California, the Golden State, is renowned for its vibrant economy, technological innovation, and stunning natural beauty. It’s also known for having one of the most complex and robust taxation systems in the United States. For residents, businesses, and even those considering a move or expanding operations to California, understanding “what is CA tax” is not just a matter of compliance, but a crucial element of financial planning and economic foresight. This guide aims to demystify California’s multi-layered tax landscape, providing an insightful and professional overview of its key components.

The sheer size of California’s economy, the largest in the U.S. and among the largest globally, necessitates a substantial revenue stream to fund its extensive public services, infrastructure projects, and social programs. This revenue is primarily generated through a diverse array of taxes, including personal income tax, corporate taxes, sales and use tax, and property tax, alongside numerous other specialized fees and levies. Navigating these various taxes requires a clear understanding of their mechanics, who they apply to, and how they impact individuals and businesses alike. Failure to grasp these intricacies can lead to significant financial penalties, missed opportunities for tax savings, and operational inefficiencies. This article will break down the essential elements of California’s taxation, offering a roadmap for compliance and strategic planning within this dynamic financial environment.

Understanding California’s Income Tax Structure

California’s approach to taxing income is one of its most defining financial characteristics, significantly impacting individuals and businesses operating within its borders. Both personal and corporate income taxes are key pillars of the state’s revenue generation.

Personal Income Tax (PIT)

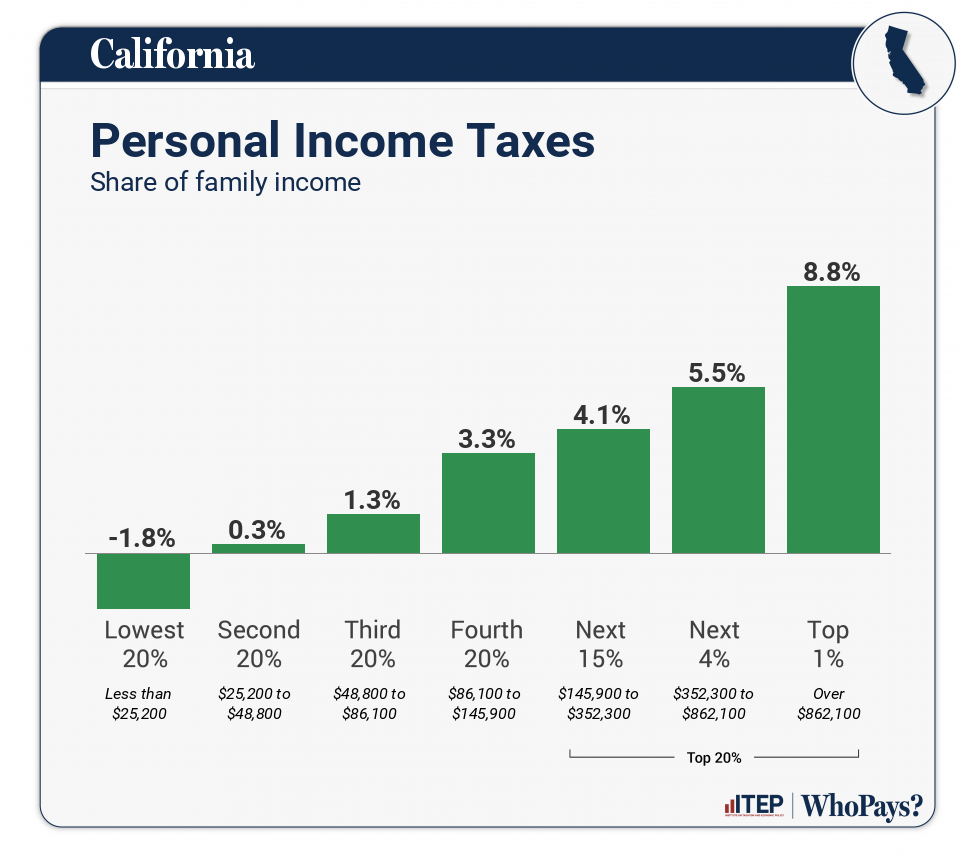

California operates a highly progressive personal income tax system, meaning that as an individual’s taxable income increases, so does the percentage of tax they pay. This system features a relatively high top marginal tax rate compared to most other states. For tax year 2023, the marginal tax rates range from 1% to 12.3%, with an additional 1% surcharge on taxable income over $1 million, often referred to as the “mental health services tax,” bringing the effective top rate to 13.3%. This structure is designed to distribute the tax burden more heavily towards higher earners.

Who needs to file California income tax returns extends beyond just full-time residents. Part-year residents are taxed on the income earned while residing in California, as well as on any California-sourced income during their non-residency period. Non-residents are taxed solely on income derived from California sources, such as wages from work performed in the state, income from a California business, or gains from the sale of California real estate. Understanding these residency rules is paramount, as misclassification can lead to significant tax liabilities or unnecessary filings.

Taxpayers can reduce their taxable income through various deductions, credits, and exemptions. Common deductions include certain contributions to IRAs, student loan interest, and itemized deductions (though California’s itemized deductions differ from federal ones). Credits, such as the California Earned Income Tax Credit (CalEITC), Dependent Exemption Credit, and Nonrefundable Renter’s Credit, directly reduce the amount of tax owed, offering targeted relief to specific groups of taxpayers. Staying informed about available tax benefits is crucial for minimizing one’s overall tax burden.

Corporate Income Tax (CIT)

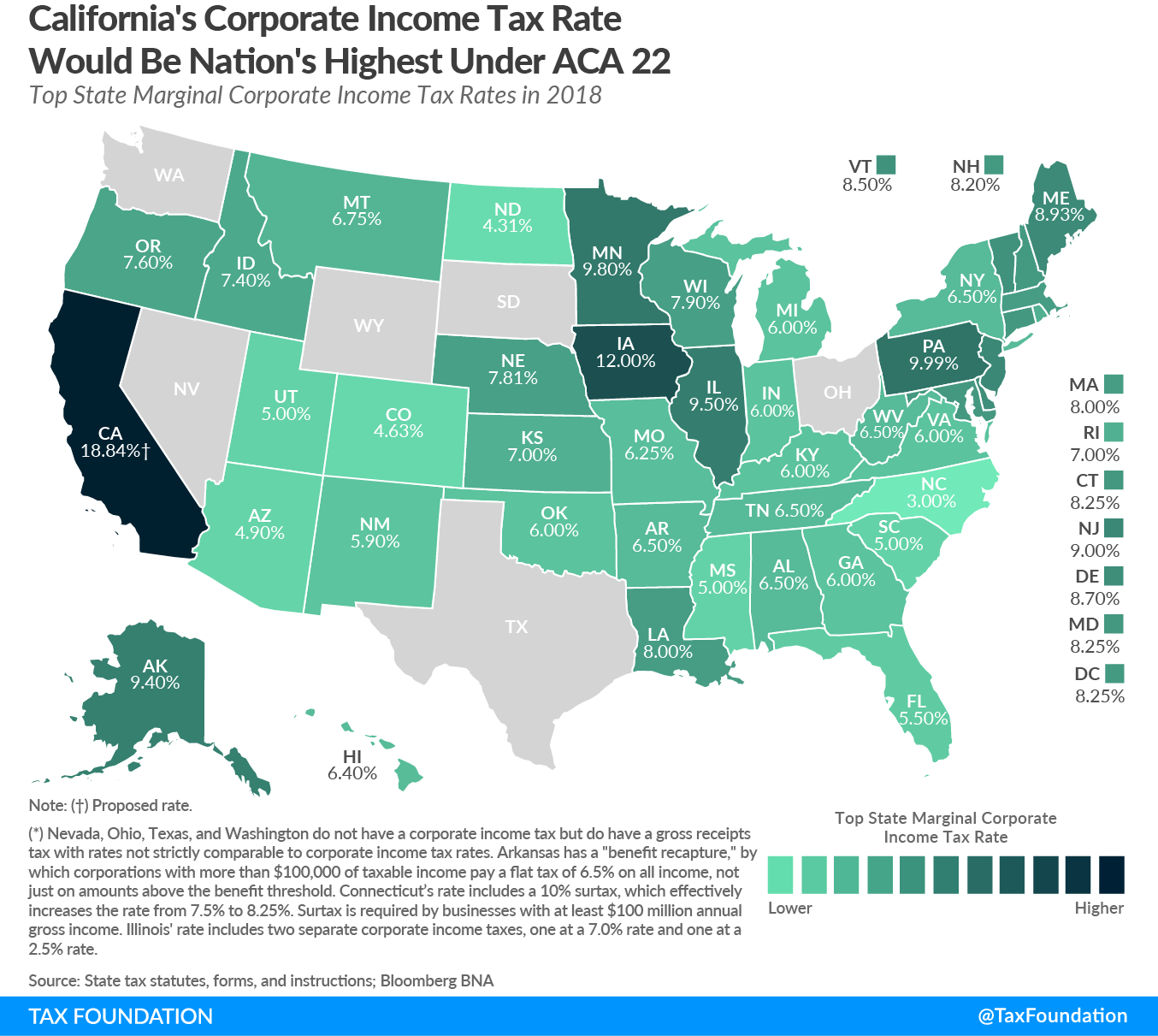

For businesses, California’s corporate income tax system presents its own set of considerations. The state generally imposes a flat corporate income tax rate of 8.84% on C-corporations, a rate that applies regardless of the corporation’s income level (above a certain threshold). This contrasts with the federal progressive corporate tax system and makes California’s rate among the highest in the nation for corporations.

Additionally, California imposes a minimum franchise tax. This is an annual tax of $800 that applies to most corporations, limited liability companies (LLCs) taxed as corporations, and limited partnerships that are registered or doing business in California, regardless of whether they generate any income or even operate at a loss. This minimum tax is a fixed cost of doing business in the state and must be factored into financial planning for all corporate entities.

The distinction between S-corporations and C-corporations is also significant in California. While S-corporations generally avoid double taxation at the federal level (income is passed through to shareholders and taxed only at the individual level), California imposes a 1.5% entity-level tax on S-corporations’ net income, with a minimum $800 franchise tax. C-corporations, by contrast, are subject to the 8.84% corporate tax, and shareholders are then taxed again on any dividends received, leading to the “double taxation” scenario. A notable recent development is the Pass-Through Entity (PTE) tax election, introduced to help mitigate the impact of the federal State and Local Tax (SALT) deduction cap. Eligible pass-through entities (like S-corporations and partnerships) can elect to pay a 9.3% tax on qualified net income at the entity level, allowing owners to claim a credit against their personal income tax. This can be a valuable tax planning tool for many California businesses.

Sales, Use, and Property Taxes in the Golden State

Beyond income, California’s tax system extensively leverages consumption and property ownership to generate revenue, impacting nearly every transaction and property owner within the state.

California Sales and Use Tax

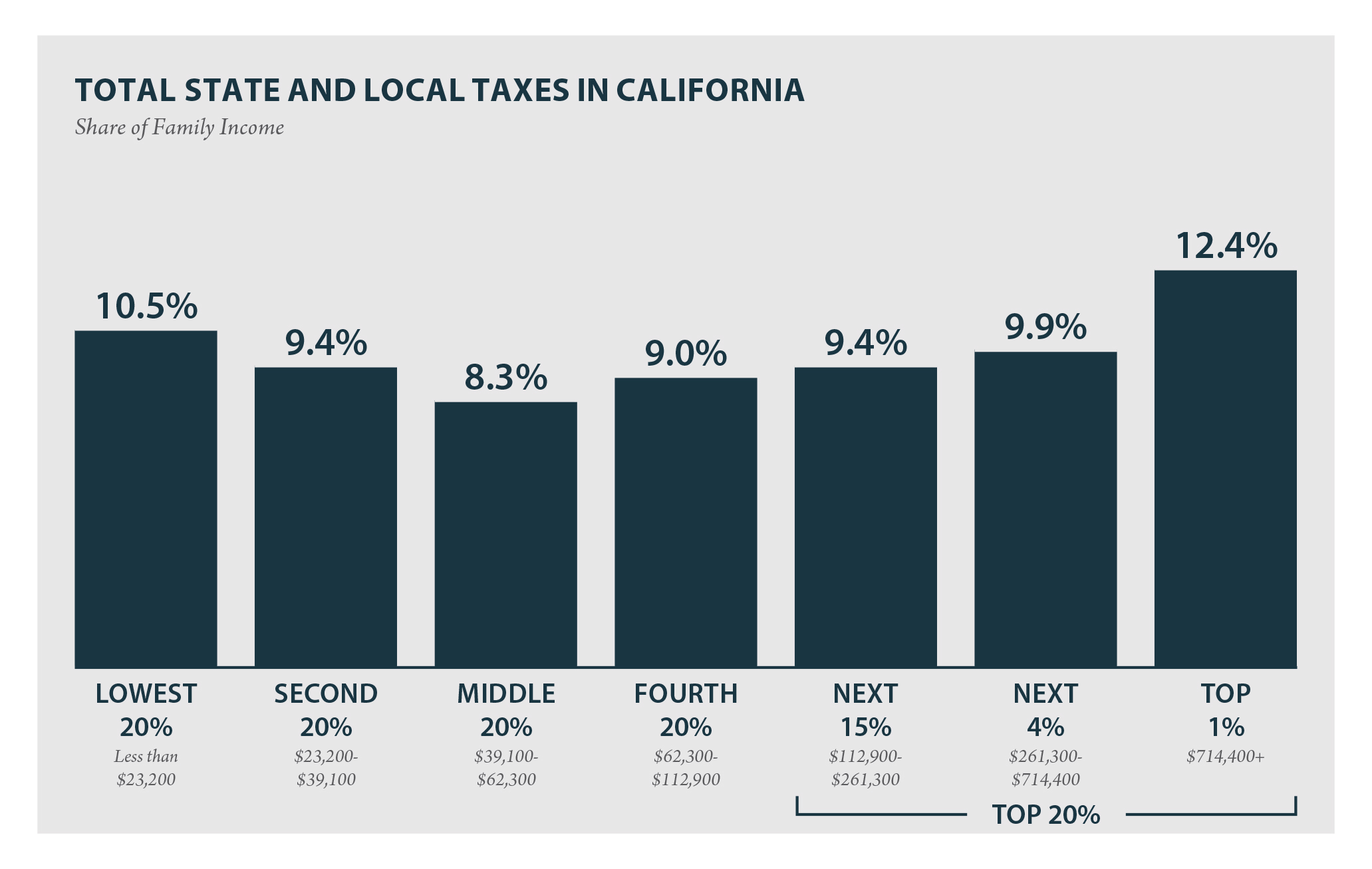

The California Sales and Use Tax is a critical component of the state’s revenue, applied to the sale of most tangible personal property and some services. The statewide base sales tax rate is 7.25%. However, this is rarely the rate consumers actually pay. Local jurisdictions (cities, counties, and special districts) have the authority to impose additional district taxes, which can push the combined sales tax rate significantly higher. For example, some areas within California can see combined rates exceeding 10%. These local taxes fund various municipal services, transportation projects, and other community initiatives.

Understanding what goods and services are taxable versus exempt is crucial for both businesses making sales and consumers making purchases. Generally, tangible personal property is taxable, while most services are not, unless they are integral to the sale of a tangible product (e.g., fabrication labor). Essential items like most food products purchased for home consumption, prescription medicines, and certain medical devices are typically exempt. Businesses are responsible for collecting sales tax from customers and remitting it to the California Department of Tax and Fee Administration (CDTFA). For consumers, the use tax comes into play when they purchase tangible personal property outside of California (e.g., online from an out-of-state vendor) for use within the state, and sales tax was not collected by the seller. The use tax rate is the same as the combined sales tax rate in the consumer’s location, ensuring that all goods consumed in California, regardless of where they were purchased, contribute to state revenue.

Property Tax Fundamentals

California’s property tax system is famously anchored by Proposition 13, a ballot initiative passed in 1978 that dramatically altered how real estate is assessed and taxed. Under Prop 13, a property’s assessed value is generally its fair market value as of the date of purchase or new construction. This base year value can only increase by a maximum of 2% per year, regardless of how much the actual market value of the property appreciates. This cap on annual increases provides a significant benefit to long-term property owners, protecting them from rapidly escalating property tax bills based on market fluctuations.

However, a property’s assessed value is “reassessed” to its current market value upon a change of ownership or new construction. This means that when a property is sold, the new owner typically faces a significantly higher property tax bill based on the purchase price. Similarly, adding substantial new construction to an existing property can trigger a reassessment of the newly constructed portion. “Supplemental assessments” can also occur when a property is reassessed during the tax year. These are additional tax bills that cover the period from the date of change in ownership or completion of new construction to the end of the current tax year, reflecting the difference between the old and new assessed values.

Several exemptions exist to provide relief to eligible property owners. The Homeowners’ Exemption reduces the taxable value of an owner-occupied primary residence by $7,000, resulting in a modest tax saving. The Veterans’ Exemption offers a more substantial reduction for qualifying veterans or their surviving spouses. Understanding these exemptions and when a property’s assessed value can change is critical for managing property tax liabilities, which are generally collected by county tax assessors and treasurers.

Other Significant California Taxes

California’s tax reach extends beyond income, sales, and property, encompassing a broad spectrum of taxes and fees designed to fund specific services, regulate certain industries, or address societal costs.

Payroll Taxes

For businesses with employees, payroll taxes represent a significant financial obligation and administrative responsibility. California mandates several state-specific payroll taxes, including Unemployment Insurance (UI), Employment Training Tax (ETT), State Disability Insurance (SDI), and Paid Family Leave (PFL). UI and ETT are typically employer-paid, funding benefits for unemployed workers and job training programs, respectively. The UI tax rate is variable, based on an employer’s experience rating. SDI and PFL are primarily employee-funded through payroll deductions, providing benefits for non-work-related illnesses or injuries and for bonding with a new child or caring for a seriously ill family member.

Employers are responsible for withholding these taxes from employee wages (where applicable), calculating the employer’s share, and remitting them to the Employment Development Department (EDD), along with filing regular payroll reports. Proper classification of workers (employee vs. independent contractor) is also a critical issue, as misclassification can lead to substantial penalties for unpaid taxes and missed benefits. These payroll taxes are vital for maintaining California’s social safety nets and workforce development programs.

Special Taxes and Fees

California levies various special taxes and fees, often designed to target specific goods, activities, or industries, or to fund particular initiatives. The gasoline excise tax, for instance, is a per-gallon tax applied to motor fuel sales, with revenues primarily dedicated to funding transportation infrastructure projects like road maintenance and public transit. California has one of the highest gas taxes in the nation, reflecting its commitment to infrastructure and environmental goals.

Tobacco taxes are another significant source of revenue, with funds often earmarked for health programs and anti-smoking campaigns. The state has incrementally increased these taxes over the years, aligning with public health efforts to reduce tobacco consumption. A more recent addition to California’s tax landscape is the cannabis excise and cultivation taxes, following the legalization of recreational marijuana. These taxes apply at various points in the supply chain, from cultivation to retail sale, with revenues directed towards public health, safety, and environmental programs.

Beyond these, numerous other fees and taxes exist, such as vehicle registration fees (which include various charges for vehicle licenses, weight fees, and specialized plates) that contribute to state transportation and environmental initiatives. While California does not have a state-level estate tax (unlike some other states), its residents are still subject to the federal estate tax if their estate exceeds the federal exemption threshold. Understanding this array of special taxes is crucial for businesses operating in specific sectors and for individuals making purchases or owning assets subject to these levies.

Local Taxes and Assessments

In addition to state-level taxes, individuals and businesses in California must contend with a myriad of local taxes and assessments imposed by cities, counties, and special districts. These local levies are essential for funding municipal services that directly impact daily life, such as police and fire departments, parks, libraries, and local infrastructure.

Common local taxes include business licenses, which most businesses are required to obtain and renew annually to operate legally within a city or county. The fees for these licenses vary widely based on the type of business, its gross receipts, or the number of employees. Utility user taxes (UUT) are another widespread local tax, typically applied to services like electricity, gas, water, and telephone/cell phone usage. These taxes are collected by the utility providers and remitted to the local jurisdiction.

Furthermore, many communities impose tourism assessments or transient occupancy taxes (TOT) on hotel stays and short-term rentals, with revenues often used to promote tourism and fund local services. Property owners might also face special assessments, such as Mello-Roos Community Facilities District (CFD) taxes, which are imposed to finance specific public improvements or services (e.g., schools, parks, sewers) within a defined area. These assessments are typically added to property tax bills and can significantly increase the total amount paid. Navigating these diverse local taxes requires close attention to municipal regulations and an understanding of how they apply to specific properties or business operations.

Navigating California Tax Compliance and Planning

Understanding the various components of California’s tax system is only half the battle; effective compliance and strategic planning are essential to mitigate risks and optimize financial outcomes. This involves knowing which regulatory bodies govern each tax, avoiding common pitfalls, and adopting proactive strategies.

Key Regulatory Bodies

California’s tax administration is fragmented across several major state agencies, each responsible for different aspects of taxation. For personal and corporate income taxes, the Franchise Tax Board (FTB) is the primary authority. The FTB handles income tax returns, audits, collections, and taxpayer inquiries. Businesses dealing with sales and use tax, cannabis taxes, fuel taxes, and other special taxes and fees will interact with the California Department of Tax and Fee Administration (CDTFA). The CDTFA is responsible for administering dozens of programs, from sales tax permits to tobacco licenses.

Payroll taxes, including UI, ETT, SDI, and PFL, fall under the jurisdiction of the Employment Development Department (EDD). The EDD manages employer accounts, processes claims for benefits, and enforces compliance with state labor and payroll tax laws. Finally, property taxes are primarily administered at the county level by County Assessors, who determine property values, and County Treasurers/Tax Collectors, who handle billing and collection. Each of these agencies has its own set of rules, filing requirements, and enforcement mechanisms, underscoring the need for careful attention to detail.

Common Pitfalls and How to Avoid Them

The complexity of California’s tax system creates numerous opportunities for common errors that can lead to penalties and audits. One frequent pitfall is underestimating tax liability, particularly for new residents or businesses unaccustomed to California’s higher rates and unique levies. This can lead to underpayment penalties. Missing deadlines for filing returns or making payments is another common issue, triggering late fees and interest charges. California has stringent deadlines for various taxes, and they often differ from federal deadlines.

Incorrectly classifying income or expenses can also be problematic. For individuals, misinterpreting what constitutes California-sourced income or failing to correctly apply deductions and credits can result in errors. For businesses, misclassifying workers as independent contractors instead of employees can lead to significant back taxes, penalties, and interest from the EDD. Additionally, failing to keep adequate records is a pervasive issue. Comprehensive and organized records are essential to substantiate deductions, credits, and reported income/expenses during an audit. Finally, ignoring local tax requirements, such as business licenses or utility user taxes, can lead to localized penalties and operational disruptions. Proactive engagement with these requirements is key.

Strategies for Effective Tax Planning

Effective tax planning in California involves a proactive and informed approach. A fundamental strategy is to fully utilize available deductions and credits. For individuals, this means exploring options like the CalEITC, educational credits, and specific itemized deductions. For businesses, understanding depreciation rules, business expense deductions, and credits for research and development or job creation can significantly reduce taxable income.

Understanding residency rules is paramount for individuals, especially those with multi-state activities or who have recently moved to or from California. Proper residency classification can have a profound impact on one’s personal income tax obligations. For businesses, strategic business structuring is crucial. Choosing the appropriate entity type (sole proprietorship, partnership, LLC, S-corp, C-corp) has significant tax implications, and regularly reviewing this structure, especially in light of new tax laws like the PTE election, can yield substantial benefits.

Given the intricacy of California’s tax code, seeking professional advice from qualified tax accountants, attorneys, or financial advisors is often the most effective strategy. These professionals can provide tailored guidance, ensure compliance, identify opportunities for tax savings, and represent taxpayers during audits. Lastly, staying updated on legislative changes is critical. California’s tax laws are subject to frequent amendments, and what was true last year may not be this year. Subscribing to tax alerts, attending seminars, and consulting with professionals can help individuals and businesses remain compliant and agile in their tax planning.

Conclusion

Understanding “what is CA tax” means recognizing the multi-faceted nature of California’s taxation system, which is arguably one of the most comprehensive and impactful in the nation. From the progressive personal income tax and the robust corporate tax structure, to the pervasive sales and use tax, and the unique property tax framework dictated by Proposition 13, California’s levies touch nearly every aspect of economic activity. Added to this are the critical payroll taxes, a myriad of special taxes and fees, and the diverse landscape of local taxes and assessments, all contributing to the Golden State’s substantial revenue base.

Navigating this intricate system demands more than just a cursory understanding; it requires diligence, attention to detail, and a proactive approach to compliance and planning. Whether you are an individual resident, a small business owner, or a large corporation, the implications of California’s tax policies are profound. By understanding the roles of key regulatory bodies like the FTB, CDTFA, and EDD, being aware of common pitfalls, and implementing sound tax planning strategies, taxpayers can effectively manage their obligations. In a state as economically dynamic and legislatively active as California, staying informed and seeking expert guidance are not just advisable—they are indispensable tools for financial success and peace of mind.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.