In the wake of the 2008 global financial crisis, an anonymous figure (or group) known as Satoshi Nakamoto released a whitepaper that would forever alter the trajectory of global economics. Titled “Bitcoin: A Peer-to-Peer Electronic Cash System,” it proposed a radical alternative to the traditional banking system. Today, Bitcoin has evolved from a niche experiment for cryptographers into a trillion-dollar asset class, often referred to as “digital gold.”

To understand Bitcoin from a financial perspective, one must look beyond the code and see it for what it truly is: a sovereign monetary system that operates without the need for a central bank, a government, or a middleman. This article explores the mechanics of Bitcoin through the lens of personal and business finance, examining how it functions as a store of value and its role in the future of global wealth.

The Evolution of Currency: Understanding Bitcoin’s Role in Modern Finance

To appreciate why Bitcoin is significant, we must first understand the limitations of the current financial paradigm. For centuries, humanity has relied on centralized authorities—kings, governments, and central banks—to issue and regulate currency. While this system provides stability during periods of growth, it is susceptible to human error, political manipulation, and the silent tax of inflation.

From Barter to Bits: The History of Money

Money is essentially a tool used to transport value across time and space. Throughout history, we have used shells, salt, gold, and eventually paper fiat currency. Each evolution aimed to make money more “saleable”—easier to store, transport, and divide. However, paper currency (fiat) lacks the scarcity that gave gold its value. Since the abandonment of the gold standard in 1971, the purchasing power of global currencies has steadily declined as central banks print more money to manage national debts.

Bitcoin represents the next logical step in this evolution. It combines the scarcity and durability of gold with the portability and divisibility of digital data. Unlike fiat currency, which can be printed at will, Bitcoin is the first “hard” digital asset.

Decentralization: Why the Absence of Central Banks Matters

The cornerstone of Bitcoin’s financial appeal is decentralization. In traditional finance, if you want to send money to someone across the world, you must rely on a series of intermediaries: your bank, their bank, and clearinghouses like SWIFT. Each of these entities takes a fee, and any of them can freeze your funds or deny the transaction.

Bitcoin operates on a peer-to-peer network. There is no “Bitcoin Inc.” or CEO. Instead, the system is maintained by a global network of computers (nodes) that follow a consensus protocol. For the individual investor, this means “financial sovereignty.” You are the sole custodian of your wealth, and no central authority can devalue your holdings through inflationary policies or restrict your access to your capital.

The Economic Mechanism: How the Bitcoin Network Operates as a Financial System

While the technical architecture of Bitcoin involves complex cryptography, its economic mechanism is remarkably simple and transparent. It is a digital ledger—an accounting book that records every transaction ever made—that is visible to everyone but controlled by no one.

Scarcity and the 21 Million Cap

In the world of investing, scarcity is a primary driver of value. Bitcoin’s monetary policy is hard-coded into its protocol: there will only ever be 21 million bitcoins. This is a stark contrast to the U.S. Dollar or the Euro, where the supply is elastic and determined by policy committees.

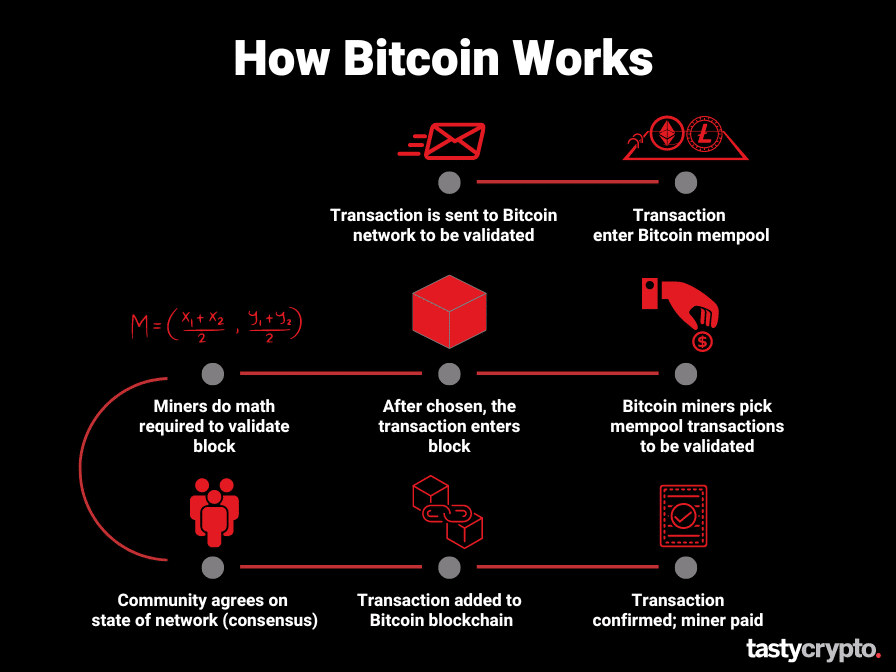

Approximately every ten minutes, a new “block” of transactions is added to the ledger, and a specific amount of new Bitcoin is issued to the “miners” who secure the network. However, every four years, an event known as the “Halving” occurs, where the issuance of new Bitcoin is cut by 50%. This programmatic scarcity ensures that Bitcoin becomes harder to acquire over time, mimicking the extraction of precious metals from the earth. From an investment standpoint, this “Stock-to-Flow” ratio is what attracts those seeking a hedge against inflation.

Proof of Work: Securing the Ledger through Economic Incentives

How can we trust a financial system with no bank? The answer lies in “Proof of Work” (PoW). This is the process where miners use high-powered computers to solve complex mathematical puzzles. The first miner to solve the puzzle earns the right to add the next block to the blockchain and receives the block reward in Bitcoin.

This is not just a technical process; it is an economic security model. To “attack” the network or double-spend a coin, an actor would need to control more than 51% of the network’s computing power, which would cost billions of dollars in electricity and hardware. Thus, Bitcoin uses the laws of physics and economics to secure its ledger, making it the most secure financial network in human history.

Bitcoin as an Asset Class: Investing, Store of Value, and Risk Management

As Bitcoin has matured, its role in a diversified financial portfolio has shifted. Once viewed as a speculative gamble, it is now being embraced by institutional investors, hedge funds, and even public corporations like MicroStrategy and Tesla.

Digital Gold vs. Medium of Exchange

There is a frequent debate in the financial world: Is Bitcoin a currency or an investment? While it can be used to buy goods and services, its current primary function is as a “Store of Value.”

Gold has served this purpose for millennia because it is difficult to find and impossible to manufacture. Bitcoin improves upon gold’s properties: it is easier to verify, cheaper to transport, and can be divided down to eight decimal places (the smallest unit being a “Satoshi”). For the personal investor, Bitcoin serves as a “prudent insurance policy” against the systemic risks of traditional fiat-based economies.

Market Volatility and Long-term Investment Strategies

One cannot discuss Bitcoin as a financial tool without addressing its volatility. Because the market for Bitcoin is relatively small compared to global real estate or equities, large trades can cause significant price swings. However, for those with a multi-year time horizon, this volatility is often viewed as the “price of admission” for outsized gains.

Financial advisors who include Bitcoin in their strategies often recommend “Dollar Cost Averaging” (DCA)—the practice of investing a fixed amount of money at regular intervals regardless of the price. This mitigates the risk of buying at a temporary peak and allows the investor to build a position in what has historically been the best-performing asset class of the last decade.

Practical Integration: Using Bitcoin in Personal and Business Finance

Integrating Bitcoin into your financial life requires a shift in mindset regarding how we store and move value. Unlike a bank account, where the bank holds the money on your behalf, Bitcoin requires you to take personal responsibility for your assets.

Wallets and Custody: Managing Your Digital Wealth

In the Bitcoin ecosystem, the phrase “Not your keys, not your coins” is a fundamental rule. When you keep Bitcoin on an exchange like Coinbase or Binance, you are essentially holding a “promise” of payment. To truly own your Bitcoin, you must move it to a private wallet where you control the “private keys.”

For serious investors, “Cold Storage” (hardware wallets that are not connected to the internet) is the gold standard for security. This eliminates the risk of exchange hacks and ensures that your digital wealth is as secure as a physical vault, yet accessible from anywhere in the world with an internet connection.

The Future of Bitcoin in Global Trade and Remittances

Beyond personal investment, Bitcoin is revolutionizing business finance, particularly in the realm of cross-border payments. Traditional remittances can take days to clear and cost upwards of 7% in fees. Bitcoin allows for the near-instant transfer of value across borders for a fraction of the cost.

With the advent of the “Lightning Network”—a secondary layer built on top of Bitcoin—transactions can now be processed in milliseconds with virtually zero fees. This makes Bitcoin a viable tool for micro-payments and global trade, allowing a small business in Africa to receive payment from a customer in London without the friction of the traditional banking corridor.

Conclusion: The Sovereign Financial Future

Bitcoin is more than just a technological innovation; it is a fundamental rethink of how we define and exchange value. By decoupling money from the state, it offers individuals a way to protect their purchasing power and participate in a global economy that is transparent, scarce, and permissionless.

Whether viewed as a high-growth investment, a hedge against inflation, or a tool for financial inclusion, Bitcoin’s influence on the world of money is undeniable. As the traditional financial system grapples with rising debts and devalued currencies, the decentralized, 21-million-cap model of Bitcoin provides a compelling alternative for the digital age. Understanding how it works is no longer just for the tech-savvy; it is an essential component of modern financial literacy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.