In the complex landscape of personal finance and risk management, few events can derail a financial plan as swiftly as a criminal conviction related to driving. Among the various legal outcomes one might face following an alcohol-related traffic stop, the term “wet and reckless” frequently emerges. While it may sound like a minor infraction compared to a standard Driving Under the Influence (DUI) charge, a “wet and reckless” conviction carries substantial fiscal implications that ripple through a person’s insurance premiums, employment opportunities, and long-term wealth-building strategies.

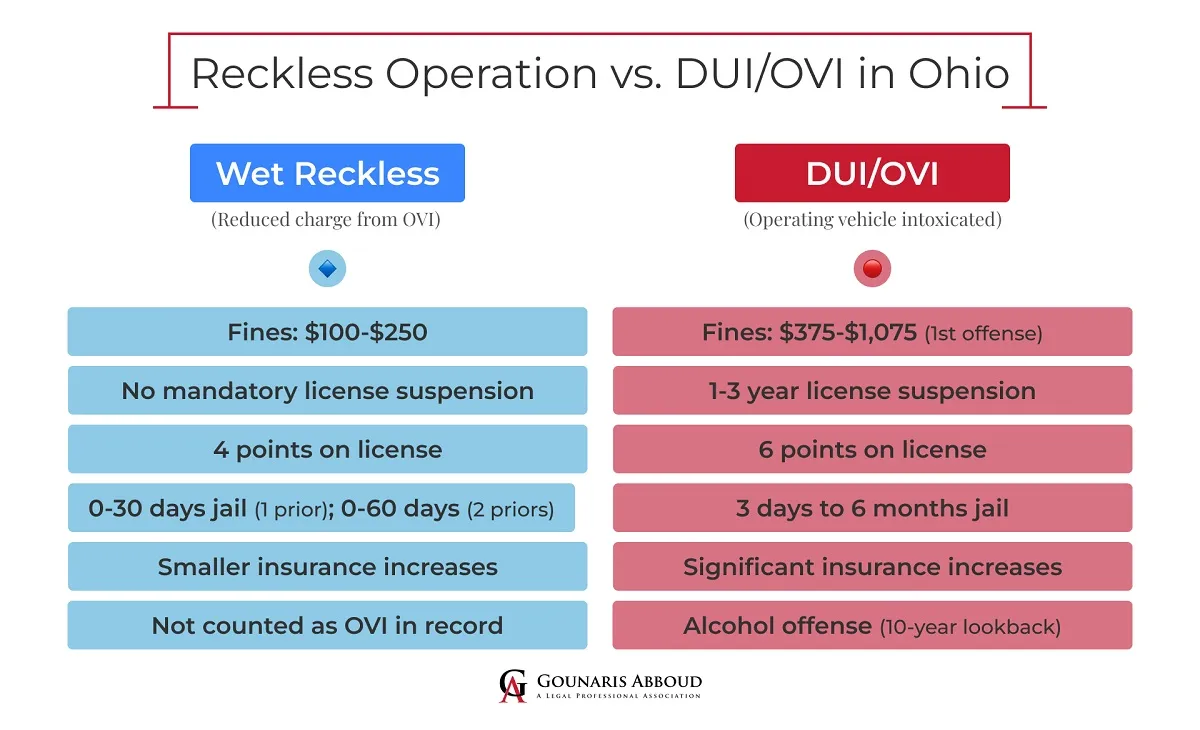

Strictly speaking, a “wet and reckless” is a plea bargain—specifically a conviction for reckless driving under California Vehicle Code 23103, with a formal note on the record pursuant to 23103.5 that alcohol or drugs were involved. From a financial perspective, understanding this distinction is crucial for anyone looking to mitigate the economic damage of a legal misstep.

The Anatomy of a Wet and Reckless: Legal Definition and Financial Context

To understand the financial weight of a wet and reckless charge, one must first understand its position in the hierarchy of legal liabilities. It is not a charge an officer writes on a ticket at the scene; rather, it is a negotiated settlement. When a defense attorney identifies weaknesses in the prosecution’s case—such as a blood alcohol content (BAC) level very close to the 0.08% limit or procedural errors—they may negotiate the original DUI down to a wet and reckless.

How it Differs from a Standard DUI

From a purely monetary standpoint, a wet and reckless is often viewed as the “lesser of two evils.” A standard DUI conviction in many jurisdictions carries mandatory minimum jail time, longer probationary periods, and significantly higher statutory fines. In contrast, a wet and reckless typically results in shorter probation (usually one to two years instead of three to five) and lower court-imposed fines. However, the financial benefit is relative. You are still dealing with a misdemeanor conviction that appears on background checks, which can have a cooling effect on your earning potential.

The Upfront Costs of Legal Representation

Before any fines are paid to the state, the first major financial hurdle is the legal defense. Retaining a private attorney to negotiate a DUI down to a wet and reckless can cost anywhere from $2,500 to $10,000 or more, depending on the complexity of the case. While this is a significant “sunk cost,” many financial advisors view it as a form of loss litigation. Paying for a high-quality defense to secure a reduced charge can potentially save tens of thousands of dollars in long-term insurance hikes and lost wages over the subsequent decade.

The Immediate Financial Impact: Fines, Fees, and Restitution

The moment a plea is entered, the immediate fiscal liabilities begin to accrue. For many individuals, the “sticker price” of the fine mentioned in court is only a fraction of the total out-of-pocket expenditure.

Court-Ordered Fines and Assessments

A wet and reckless conviction usually carries a lower base fine than a DUI—often ranging from $145 to $1,000. However, the “penalty assessments” added by the state and county can quadruple the base fine. In many cases, a $300 base fine transforms into a $1,200 total payment due to court construction funds, DNA identification funds, and various administrative surcharges. For an individual living paycheck to paycheck, this sudden liquidity drain can necessitate high-interest personal loans or credit card debt, further compounding the financial damage.

Mandatory Education Programs and Their Costs

Even with a reduced charge, the court almost always mandates the completion of an alcohol education program (often referred to as “DUI school”). While a standard DUI might require a three-month, six-month, or nine-month program, a wet and reckless often requires a shorter six-week or twelve-week course. Regardless of the duration, these programs are not free. Participants are responsible for enrollment fees, which typically range from $200 to $600. Failure to budget for these costs can lead to a probation violation, which triggers even more severe financial penalties and potential incarceration.

Long-Term Economic Consequences: Insurance and Employment

The true “cost” of a wet and reckless conviction is not found in the courtroom, but in the recurring expenses and missed opportunities that follow the individual for years. This is where the charge moves from a one-time expense to a persistent drag on one’s net worth.

The “SR-22” Spike: How Premiums Skyrocket

One of the most persistent myths in personal finance is that a wet and reckless conviction won’t affect your insurance because it isn’t a “DUI.” This is dangerously incorrect. Actuaries—the professionals who calculate risk for insurance companies—view a wet and reckless nearly identical to a DUI.

Once the conviction is reported to the DMV, most insurance providers will reclassify the driver as “high risk.” This often results in:

- Loss of Good Driver Discounts: These discounts, which can save a driver 20% or more annually, are immediately revoked.

- SR-22 Requirements: You may be required to file an SR-22 certificate, a document that proves you carry the state’s minimum liability coverage. Filing this often triggers a massive premium hike.

- Premium Increases: It is not uncommon for monthly insurance costs to double or triple. Over a three-to-seven-year period (the typical time a conviction stays on a driving record for insurance purposes), the cumulative cost of these increased premiums can easily exceed $10,000 to $15,000.

Career Opportunity Costs and Professional Licensing

In the modern economy, your “brand” and your “background” are financial assets. A wet and reckless conviction can significantly impair these assets. For individuals in the “gig economy,” such as Uber or Lyft drivers, a wet and reckless is usually a disqualifying event, leading to an immediate loss of income.

For corporate professionals, the impact is more subtle but no less damaging. Many employment contracts contain “morality clauses” or require disclosure of any misdemeanor convictions. Furthermore, those in licensed professions—such as nursing, law, or accounting—may face disciplinary actions from their respective state boards. The time spent attending hearings and the potential for temporary license suspension represent a direct hit to one’s lifetime earning capacity.

Strategic Financial Planning After a Conviction

Recovering from the financial blow of a wet and reckless requires a disciplined approach to budgeting and risk management. It is not merely about paying the fines; it is about restructuring your financial life to absorb the increased costs of living.

Rebuilding Your Credit and Emergency Fund

The immediate drain on liquid assets following a conviction often leaves an individual’s emergency fund depleted. Priority one should be the replenishment of this fund. Because a wet and reckless makes you more vulnerable to further financial shocks (such as a job loss or further legal issues), having a robust cash cushion is more important than ever. Furthermore, if legal fees were put on credit cards, a targeted debt-snowball or debt-avalanche strategy is necessary to prevent interest payments from ballooning into a long-term liability.

Budgeting for Increased Transportation Expenses

Given the likelihood of increased insurance premiums and potential driver’s license restrictions, a strategic financial plan must account for higher transportation costs. This might involve:

- Downsizing Vehicles: Switching to a car that is cheaper to insure can help offset the premium hike caused by the conviction.

- Utilizing Pre-Tax Commuter Benefits: If your employer offers them, using pre-tax dollars for public transit can free up cash flow to pay off court-related debts.

- Auditing Insurance Policies: While options will be limited, shopping around for “high-risk” insurance specialists can sometimes yield a lower rate than sticking with a traditional provider that no longer wants your business.

Conclusion: The Price of a Second Chance

A “wet and reckless” is frequently described as a “win” in the legal system, but in the world of personal finance, it is a significant loss that requires careful management. While it offers a shorter path to legal resolution than a standard DUI, its impact on insurance, employment, and overall cash flow remains formidable.

By treating a wet and reckless as a major financial event—rather than just a legal one—individuals can take the necessary steps to mitigate the damage. This involves recognizing the long-term “hidden costs,” planning for the multi-year insurance spike, and safeguarding one’s career against the stigma of a criminal record. Ultimately, the best financial strategy regarding a wet and reckless is prevention; however, for those already facing the consequences, rigorous financial discipline is the only way to ensure that a temporary mistake doesn’t turn into a permanent financial catastrophe.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.