In the modern financial landscape, where digital transactions have largely superseded physical cash, the security of our personal finance tools is of paramount importance. Among the various codes and numbers embossed on a plastic card, the CID—or Card Identification Number—stands as a critical line of defense against fraud. For the savvy consumer and the business professional alike, understanding the nuances of the CID is not just about completing a purchase; it is about maintaining the integrity of one’s financial identity.

This article explores the definition, utility, and strategic importance of the CID in the context of personal finance, digital security, and modern banking.

Decoding the CID: Definitions and Physical Locations

To the uninitiated, the back (or front) of a credit card can appear to be a jumble of random digits. However, in the world of financial tools, every number serves a specific purpose. The CID is a multi-digit security code used to verify that the person making a purchase actually possesses the physical card during a “card-not-present” (CNP) transaction, such as those conducted online or over the phone.

CID vs. CVV: Navigating the Acronyms

While the terms CID, CVV (Card Verification Value), and CVC (Card Validation Code) are often used interchangeably by merchants, they technically refer to specific protocols used by different card networks.

- CID: Primarily used by American Express and Discover.

- CVV/CVV2: The standard terminology for Visa.

- CVC/CVC2: The standard terminology for Mastercard.

Despite the different names, their function remains identical: providing an extra layer of authentication that is not stored in the magnetic stripe or the EMV chip, making it harder for hackers to steal via traditional card readers.

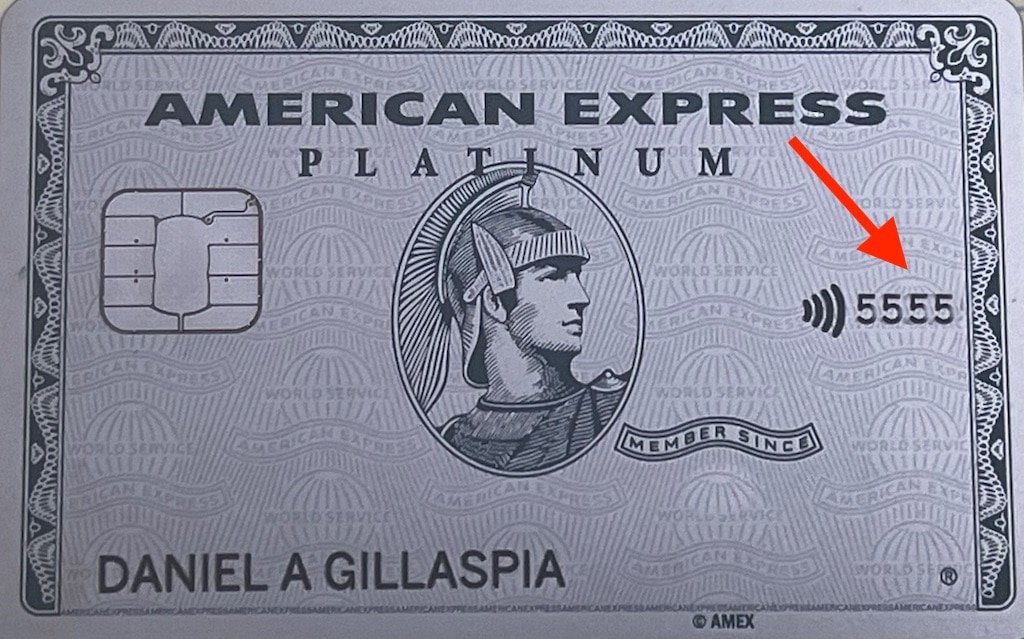

Where to Find the CID on Your Card

The placement of the CID varies significantly depending on the card issuer, which is a common point of confusion for consumers. For American Express users, the CID is a four-digit code located on the front of the card, usually positioned above and to the right of the main credit card number. In contrast, Discover, Visa, and Mastercard typically place a three-digit code on the back of the card, often located within or just to the right of the signature panel.

The Role of Non-Embossed Digits

Unlike the primary 16-digit account number, the CID is almost never embossed (raised). It is printed using thermal ink or laser-etched. This is a deliberate design choice in personal finance security. Embossed numbers can be easily “rubbed” or copied through carbon paper—a relic of older merchant processing—whereas the flat-printed CID requires a clear visual line of sight, ensuring it is only accessible to the person holding the physical card.

The Strategic Role of CID in Financial Security

In the realm of personal finance and business operations, the CID acts as a gatekeeper. As e-commerce continues to dominate the retail sector, the risk of data breaches increases. The CID is a crucial component of the Payment Card Industry Data Security Standard (PCI DSS).

Preventing Card-Not-Present (CNP) Fraud

CNP fraud occurs when a criminal uses stolen card information to make purchases online. Since the thief often obtains the primary account number and expiration date through database leaks or phishing, they may lack the CID. Most modern payment gateways require the CID to authorize a transaction. By requiring this code, financial institutions can significantly filter out fraudulent attempts, protecting the cardholder’s balance and the merchant’s revenue from chargebacks.

Why Merchants Cannot Store Your CID

One of the most robust features of the CID system is the legal and technical restriction on its storage. According to PCI compliance rules, even if a merchant stores your credit card number for “one-click” future shopping, they are strictly prohibited from storing the CID. This is why, even on sites like Amazon or Apple, you are occasionally asked to re-enter your security code. If a merchant’s database is hacked, the CID won’t be there for the taking, rendering the stolen card numbers much less useful to the attacker.

Verification vs. Authorization

It is important to understand the distinction between card authorization and CID verification. A transaction can be “authorized” by a bank (meaning there are sufficient funds), but “declined” by the merchant’s payment processor if the CID does not match. This dual-verification process is a cornerstone of professional financial risk management, ensuring that liquidity is only accessed by the rightful owner.

CID and Modern Personal Finance Management

For individuals managing their own portfolios and daily expenses, the CID is more than just a number; it represents the “key” to their liquid assets. Proper management of this information is essential for maintaining a healthy credit score and avoiding the bureaucratic nightmare of identity theft.

Best Practices for Protecting Your CID

In the context of personal finance, “information hygiene” is vital. Users should never share their CID via email or text message, as these channels are often unencrypted. Additionally, when using a card at a physical location, such as a restaurant or gas station, one should be wary of “skimming” devices or employees who take the card out of sight for an extended period. Some extreme privacy advocates even go as far as placing a small piece of opaque tape over the CID to prevent “shoulder surfing” or recording by CCTV cameras.

Virtual Credit Cards and Dynamic CIDs

As financial tools evolve, we are seeing the rise of “Virtual Credit Cards” (VCCs). Offered by many fintech apps and premium credit card issuers, VCCs generate a temporary card number and a dynamic CID. This CID may only be valid for a single transaction or a 24-hour period. This is the gold standard for online income protection and secure side-hustle spending, as it ensures that even if a site is compromised, the CID the hacker finds is already obsolete.

Impact on Credit Health and Disputes

If a CID is compromised and a fraudulent transaction occurs, the speed at which you report it is linked to your financial liability. Under the Fair Credit Billing Act, cardholders are generally protected against unauthorized charges. However, demonstrating that you have practiced due diligence—such as keeping your CID private—can expedite the dispute process with your bank’s fraud department.

Troubleshooting and Technical Challenges with CID

Even the most seamless financial systems encounter friction. Understanding why a CID might be rejected can save time and prevent a temporary freeze on your account.

Common Reasons for CID Failures

The most frequent cause of a CID error is simple human entry error. Because the digits are small and sometimes fade over time, it is easy to misread them. However, if the code is entered correctly and still fails, it may indicate that the card has been flagged for suspicious activity or that the bank’s verification server is temporarily offline. In some cases, if you have recently received a replacement card, the old CID is immediately invalidated, even if the primary 16-digit number remains the same.

The Problem of Faded Digits

On older cards, the printed CID can wear off due to friction with a wallet or purse. From a financial management perspective, a card with an illegible CID is a liability. If you cannot read your code, you cannot make online purchases. In this scenario, it is professionally recommended to request a replacement card immediately rather than trying to guess the code, as multiple incorrect attempts can lead to a “hard block” on your account.

Merchant Side Implementation

For business owners and those interested in business finance, implementing CID requirements on your checkout page is a fundamental step in reducing “friendly fraud” and legitimate theft. While requiring the CID adds a small amount of “friction” to the checkout process, the trade-off in security and reduced merchant fees (as banks often charge lower processing rates for CID-verified transactions) makes it an essential strategy for any online enterprise.

The Future of Transaction Authentication: Beyond the CID

As we look toward the future of money and investing, the traditional static CID may eventually be phased out in favor of more advanced biometric and cryptographic solutions.

Biometric Integration

Some innovators in the financial sector are testing cards with built-in fingerprint scanners. In this model, the “CID” is essentially your biometric signature. Until this becomes a global standard, the printed CID remains the most practical and universal tool for verifying card ownership in the digital space.

Tokenization and the Death of the Physical Card

With the rise of Apple Pay, Google Pay, and Samsung Pay, the physical CID is becoming less visible to the consumer. These services use “tokenization,” where a unique digital token is created for each transaction. The CID is replaced by a one-time cryptographic code generated by the device’s secure element. This technology offers a glimpse into a future where the manual entry of a CID is a thing of the past, yet the logic of the CID—an extra piece of one-time-use information—remains the backbone of the system.

Conclusion: The Cornerstone of Financial Integrity

What is a CID credit card code? It is more than just a three or four-digit sequence; it is a vital instrument of financial security. Whether you are a consumer protecting your personal savings or a business professional managing corporate accounts, the CID is your primary defense against the growing tide of digital fraud. By understanding how it works, where it is located, and how to protect it, you ensure that your financial journey remains secure, efficient, and uncompromised in an increasingly connected world.

Maintaining vigilance over your CID is not just a safety measure—it is a sophisticated approach to managing your most valuable financial tools. As technology evolves, the CID reminds us that in the world of money, the simplest layer of security is often the most effective.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.