For many Americans, the dream of homeownership is a cornerstone of financial security and a symbol of stability. However, the path to achieving this dream can often feel complex and financially daunting, especially for those looking to navigate the intricacies of real estate transactions. When we consider the significant contributions made by our nation’s veterans and active-duty service members, it becomes clear that facilitating their homeownership journey is not just a matter of fairness, but a vital component of honoring their service. This is where the VA mortgage steps in, a powerful financial tool designed to make owning a home more accessible for those who have served.

The Department of Veterans Affairs (VA) doesn’t directly issue loans. Instead, they guarantee a portion of the loan made by private lenders, such as banks and mortgage companies. This guarantee reduces the risk for the lender, allowing them to offer more favorable terms to eligible veterans. Think of it as a safety net for the lender, making them more comfortable extending credit to individuals who might otherwise face challenges securing traditional financing. This innovative approach, born from a deep understanding of the financial landscape and a commitment to supporting our service members, leverages private capital while providing a crucial government backing.

This article will delve into the multifaceted world of VA mortgages, exploring their unique advantages, the eligibility requirements, and the practical steps involved in securing one. We’ll also touch upon how this financial instrument intersects with broader themes of personal finance, technology in lending, and even the branding associated with recognizing and rewarding military service.

Unlocking the Benefits: Why a VA Mortgage Stands Out

When comparing home financing options, VA mortgages consistently emerge as a standout choice for eligible veterans. The advantages they offer are significant and can translate into substantial long-term financial benefits, impacting everything from initial affordability to the overall cost of homeownership.

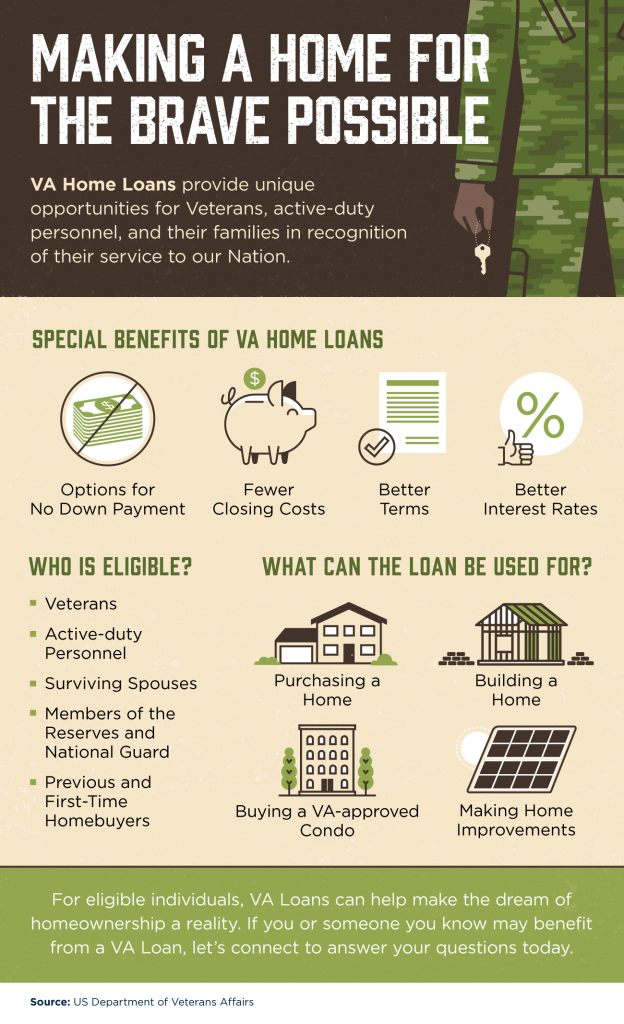

The Power of No Down Payment

Perhaps the most celebrated benefit of a VA mortgage is the potential to purchase a home with no down payment required. For many aspiring homeowners, a substantial down payment is the biggest hurdle to overcome. The traditional path often demands 5%, 10%, or even 20% of the home’s purchase price upfront. This can take years to save, delaying the dream of homeownership indefinitely.

VA mortgages, however, can allow eligible borrowers to finance 100% of the home’s value. This drastically lowers the barrier to entry, making homeownership a reality for a much wider range of service members and veterans, even those who may not have accumulated significant savings. This benefit isn’t just about initial affordability; it also means that the capital that would have been tied up in a down payment can remain accessible for other financial goals, such as investing, home improvements, or simply building an emergency fund. This strategic flexibility in personal finance can be a game-changer.

Competitive Interest Rates

Beyond the zero down payment, VA mortgages typically feature highly competitive interest rates. Because the VA guarantees a portion of the loan, lenders face less risk. This reduced risk is often passed on to the borrower in the form of lower interest rates compared to conventional loans. Over the life of a mortgage, even a slight reduction in the interest rate can amount to tens of thousands of dollars saved. This directly impacts the monthly mortgage payment, making it more manageable and freeing up funds for other financial priorities.

When considering the broader spectrum of “Money” topics, securing a lower interest rate is a fundamental principle of smart investing and personal finance. It’s about minimizing your cost of borrowing and maximizing your long-term financial well-being. The VA mortgage, by design, facilitates this principle for a deserving segment of the population.

No Private Mortgage Insurance (PMI)

Another significant advantage is the elimination of Private Mortgage Insurance (PMI). For conventional loans with down payments less than 20%, lenders typically require PMI to protect themselves against potential default. PMI premiums are an additional monthly cost that adds to the overall expense of homeownership.

VA mortgages do not require PMI, regardless of the down payment amount (or lack thereof). While there is a VA Funding Fee (which we’ll discuss later), it’s typically a one-time charge that can often be financed into the loan. This removal of PMI further reduces the monthly housing cost, making VA-financed homes more affordable to own on a day-to-day basis. This directly contributes to improved personal finance management for veterans.

Limited Foreclosure Relief

The VA also offers programs designed to assist veterans who may face difficulties making their mortgage payments. While not a guarantee against foreclosure, these programs can provide options such as loan forbearance, repayment plans, or even loan modification. This commitment to supporting homeowners in times of financial distress underscores the program’s dedication to its beneficiaries.

Understanding Eligibility and the VA Funding Fee

Securing a VA mortgage hinges on meeting specific eligibility requirements and understanding the associated VA Funding Fee. These are crucial components that lay the groundwork for accessing this valuable home financing benefit.

Who Qualifies for a VA Mortgage?

Eligibility for a VA mortgage is primarily determined by a veteran’s or active-duty service member’s length and nature of service. The VA has specific service requirements, which generally include:

- Veterans: Typically, those who have served 90 consecutive days of active service during wartime, or 181 days of active service during peacetime. There are also provisions for those who were discharged due to a service-connected disability.

- Active-Duty Service Members: Generally, individuals who have served at least 90 consecutive days of active service.

- Surviving Spouses: Unremarried surviving spouses of veterans who died in service or as a result of a service-connected disability may also be eligible.

To prove eligibility, borrowers will need to obtain a Certificate of Eligibility (COE) from the VA. This document confirms that the applicant meets the service requirements and is authorized to use their VA home loan benefit. This process is streamlined through online portals and direct applications, reflecting the increasing integration of technology in government services.

The VA Funding Fee: An Investment in the Program

The VA Funding Fee is a one-time charge paid by the borrower to the VA. This fee helps to offset the costs of the VA loan program and reduces the burden on taxpayers. The amount of the funding fee varies depending on several factors, including:

- Type of service: Whether the borrower is a veteran, active-duty, National Guard, or Reserves.

- Down payment amount: A larger down payment can reduce the funding fee.

- Prior use of VA loan benefit: Subsequent uses of the VA loan benefit may incur a higher funding fee.

- Whether the loan is for a first-time or subsequent purchase.

It’s important to note that certain veterans are exempt from paying the VA Funding Fee. This includes veterans who receive VA compensation for service-connected disabilities or who are eligible to receive such compensation. This exemption is a significant financial relief for those who have borne the physical costs of their service.

The funding fee can typically be financed into the loan amount, meaning borrowers don’t necessarily have to pay it out of pocket at closing. This aligns with the overall goal of making homeownership as accessible as possible. The transparency around this fee, often explained through detailed online calculators and by lending institutions, speaks to the importance of financial literacy within the “Money” domain.

The VA Mortgage Process: From Application to Closing

Navigating the VA mortgage process requires understanding each step, from initial inquiry to securing the keys to your new home. While similar to conventional mortgages, the VA aspect introduces specific requirements and benefits.

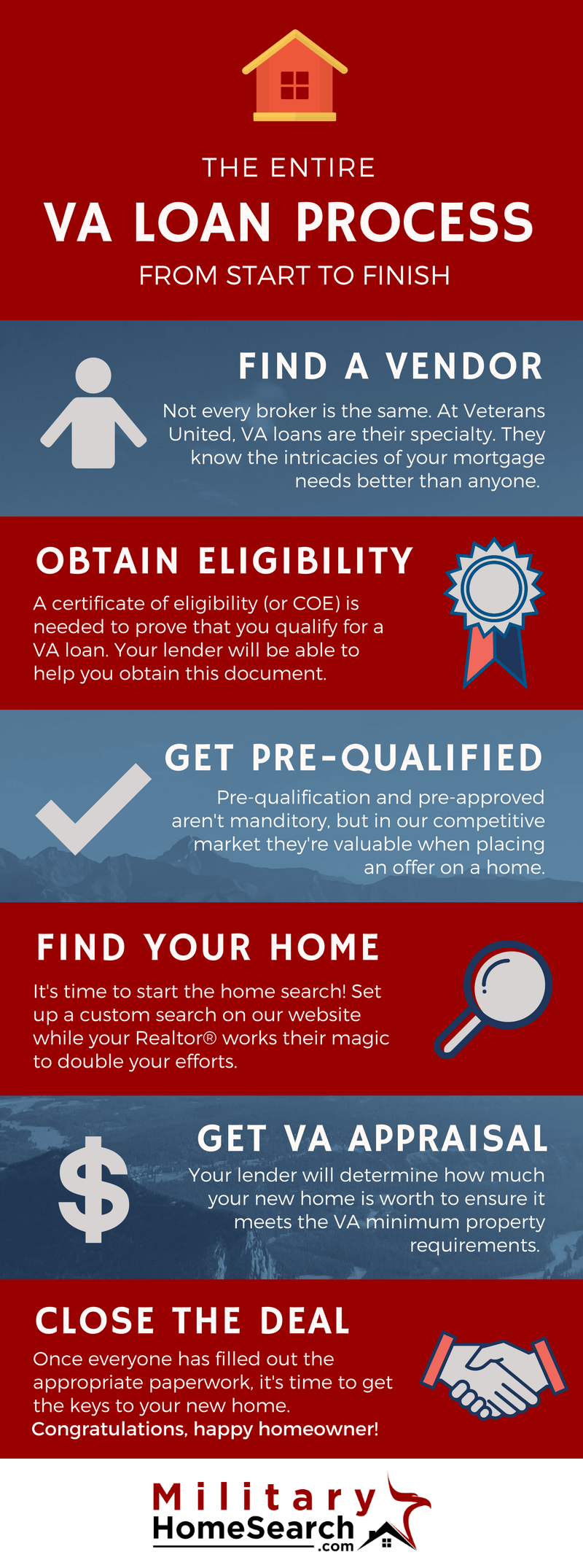

Finding a VA-Approved Lender and Getting Pre-Approved

The first practical step is to find a VA-approved lender. Not all mortgage lenders offer VA loans, so it’s essential to seek out those who specialize in or are authorized to originate them. This is where technology plays a significant role. Online platforms and financial comparison tools can help you identify lenders, compare rates, and even initiate the pre-approval process remotely.

Getting pre-approved for a VA loan is crucial. This involves the lender reviewing your financial information, including your credit score, income, and assets, to determine how much you can borrow. The pre-approval process also helps you understand your purchasing power and strengthens your offer when you find a home. Lenders will also verify your VA eligibility by requesting your COE.

The Home Appraisal and Loan Underwriting

Once you have a ratified purchase agreement, the VA requires a VA-certified appraisal of the property. This appraisal is more comprehensive than a standard appraisal and includes specific minimum property requirements (MPRs) to ensure the home is safe, sanitary, and structurally sound. This focus on property quality is a unique aspect of the VA loan program, aiming to protect veterans from purchasing homes with significant defects.

The loan underwriting process is where the lender thoroughly reviews all your documentation, including your income verification, credit history, and the VA appraisal, to ensure you meet all the requirements for the loan. This meticulous review process, often facilitated by digital platforms and automated underwriting systems, ensures compliance with VA regulations and the lender’s own standards.

Closing on Your VA Mortgage

The final stage is closing on your VA mortgage. This is when all parties sign the necessary paperwork, funds are disbursed, and ownership of the property is transferred to you. You will typically receive a Closing Disclosure outlining all the final loan terms, fees, and costs.

The transparency and digital integration in modern closing processes, often managed through secure online portals and electronic signatures, represent the evolution of the “Tech” landscape within the financial sector. This digital transformation makes the closing process more efficient and accessible.

Beyond the Loan: VA Mortgages and Your Financial Future

The impact of a VA mortgage extends beyond the initial purchase of a home. It represents a strategic financial decision that can influence your long-term financial health, your ability to leverage technology, and even the way your service is recognized and valued.

VA Mortgages and Your Overall Financial Strategy

The financial advantages of a VA mortgage – no down payment, competitive rates, and no PMI – can significantly impact your personal finance strategy. By freeing up capital that would otherwise be tied up in a down payment and reducing your monthly housing costs, you have more resources available for other financial goals. This could include:

- Investing: Accelerating your investment portfolio growth with the capital you save.

- Debt Reduction: Paying down other high-interest debts more aggressively.

- Emergency Fund: Building a robust emergency fund for greater financial security.

- Home Improvements: Investing in your new home to increase its value and your enjoyment.

Understanding how a VA mortgage fits into your broader financial plan is key to maximizing its benefits. This involves careful budgeting, informed decision-making about your financial priorities, and a clear understanding of the long-term implications of your borrowing choices.

The Role of Technology in VA Lending

The landscape of mortgage lending is continuously being shaped by technological advancements. For VA mortgages, this means:

- Online Applications and Pre-approvals: Streamlining the initial stages of the loan process.

- Digital Document Submission: Reducing paperwork and speeding up processing times.

- Virtual Tours and Property Assessments: Leveraging technology to facilitate remote property evaluation.

- AI-Powered Underwriting Tools: Enhancing efficiency and accuracy in the underwriting process.

These technological integrations make the VA mortgage process more accessible, efficient, and transparent for borrowers. As the “Tech” sector continues to innovate, we can expect even more advancements that will further simplify and improve the VA home buying experience.

The “Brand” of Service: Recognizing and Rewarding Veterans

The existence of the VA mortgage program itself is a testament to the societal “brand” of valuing and rewarding military service. It’s a tangible way to acknowledge the sacrifices made by those who have served our country. This recognition extends beyond the financial benefits of the loan itself, shaping the narrative of how veterans are supported and integrated back into civilian life.

The process of obtaining a VA mortgage, while a financial transaction, also carries a symbolic weight. It represents a nation’s commitment to its service members, a promise of stability and opportunity. This aligns with broader themes of personal and corporate branding, where consistent actions and programs build trust and reinforce a positive identity. The VA mortgage, in essence, reinforces the brand of a grateful nation.

Conclusion: A Powerful Tool for Homeownership

The VA mortgage is far more than just a home loan; it’s a powerful financial tool designed to honor the service and sacrifice of our nation’s veterans and active-duty military personnel. By offering the remarkable benefit of no down payment, competitive interest rates, and the elimination of PMI, it significantly lowers the barriers to homeownership.

Navigating the eligibility requirements and the VA Funding Fee is a necessary step in unlocking these advantages. Understanding the process, from finding a VA-approved lender and getting pre-approved to the appraisal and closing, ensures a smoother and more informed journey. Furthermore, recognizing how a VA mortgage fits into your overall financial strategy and embracing the technological advancements that streamline the process will maximize its long-term benefits.

Ultimately, the VA mortgage program stands as a shining example of how strategic financial policy, coupled with a commitment to recognizing service, can profoundly impact the lives of individuals and families. It empowers our nation’s heroes to achieve the dream of homeownership, laying a foundation for a secure and prosperous future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.