for the official registration of the property transfer and for revenue generation.

- Facilitation of the Transaction: Escrow fees compensate the neutral third party responsible for managing the funds and documents, ensuring all conditions of the sale are met before the exchange.

- Securing the Loan: Prepaid items like homeowner’s insurance and property taxes ensure that the property is protected and that the lender’s investment is secured from the outset.

Strategies for Managing and Reducing Closing Costs

While closing costs are often unavoidable, there are several strategies buyers and sellers can employ to manage and potentially reduce these expenses. Proactive planning and informed negotiation are key.

For Buyers: Strategies to Mitigate Closing Costs

- Shop Around for Lenders: Different lenders have varying fee structures. Obtaining Loan Estimates from multiple lenders and comparing them side-by-side can reveal significant savings on origination fees and other loan-related charges.

- Negotiate with the Seller: In a buyer’s market, or even in a competitive one, you might be able to negotiate for the seller to cover some of your closing costs. This can be done as a direct request or through a slightly higher purchase price.

- Look for Lender Credits: Some lenders may offer credits towards closing costs in exchange for a slightly higher interest rate. Evaluate this carefully to see if the long-term cost of the higher rate outweighs the upfront savings.

- Utilize First-Time Homebuyer Programs: Many state and local governments, as well as some non-profit organizations, offer assistance programs for first-time homebuyers that can help cover closing costs.

- Review Your Loan Estimate Carefully: Understand every fee listed on your Loan Estimate. Don’t hesitate to ask your loan officer for clarification. Some fees might be negotiable or could be reduced.

- Consider a No-Closing-Cost Mortgage: While these loans often come with a higher interest rate, they can be beneficial if you plan to move or refinance in a few years and want to minimize upfront expenses.

For Sellers: Strategies to Minimize Closing Costs

- Negotiate Agent Commissions: While agents’ commissions are a significant cost, they are negotiable. Discuss commission rates with potential agents early in the process.

- Understand and Negotiate Transfer Taxes: In some jurisdictions, transfer taxes are negotiable, or there might be exemptions based on certain criteria. Research local regulations.

- Be Prepared for Repairs: Addressing necessary repairs before listing your home can prevent them from becoming a point of negotiation and a costly concession to the buyer at closing.

- Choose Your Service Providers Wisely: For services like title insurance or escrow, while often selected by the buyer’s lender, you might have some influence or be able to research competitive pricing.

The Closing Disclosure: Your Final Statement

Once you’re nearing the end of the transaction, typically within three business days of closing, you will receive a Closing Disclosure. This is a standardized five-page document that details all the final loan terms, projected monthly payments, and a precise breakdown of all your closing costs. It’s crucial to compare this document with your initial Loan Estimate. Any significant discrepancies should be questioned and clarified with your lender immediately. The Closing Disclosure serves as the final accounting of the transaction, and understanding it is the last step in ensuring a clear financial picture before you officially take possession of your new home or hand over the keys to your sold property.

In conclusion, closing costs are an intrinsic part of any real estate transaction. By understanding their composition, their purpose, and by employing smart financial strategies, both buyers and sellers can navigate this essential expense with greater confidence and achieve a more favorable outcome.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.